US university students are up to their ears in debt. And, increasingly, so are many US colleges.

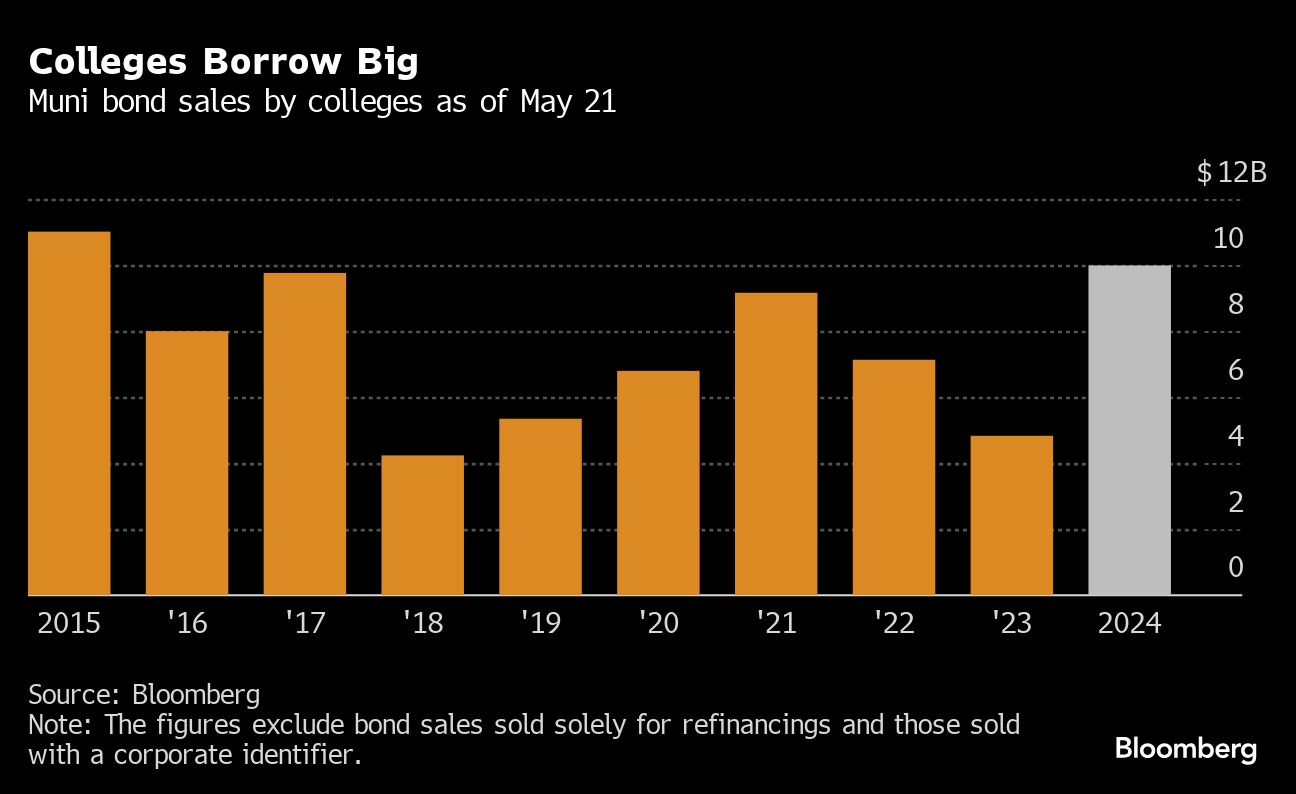

From small liberal-arts schools to giant universities, America’s ivory towers are on a borrowing binge as part of an effort to spruce up their campuses and lure the next generation of students. In just the last five months, roughly 50 colleges have tapped investors to build student centers, refurbish dorms, and make-over academic buildings as well as refinance debt — to the tune of $10 billion, according to data compiled by Bloomberg. That volume is more than double from the same time last year.

The fraught economics of higher education are leaving some institutions with an uncomfortable choice: take on more debt in the hope of attracting new students to campus — a bet that doesn’t always work out — or risk being left behind in the race for a rapidly dwindling pool of high school seniors. Adding to the peril, borrowing threatens to raise the cost of college, which is already pushing close to $100,000 a year at some institutions.

“There’s an arms race to create an overall attractive social and academic experience that will cause students to choose those colleges,” said Jeff Hamrick, chief financial officer at Whitman College, which sold debt in March to build housing for juniors and seniors at the campus in Walla Walla, Washington. “As you participate in this arms race, you want to make sure that you’re using that debt really wisely.”

Taking on more debt could further pressure a campus that is struggling financially. New York’s Cazenovia College shuttered in 2023 after it couldn’t pay its debt - the private school sold bonds for campus projects less than four years earlier. And Ohio’s Notre Dame College in March cited “significant debt” as a reason for its closure.

The list of college borrowers this year is long and varied. Classrooms at Cornell University are getting upgraded, as are dorms at the University of Maryland. Harvard University is renovating medical school offices and building new housing options in Boston while Arizona State University is erecting a 180,000 square-foot research facility for its polytechnic campus.

On the smaller end, Muhlenberg College, a small, private liberal-arts school nestled in eastern Pennsylvania, has grand plans to spruce up one of the first buildings that prospective students and their parents will see on tours. The $35 million expansion includes a welcome center for visitors, floor-to-ceiling windows, an event space and career center.

Boosting its appeal could help. Muhlenberg has seen its full-time undergraduate enrollment drop by almost 20% from six years prior, according to 2022 data from the US Department of Education.

Ahead of its bond sale this month, Moody’s Ratings downgraded Muhlenberg to A3 — four steps above junk. The college’s bond deal will increase its debt load by about 40% even as there’s “widening misalignment” between revenue and expenses, Moody’s analysts said.

A spokesperson for Muhlenberg said in a statement that many schools are in a similar situation “owing to the lingering effects of the global pandemic and the need to adjust to new demographic and market realities.”

Muhlenberg refinanced debt, which many schools have done to save money. The school has seen record applications for the fall and is on pace to beat its first-year enrollment goals, a school spokesperson said.

One problem is that it has staunch competition. Just 10 miles away, Moravian University — another small, private liberal-arts school — is also in the midst of a $40 million expansion of its student union. Both schools tapped the capital markets to raise funds this month.

“There are schools that are having significant financial challenges, trouble balancing their budget and doing some Hail Mary financing to try and make things work,” said Mark Reed, Moravian’s chief financial officer. That doesn’t describe Moravian, which has reported 40% enrollment growth over 10 years.

Demographic Challenges

The crux of the challenges many schools face comes down to the basic economic principles of supply and demand. There are simply too many colleges and not enough students.

The number of high school graduates are expected to drop 10.4% between 2026 to 2037, according to the Western Interstate Commission for Higher Education. Pennsylvania alone has 88 private four-year institutions, of which 81 have 5,000 undergraduate students or less, according to federal data.

It’s a trend that’s playing out across the country, and pushing schools that look similar on paper to seek to differentiate themselves.

Some schools are taking on debt to finance sports facilities — betting that new arenas will help attract student-athletes who want to continue playing after high school. New York’s Alfred University sold $19 million of bonds to help build a $30 million, 41-acre sports complex.

Mark Zupan, president of Alfred, sees athletics as one of the areas that can “move the needle” to boost enrollment and retention. About 40% of the school’s student body is made up of student-athletes. For the last several years, the college has been “laser focused” on improving the student experience, he said.

More sports teams are expected to help the college add and retain about 170 new students. The sports complex will serve new baseball, rugby and field hockey teams plus an expanded track program, Zupan said.

Jeremy Bass, who advises colleges on their debt at PFM Financial Advisors, said schools are pursuing capital projects that may have been put on hold over the past few years. They’re also looking to take advantage of strong conditions in the muni market, he said.

A bevy of colleges have also taken advantage of the stability of interest rates to refinance their debt.

Trinity University, a 2,600-student college in San Antonio, Texas, sold bonds to help finance a new welcome center, as well as the renovation of residence halls. It recently opened a $130 million science and innovation building. The college noted in its bond offering documents that campus visits are influential for students picking colleges.

Borrowing costs in the muni market for colleges are elevated compared to the era of near-zero interest rates, but they aren’t dramatically higher. Top-rated muni issuers can borrow at a yield of about 3.8% in 30 years, whereas a homeowner faces a mortgage rate of more than 7%.

Colleges “have been playing a wait and see game,” said Megan Kearns, a higher education analyst for S&P Global Ratings. “They’ve hit the point where they need to get moving.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Amanda Albright, Sri Taylor