Jamie Dimon Has a Rival in Tech: Silicon Valley Bank

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSince Silicon Valley Bank became the second-biggest failure in US history a year ago, other lenders have been trying to take its place in banking the fast-moving, entrepreneurial world of startups and tech companies. JPMorgan Chase & Co. and HSBC Holdings Plc have jumped into a market focused on small companies that could become the billion-dollar businesses of tomorrow. But these two giant upstarts on the San Francisco scene face stiff competition from a familiar name — Silicon Valley Bank itself, which lives on under the ownership of First Citizens Bancshares Inc.

SVB’s goal is to dominate startup land once again. Sure, it has a trust deficit to rebuild with venture capital firms and their companies, but its well-informed local bankers who are close to their industries give it an edge.

JPMorgan and HSBC, which both picked up parts of failed banks and teams of people in California last year, may offer unquestioned safety for depositors. But it’s far from obvious that these behemoths can recreate SVB’s on-the-ground expertise and attentiveness to hundreds of founders and their venture capital backers. Plus, there’s some skepticism about their long-term commitment.

Marc Cadieux, the 32-year veteran who was SVB’s chief credit officer before its collapse and now runs the business within First Citizens, says the bank can regain its position in time. “One silver lining is how difficult it is to replicate what we do,” he told me at SVB’s new offices in downtown San Francisco last month. “Larger banks entering this market need to still build a business.”

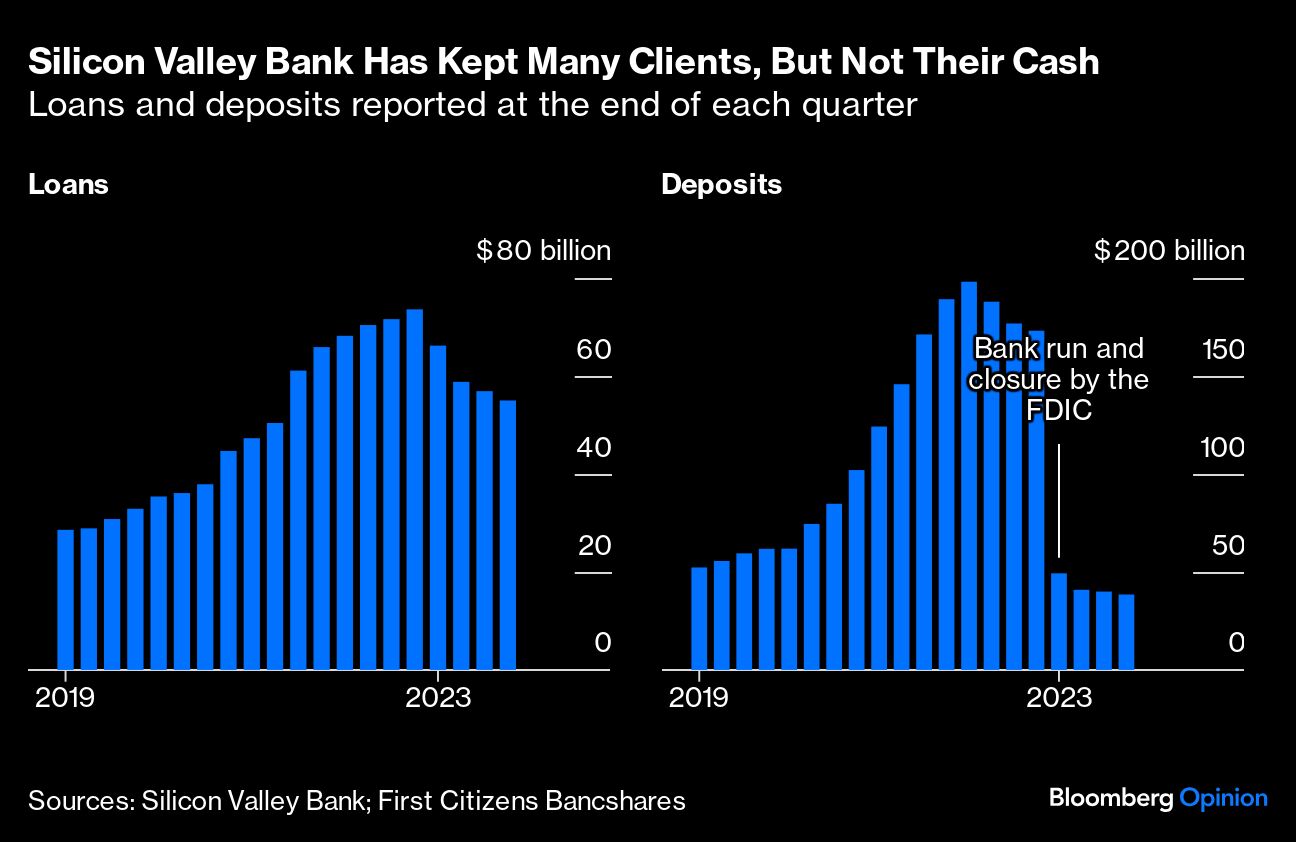

Since it was sold by the Federal Deposit Insurance Corp. to First Citizens, SVB has kept 80% of its pre-crisis staff and a similar share of its clients, although it has lost a lot of their business. At the end of 2022, it had $74 billion of loans and $173 billion of deposits; by the end of 2023, it had $55 billion in loans and just $38.5 billion of deposits. First-quarter results Thursday will show whether it has continued to shrink.

