Fixed-income markets are back in a tizzy over inflation, thanks to the combination of rising risks for energy prices and strong retail sales data — both of which come on the heels of a higher-than-expected consumer price index last week. Still, it’s important not to conflate the three developments when assessing the prospects for Federal Reserve interest rate cuts, which probably remain in the cards despite the latest sequence of developments.

Yields on 10-year Treasury notes jumped as much as 14 basis points on Monday to 4.66%, the highest in five months, as March retail sales exceeded most economists’ expectations and global oil markets weighed the fallout from Iran’s direct attack on Israel over the weekend. The retail sales report, in particular, gave a fresh boost to the narrative that robust demand is now the main culprit for America’s lingering inflation problem. In fact, there isn’t much of a connection — not yet at least.

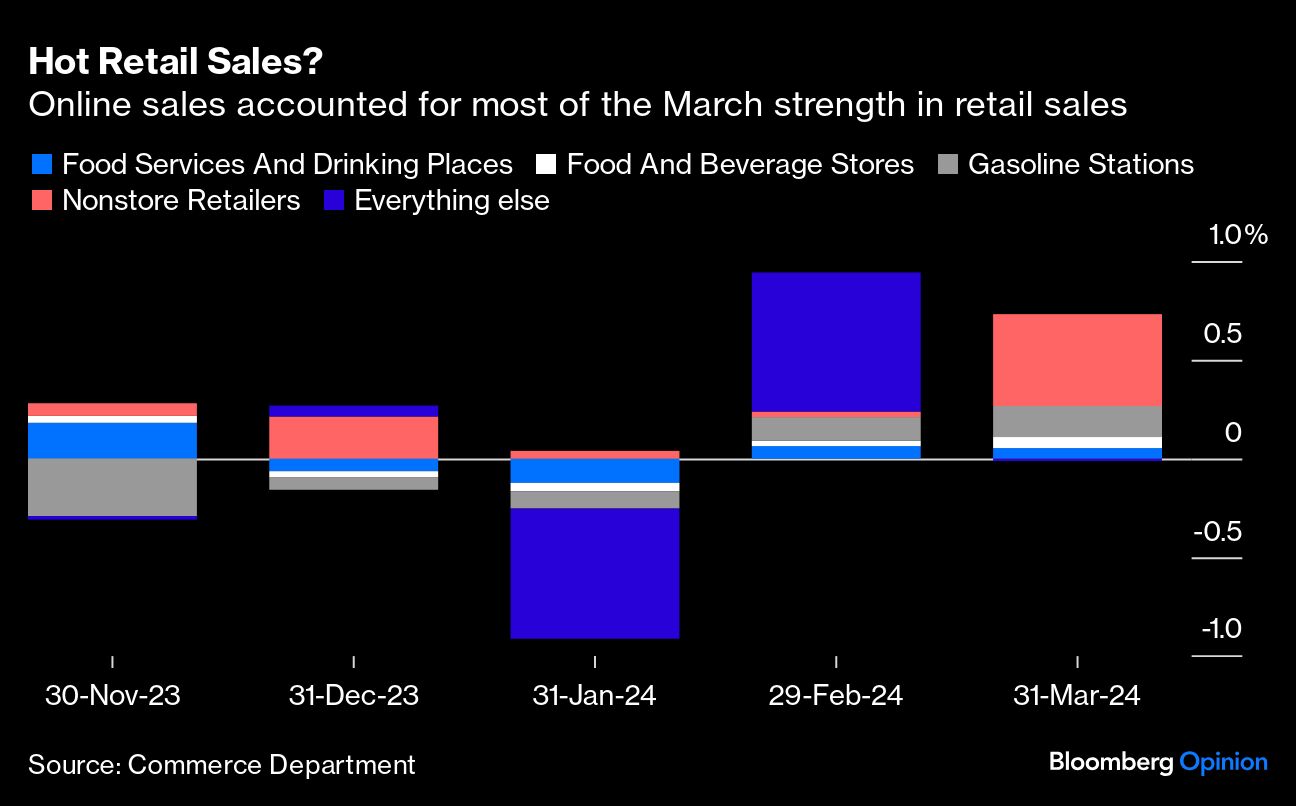

In Monday’s retail sales data, online spending was the primary driver of the upside surprise. In nominal terms, online retail rose 2.7% month-over-month, enough to account for about two-thirds of the 0.7% increase in the metric overall. Notably, if inflation were a story of excess demand, you might expect price pressures in the parts of the economy where spending has been strongest, but that hasn’t really been the case, so it’s hard to make the connection. In fact, nondurable goods prices ticked up just about 0.1% in March, and online prices measured in the Adobe Digital Price Index have performed comparably.

