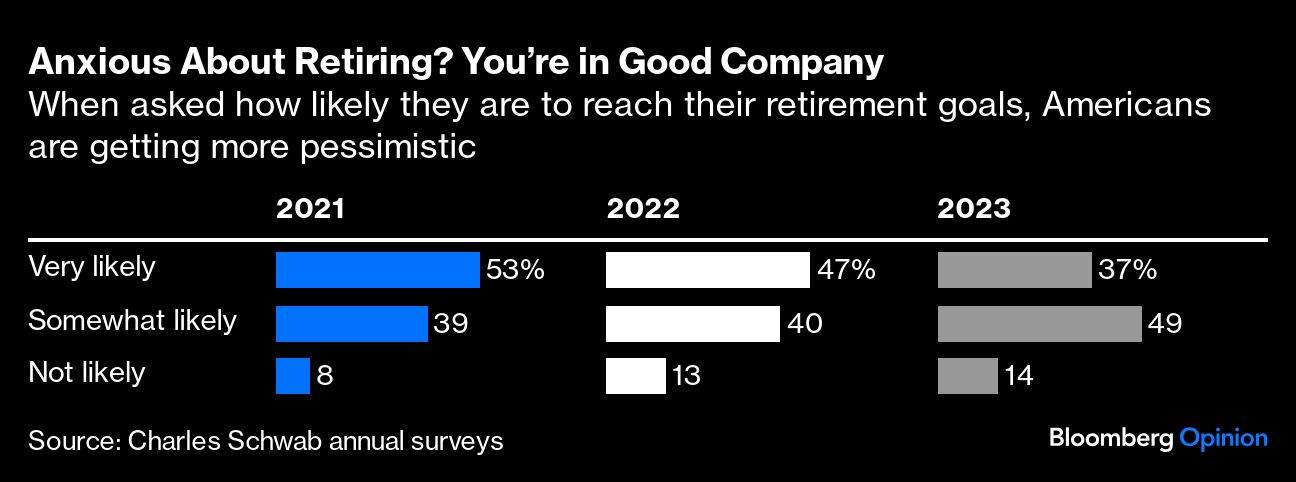

The often-cited goal of having a $1 million retirement nest egg needs to be retired itself. Adjusted for inflation , it would take nearly $1.9 million to have the same purchasing power today as in 1999, when the oldest of millennials were just turning 18. Granted, $1 million still sounds like a lofty sum to many Americans, which could be why so many are nervous that they won’t reach the double-comma club by retirement.

What makes me anxious for my fellow millennials, however, is how many are relying on social media, YouTube, podcasts and cable news for free advice about how to build their retirement plans. All these platforms are loaded with unreliable information that could create unrealistic expectations.

Nearly 80% of millennials and Gen Z have turned to social media for financial advice, according to a Forbes Advisor survey . One reason is that it is very hard to set up a simple, safe and affordable retirement plan. With no federal requirement for employers to offer a 401(k) plan to employees, let alone an employer match, it falls to individuals to figure out how to plan for old age.

So I shuddered recently when I heard longtime personal finance guru Dave Ramsey suggest retirees could expect to afford withdrawals of 8% each year from their retirement savings, which is presumably based on the assumption that the stock market will return 12% on average .

Ramsey himself might point out that he isn’t an investment adviser and recommend that listeners of his show consult a professional. But that rarely stops people from taking advice from what they perceive to be a credible source. And while it is seductive to hear that you can safely withdraw $80,000 annually on a $1 million portfolio, it adds a lot of risk into retirement planning — especially if you retire into a down market.

Most financial professionals suggest a withdrawal rate closer to 4%, with adjustments based on market conditions and cost of living. That implies someone with $1 million saved for retirement could safely withdraw $40,000 a year without outliving their money. This is based on a decades-old paper Retirement Savings: Choosing a Withdrawal Rate That Is Sustainable, more colloquially known as the Trinity study. But many advisers and brokerage firms run their own stress tests to determine a safe rate.

It’s a good rule of thumb, though retirees will have to adjust their withdrawal rates based on actual market conditions when they retire. And appetite for risk varies. Some experts would agree with Ramsey that 4% is needlessly conservative, while others would push to set a nest-egg goal based on a lower early withdrawal rate, such as 3%, to hedge against a bear market.

Fortunately, recent legislation should at least get people started, especially the youngest workers. Starting in 2025, the rollout of the Secure 2.0 Act will require newly created 401(k) plans to auto-enroll employees, with a minimum contribution of 3% of their annual pay. Automatic adjustments will raise contributions annually by 1% until hitting a 10% or 15% threshold.

The growth of opt-out plans could help Gen Z build stable retirement savings. But the new rules don’t apply to existing plans, meaning many workers won’t benefit from the automatic increase in contributions.

Automatic enrollment and savings increases might sound paternalistic, and in some ways they are. But in the absence of proper financial education and initiative on the part of workers, many people would otherwise put off starting a 401(k) and increasing contributions.

