The regular market for US equities runs for 390 minutes on a standard trading day. But at the rate things are going, eventually the last 10 might be the only ones that matter.

About a third of all S&P 500 stock trades are now executed in the final 10 minutes of the session, according to data compiled by BestEx Research, a developer of trading algorithms. That’s up from 27% in 2021.

Now fresh evidence emerging from Europe — where the pattern is similar — suggests the trend may be hurting liquidity and distorting prices.

It’s new ammo for critics of the global boom in passive investing, because index funds drive the phenomenon. These products typically buy and sell shares at the close, since the last prices of the day are used to set the benchmarks they aim to replicate.

Assets in passive equity funds have surged over the past decade to more than $11.5 trillion in the US alone, according to data compiled by Bloomberg Intelligence, shifting ever-more trading to the end of the session. Active players seeking to take advantage of that liquidity have followed, creating a self-reinforcing cycle.

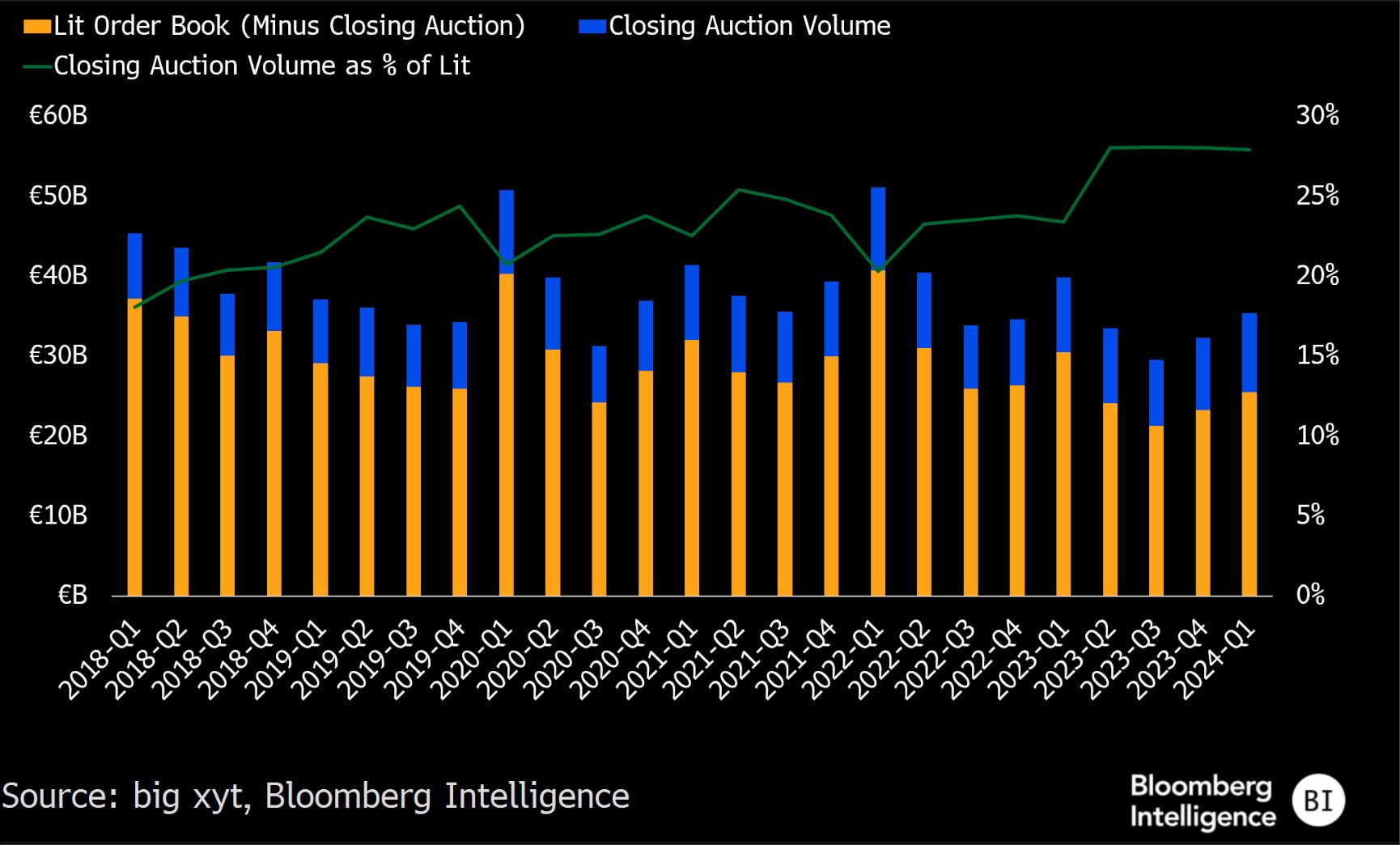

The closing auction in Europe, which occurs after the end of regular trading, now accounts for 28% of volumes on public venues, up from 23% four years ago, data from Bloomberg Intelligence and analytics firm big xyt show.

“The common knowledge is that closing auctions are very, very good mechanisms to close markets,” said Benjamin Clapham at Goethe University Frankfurt, co-author of a new research paper titled Shifting Volumes to the Close: Consequences for Price Discovery and Market Quality. “This might be true, but if we have such a shift of volumes to this very last opportunity of trading in the day, we might see price inefficiencies.”

The paper, which Clapham wrote with colleague Micha Bender and Deutsche Bundesbank researcher Benedikt Schwemmlein, focused on large-caps on the London, Paris and Frankfurt exchanges in the four years through mid-2023. The trio found shares generally move between the end of continuous trading and the last price set in the closing auction, yet 14% of that move reverses overnight — a sign it’s fueled by one-sided flows rather than fundamentals.

The new research echoes earlier studies, including in the US, where a 2023 paper also argued that moves seen during the auction revert overnight as a result of the liquidity dynamic.

The charge is one of a number leveled against passive investing, including that it can blindly inflate company valuations and wreak havoc when major indexes rebalance, triggering billions in one-way trades. The litany of concerns has inspired high-profile attacks from critics such as Elon Musk, and more recently Greenlight Capital’s David Einhorn.