The collapse in SVB’s deposits is unsurprising: It was ruined by a bank run. It’s unlikely to regain dominance in that area because its clients learned a lesson and now spread money among multiple banks. But competitive dynamics have changed across other parts of the business, too. Along with JPMorgan and HSBC, other regional and investment banks have been wooing customers, while fintech firms offering rudimentary but efficient accounts and payments services have also won clients.

It is an odd time for competition to get so heated. The venture capital sector has just been through a huge bubble that peaked in 2021, when more than 350 new unicorns were minted, more than in the previous five years combined, according to analysis by Aileen Lee, founder of Cowboy Ventures, who coined the nickname for $1 billion-plus startups.

Dealing with startups is a long-term game. Banks can struggle to make good day-to-day profits from every client, but as they grow and need more sophisticated (and expensive) financing, the paydays for lenders increase. Those startups that really succeed will go public or get sold for big money, giving their long-time bankers an opportunity to reap advisory fees and land newly enriched wealth-management clients. Lenders also often take warrants from their borrowers, which can convert into valuable shares. This is the definition of “relationship banking.”

JPMorgan and its major Wall Street peers will win plenty of investment banking fees from the venture capital industry whether they offer accounts and loans to startups or not. So JPMorgan’s West Coast push is focused more on those who already have serious money: rich entrepreneurs for its wealth business and venture capital funds for its investment bank. The bankers that joined when JPMorgan bought First Republic Bank from the FDIC last year have brought some Valley contacts and know-how that America’s biggest bank lacked.

HSBC, however, wants to battle SVB on its home turf: First Citizens is bothered enough that it filed a $1 billion lawsuit against the UK-based bank over its hiring of dozens of SVB staff.

These Californian bankers and HSBC’s deal to buy SVB’s tiny UK unit are part of a multi-country effort to tap more deeply into startups, according to Dave Sabow, US head of its rebranded Innovation Banking division. The aim is to channel business to its investment banking and wealth divisions, as well as generate intelligence and potential deals for its existing multi-national technology, pharmaceutical and healthcare clients. HSBC also hopes the entrepreneurial style and methods of its SVB escapees will rub off on the rest of HSBC’s bureaucracy, never famed for its agility or speed. To achieve all this, it needs to build a new reputation in a new market.

“HSBC wasn’t known in seed, startup, entrepreneurial stories,” said Sabow, who formerly ran tech and healthcare banking at SVB. “We’re heavily indexing towards that area to send the message that we’re there for every stage.”

A crucial part of winning potential clients will be convincing them HSBC can be smart when things go wrong: False starts, unforeseen challenges and financial shortfalls are endemic to the sector. This is as much of a challenge for HSBC starting out as it is for SVB staying in the game; many firms have been unable to raise fresh funding since the VC bubble popped, and some never will again.

This is another unusual wrinkle of Bay Area banking: A lender’s relationship with venture capital funds is as important as the one with its startups. Bankers take a view on each backer’s commitment to a business when they come asking for credit. But some investors reckon that banks’ trust in VCs has been burned because the run on SVB was accelerated by big funds telling their companies to get out, quickly. Credit will be harder to come by if banks no longer take VCs at their word.

Sabow disagrees: Understanding a company’s backers — not just the funds, but the individual managers — remains key, and trust still cuts both ways. “That’s hugely important in lending decisions,” he says. “You can’t lend without it.” The VCs “are also doing due diligence on us. What do we do when things don’t work first time? Will we just take the keys?”

The answer to that question has to be: No. Aside from anything else, startups often don’t have anything tangible for a bank to sell – it’s not like seizing your house if you default on the mortgage.

For SVB, this is another advantage from its long history of banking Silicon Valley — and it’s a muscle that’s getting plenty of exercise right now. Cadieux told me his bankers have years of experience watching the progress companies make against their financial and business goals and knowing when a bit of extra funding can get them to the next milestone, or when the lenders and backers need to get involved to help it change course. If a company is never going to reach the next target, the bank’s job becomes a tricky balancing act to ensure it gets something back. It often means finding a way to keep key people interested when their dreams of becoming a billionaire tech-titan have evaporated; the intellectual property of a startup may be worthless without the people who created it.

The lender might not get all its money back, but giving some financial reward to the founders and maybe their backers gives a bank a better chance of recovering something rather than nothing at all. But those people also have reputational reasons for not just walking away. “There’s no shame in failure, but how you fail really matters if you want to do this again,” Cadieux says.

This is a fitting aphorism for SVB this past year as much as for startups. HSBC and other banks with new teams trying to pick winners in the venture capital world will need to remember it too if they want to build lasting franchises.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All