That said, a requirement to contribute to a retirement plan does not address the widespread lack of understanding about how to properly invest those funds. Putting contributions into a target-date fund is a more or less suitable strategy, though not for everyone. Millennials and Gen Z would be better off speaking with a professional to assess their strategy instead of turning to the internet, which is fine for recommendations on which water bottle to buy but not great for free investment advice.

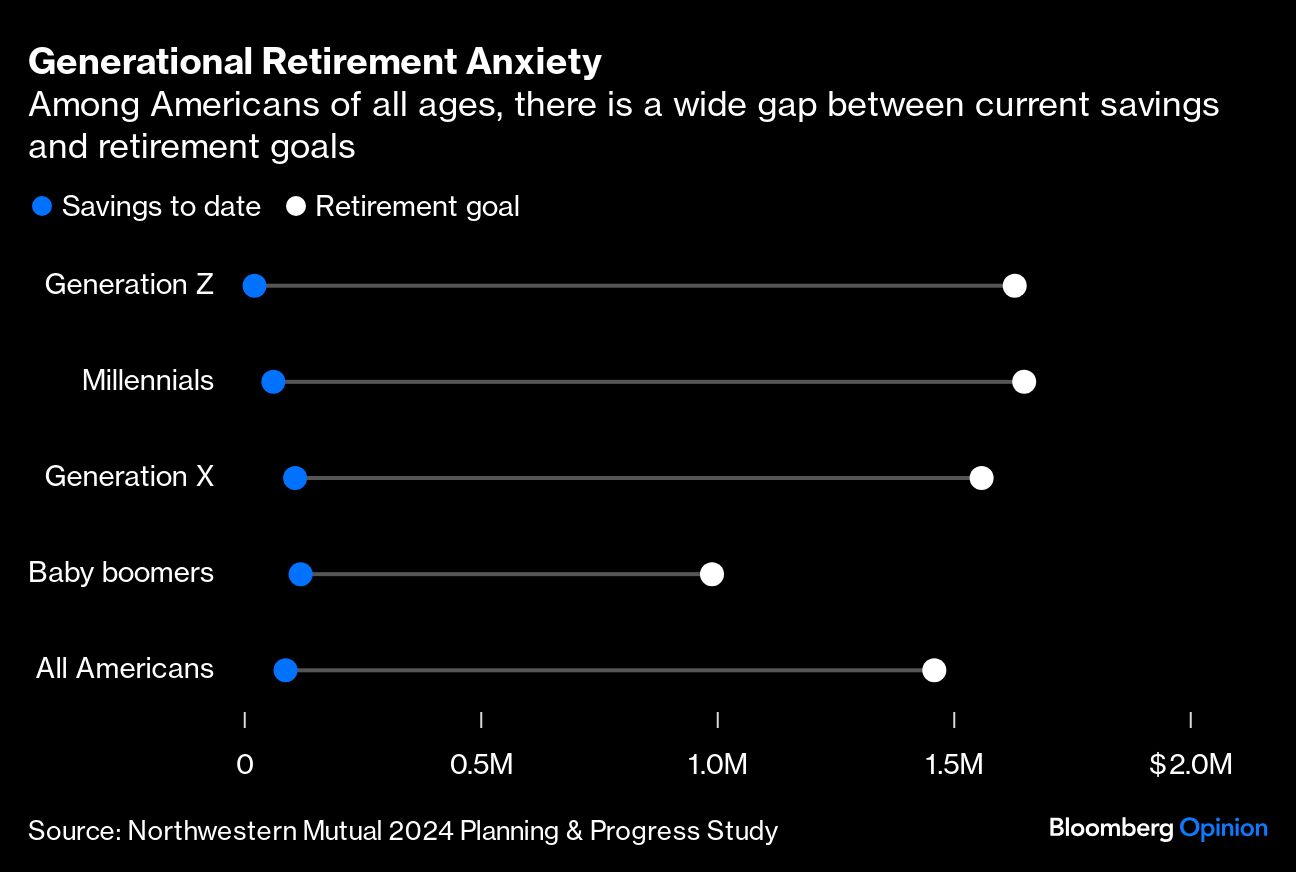

I don’t want to be a complete doomsayer. Plenty of millennials are doing just fine coping with conflicting advice. The average millennial has $62,600 currently invested for retirement and plans to retire at about 64, according to a 2024 Northwestern Mutual study. That means the average 34-year-old would need to invest approximately $9,000 annually, assuming an 8% market return, to get close to their goal of $1.65 million. That’s achievable, though the continued rise in costs of housing, child care, college tuition and care for aging parents could make it difficult.

The bottom line is that anyone funding their own retirement accounts, no matter the amount, would do well to overestimate how much they’ll need and plan on a conservative withdrawal rate, at least in their early retirement years. Designing a retirement strategy based on free advice is a dangerous plan.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Erin Lowry