Energy prices are equally deceptive. At the time of writing, West Texas Intermediate was trading near $85 a barrel, from around $70 at the start of the year. Down just slightly from recent highs, markets and inflation-watchers remain on high alert amid concerns about an all-out war between Israel and Iran. But while energy prices have the potential to push up overall inflation, economic orthodoxy typically says that policymakers should usually look through such supply-driven factors, and there’s no reason to think that Chair Jerome Powell’s Fed would buck that wisdom. Oil shocks often come at the expense of other kinds of consumption, and central banks are generally helpless at fighting them, unless they coordinate in such a way as to essentially drive the global economy into recession and, in so doing, crush demand for fuel.

So what’s actually driving inflation?

The single-biggest reason that the consumer price index exceeded expectations in March was the surprise jump in motor vehicle insurance. Without that, core inflation would have met consensus expectations; bond market sentiment wouldn’t have taken this turn for the worse; and we probably wouldn’t be talking about this today.

While insurance is a very real pain point for Americans, it’s hardly the result of recent aggregate supply and demand dynamics. In fact, it mostly reflects the surge in used-car and parts prices from 2021 and 2022. Due to the heavily-regulated insurance market, it’s taken all this time for many insurers to push through premium increases, particularly in states such as New Jersey and California. Going forward, those pressures should be expected to abate a bit. To the extent that I’m being overly optimistic, it would be because of climate change, a worse-than-expected storm season and a wave of excessive litigation — factors that the Fed has absolutely no control over.

Later this month, the Bureau of Economic Analysis will release the core personal consumption expenditures deflator, the Fed’s preferred inflation gauge, and it won’t look quite as bad — partially because of the differences in how insurance1 is measured, and the lower weighting for the housing inflation category, which has been disinflating very slowly and should continue to do so.

On a month-on-month basis, core PCE is widely expected to have increased a not-terrible 0.3%, according to projections from Bloomberg Economics and Inflation Insights LLC based on information gleaned from the CPI and the producer price index. While that’s still not good enough to get inflation back to target in short order, the PCE has been dealing with idiosyncratic issues of its own — net foreign travel and portfolio management — that seem to be helping to push up the top-line, according to Inflation Insights President Omair Sharif.

The biggest risk in all of this is perhaps business and consumer inflation expectations: persistently elevated energy prices and the constantly negative news coverage of inflation still have the potential to become self-fulfilling prophecies, especially if this streak of bad luck drags on for another quarter or two. While I’m loath2 to make too much of it for now, the small sample-size University of Michigan survey indeed showed that consumers’ expectations for longer-run inflation are drifting higher again, a data point that’s unsettled policymakers in the past. If businesses start to think that “everyone else is doing it,” they might try to pad profit margins by pushing through additional price hikes. But to me, that’s a worst-case scenario, and recent history has revealed inflation expectations to be pretty well-anchored and much of the handwringing unnecessary.

I’ll be the first to admit that it’s becoming pretty lonely to be a dove in this early 2024 environment, but it’s ultimately too early to abandon the rate-cut thesis. Amid all of the hawkish sentiment, the influential Federal Reserve Bank of New York President John Williams told Bloomberg Television’s Michael McKee on Monday that, in his view, the process of bringing rates back to “more normal levels” would likely start later in the year. “We’re seeing restoring balance in the economy,” he said. “We are seeing a slow decline in inflation, so I do think monetary policy right now is in a good place.” He noted that while he would continue to watch the data closely, nominal interest rates were now quite a bit higher than inflation, generally a sign to central bankers that their policy is restrictive. That doesn’t mean that the narrative can’t change — especially if inflation expectations really get out of hand — but for now, it looks like the market is getting overly worked up about recent developments for the interest rate outlook.

1 In insurance, you pay a certain premium and get a certain amount back when you make a claim. In the PCE and PPI, it's measured on a net basis, where insurance "costs" are essentially premiums net of insured losses. In practice, that's meant that PCE/PPI vehicle insurance is up much less than CPI car insurance since the start of the pandemic.

2 Inflation expectations are a key part of how economists think about realized inflation and the practice of central banking today. But no one's figured out a perfect way to measure them. Consumers have wildly varying understandings of what inflation actually is, and even the best-designed surveys tend to be extremely noisy, with their usefulness to policymakers far from clear.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin