The US economy expanded at a strong 3% last year, though growth slowed to a 1.6% annual rate in the first quarter with a drag from imports. Even so, consumer spending and business fixed investment — which is less volatile, and usually gives a better sense of where the economy is headed — rose at a brisk 3%.

Contrary to what commentators such as former Treasury Secretary Larry Summers might say, this strong economy does not complicate the US Federal Reserve’s fight against inflation, nor is it a reason for the bank to delay rate cuts. The past year shows that it is possible to have a rapid decrease in inflation along with low unemployment and strong growth. Notwithstanding 2024’s bumpy start on inflation, there is reason to believe that the tradeoff between demand and inflation is weaker now than in the past.

What’s unusual in this cycle is the pandemic. It drove disruptions in global supply chains, vehicle production, labor force participation, housing construction, spending on goods (which increased during the pandemic) and demand for services (which rose after it ended). All of this has contributed significantly to inflation.

Now the rebalancing is nearly complete: PCE prices, excluding food and energy, are less than a percentage point from the Fed’s target and about half their peak. At the same time, while they are waning, the economic echoes of the pandemic are ongoing.

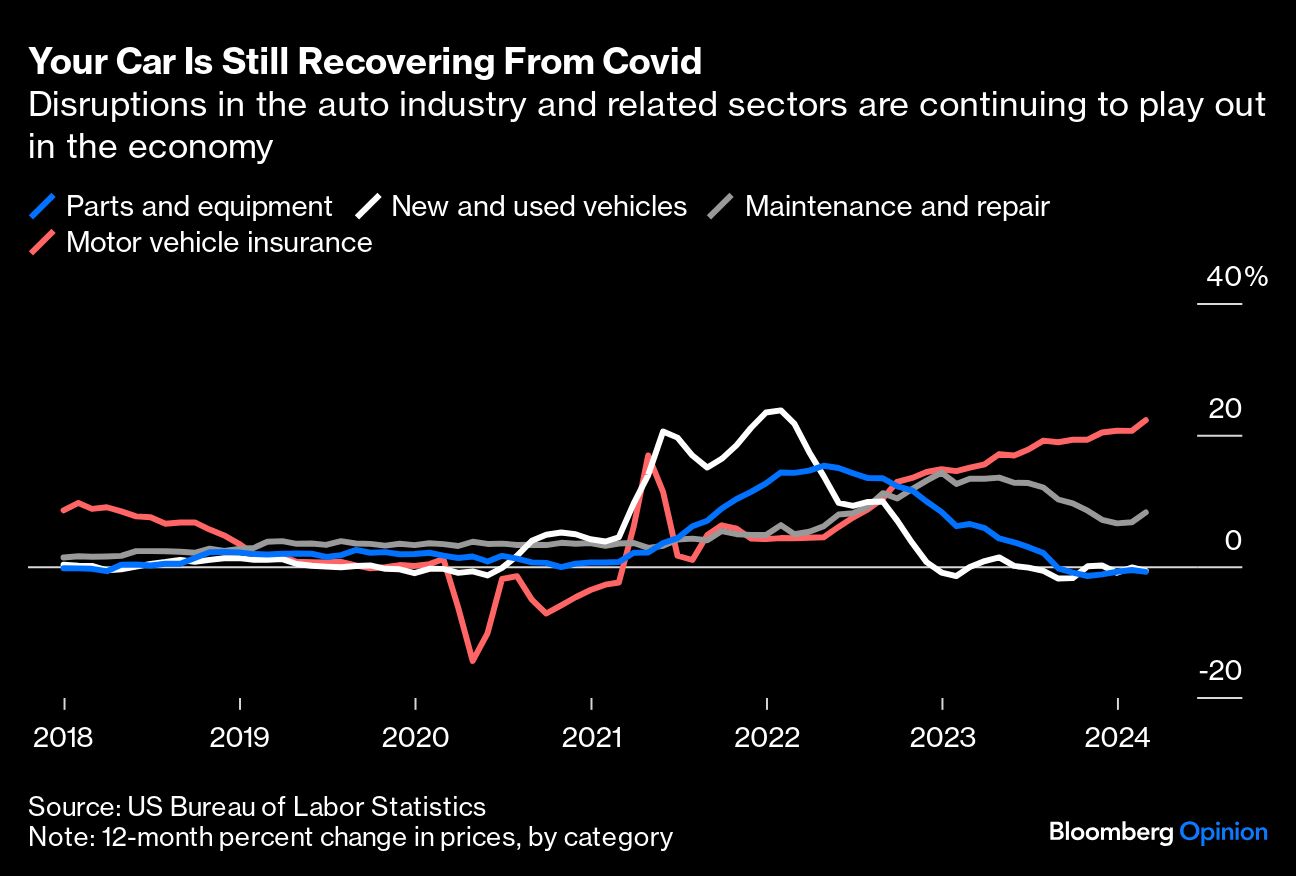

The motor vehicle and related sectors are one example of the complex linkages. Supply chains — as measured by the New York Fed’s index — began to improve in late 2021. Soon after that, new and used vehicle inflation began to ease. Inflation in motor vehicle parts, however, continued to rise, not easing until mid-2022. Then inflation moved into services such as repair and maintenance and insurance.

The stickiest inflation in the “supercore” or core services, excluding shelter, is related to motor vehicles.1 Working through the last echo in motor vehicle insurance is not primarily about current demand or interest rates. Rebalancing, especially with supply-driven inflation, takes considerable time, especially since the Fed’s policy tools are unsuited for the task.