But the extent to which any closing distortions should cause concern is uncertain and, as with so much in the modern market, the debate isn’t clear cut.

For Hitesh Mittal, BestEx Research’s founder, the overnight reversion is part of normal market function. Passive funds may be buying at fractionally higher prices at the close, but he reckons the cost is “way, way less” than liquidity providers would charge for transactions of their size in thinner liquidity earlier in the day.

In the US, the mechanism to determine closing prices runs alongside the last minutes of continuous trading. Nearly 10% of all US shares were traded in that closing auction last month, nearing previous 2019 highs after dipping in the retail trading frenzy, data compiled by Rosenblatt Securities show.

Chuck Mack, head of strategy for North American trading services for Nasdaq, said market participants like the transparent price discovery and “depth of liquidity” in closing auctions. He said US intraday liquidity is affected more by the growing fragmentation of stocks trading on different platforms.

Meanwhile, two other researchers — Carole Comerton-Forde at the University of Melbourne and Barbara Rindi at Bocconi University — concluded in 2022 that ostensible European reversals might be due to noise at the market open, rather than distortions, and that intraday liquidity hasn’t been hurt by the closing auction. Writing on behalf of the duo, Comerton-Forde said regulators don’t have cause for concern yet, “but should continue to watch this space in case things change.”

The London Stock Exchange didn’t immediately respond to a request for comment. A spokesperson for Euronext acknowledged that price reversions occur in the wake of indexes rebalancing, but said “observed reversals are typically modest, and market overreactions are common after significant liquidity events.”

A Deutsche Börse spokesperson said that while there were different views among market participants, closing auctions were generally not seen as a problem.

In the US, even as volumes shift to the end of day, the growing role of retail investors has prompted a number of brokerages like Robinhood to offer 24-hour trading of some securities to give them maximum opportunity to buy and sell. Yet for institutional pros, it’s increasingly all about those last few minutes.

“When I do speak to clients who are trading portfolios that are more sensitized to these changes in liquidity, they will definitely wait,” said Mark Montgomery, head of business development at big xyt. “As the liquidity decreases in the continuous part of the day, the potential for them to leak information about their intent is far greater.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Justina Lee