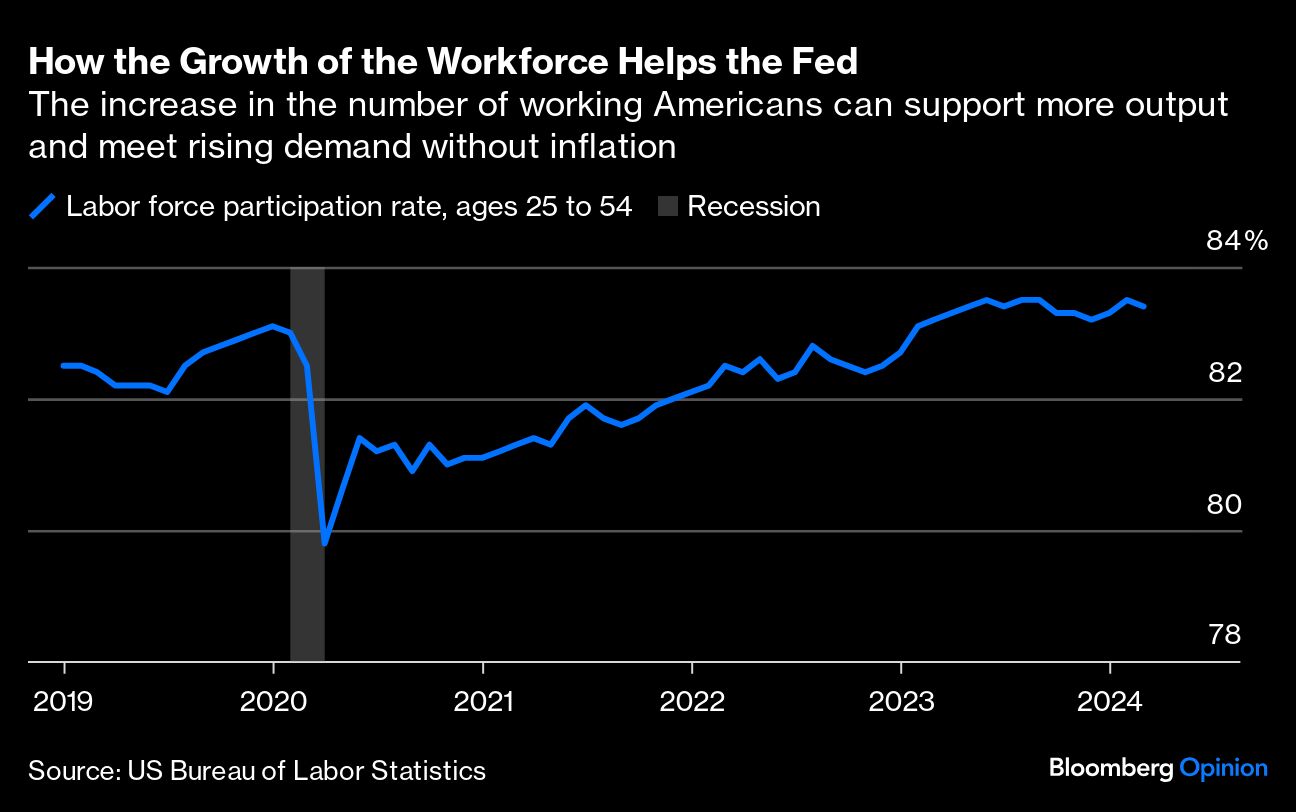

With further improvements on the supply side, strong economic growth should not bring about a return of inflation. The increase in the prime-age labor force, especially immigrants, can support more output and meet rising demand without inflation.

The Congressional Budget Office projects net immigration to the US of 3 million people this year, matching last year's and triple the pre-pandemic average. It expects the level to decrease only slowly in the few years after that. Immigrants and more prime-age women entering the labor force are essential to offset the aging of the population and keep growth high.

This supply-driven growth is good for the Fed. More workers take pressure off the central bank to use high interest rates to reduce demand.

In addition, productivity growth picked up last year, likely reflecting more flexible work arrangements such as working from home. The strong labor market has also improved worker-job matching and brought in people who were on the sidelines. New technologies such as artificial intelligence may support future productivity growth. Again, these developments do not make the Fed’s job harder, though it would need to adjust its models for potential growth and neutral interest rates.

The good news is that Fed Chair Jay Powell seems to recognize these issues and no longer views lower growth as a precondition for lower inflation. So long as the supply of labor is rising and supply-chain issues are improving, he said at his press conference last month, then demand can increase without causing inflation. In fact, he noted, that’s essentially what happened last year, when the US had “a bigger economy where inflationary pressures are not increasing.”

That said, the process of rebalancing the economy and working through the supply disruptions need not be as slow and painful as it has been. Inflation will likely return to target in the next year or so. Still, more than three years of above-target inflation have pushed up prices more than anyone expected before the pandemic, creating hardships for millions of Americans.

Mario Draghi, former president of the European Central Bank, has argued that monetary policy must change its approach in the face of supply-driven inflation. “A world of supply shocks makes monetary stabilization more difficult,” Draghi said. “The lags of monetary policy are typically too long either to restrain supply-driven inflation or offset the resulting economic contraction, meaning monetary policy can at best focus on limiting second-round effects.” His observation lines up well with the current pandemic-driven inflation cycle.

The path forward is complicated. Fiscal policymakers must use more targeted programs to strengthen the supply side, which will necessarily interact with monetary policy. For example, more activist policies to rely more on domestic production could trade resilience for efficiency and increase underlying inflation. The reshoring of the semiconductor manufacturing industry under President Joe Biden, and higher tariffs under a possible President Donald Trump, could make it difficult for the Fed to maintain its 2% target.

Today’s GDP number reflects supply improvements and supports the last mile in the fight against inflation. Yet this cycle also provides a cautionary tale of inflationary supply disruptions sure to occur in the future. It’s that inflation, not today’s, that the Fed should be worried about.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Claudia Sahm