Meta Platforms Inc.’s record-breaking, artificial intelligence-fueled rally has added $1 trillion in market value since its darkest days of 2022, and yet by some perspectives it’s still trading at a discount.

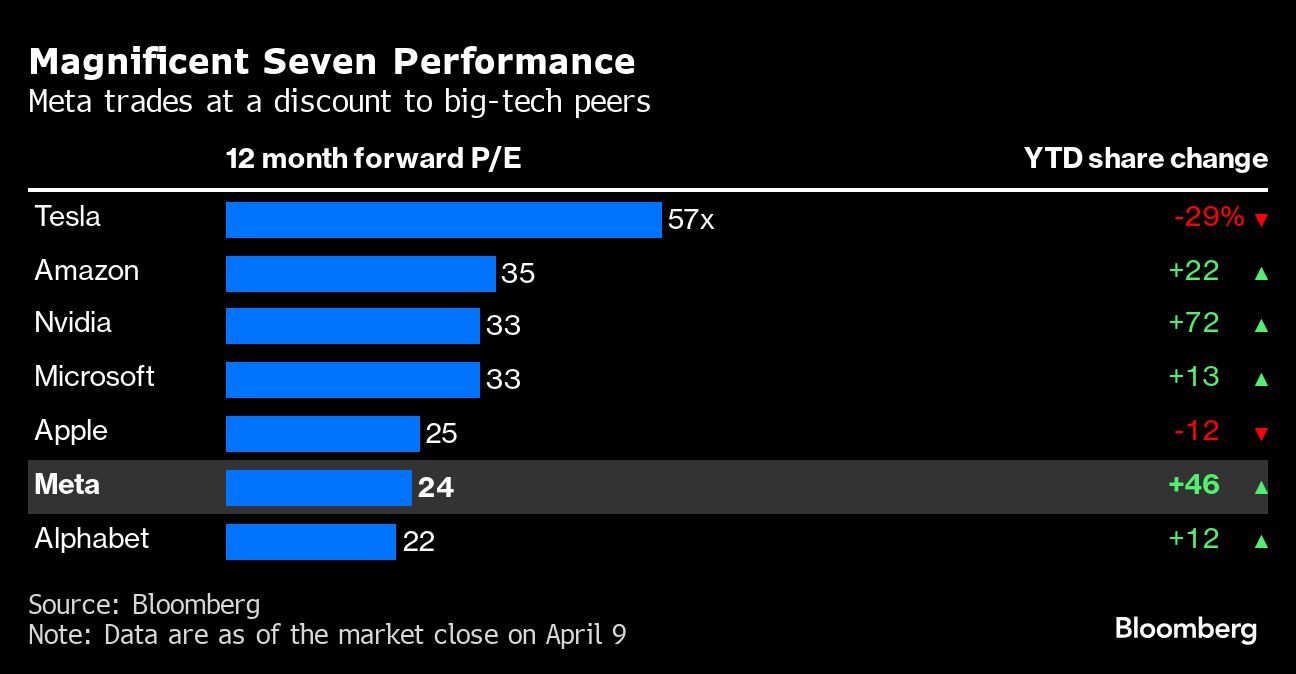

Its shares traded at 24 times estimated earnings early Wednesday, roughly in line with their 10-year average and just below the 25 times of the Nasdaq 100. Among the Magnificent Seven group of big tech companies, only Alphabet Inc., with a multiple of about 21, is cheaper.

Artificial intelligence is the biggest driver of gains and the largest future tailwind investors see for the stock. Meta has been heavily investing in AI to improve ad targeting and recommend content to its massive user base, a bet investors see paying off big time. Profits tripled in the social media giant’s most recent quarterly report while revenue growth surged. The earnings were so strong that Meta also announced a $50 billion buyback program and implemented a dividend.

“Outside of chip or hardware companies like Nvidia or Dell, no company has benefited more from AI than Meta, just in terms of the impact on growth,” said Conrad van Tienhoven, a portfolio manager at Riverpark Capital. “There’s been a clear shift in Meta’s ability to target and measure ads through AI, and executing on this has set the company up for another five to seven years of growth.”

Meta has soared more than 450% from its nadir almost 18 months ago, including a gain of about 46% this year that’s behind only chipmaker Nvidia Corp. among the Magnificent Seven.

The selloff that preceded the current rebound erased more than three-fourths of Meta’s valuation and featured a historic wipeout in market value, largely due to concerns over spending on the its metaverse initiative. While the Menlo Park, California-based company continues to invest in that virtual reality world, it also made cost cuts a focus, dubbing 2023 the “Year of Efficiency.”

“Meta has figured out how to get rid of unnecessary spending, which has been a real balance sheet plus, and it continues to innovate. If you’re late to the game, there’s always some drawdown risk buying this high, but I don’t see a reason to get out,”said Rick Bensignor, chief executive officer of Bensignor Investment Strategies and a former Morgan Stanely strategist. “When I look out five or 10 years to where Meta could be, it still looks like a great core holding that is trading at a very favorable price.”

Of course, investors looking for exposure to ad revenue could also snap up Alphabet, which has a cheaper valuation and has gained about 12% this year, a much more modest performance than Meta’s rally. Though Wall Street is bullish on both names, average price targets signal that analysts see slightly more upside for Alphabet at current levels, according to data compiled by Bloomberg.

However, Alphabet continues to face investor skepticism over its AI products and ability to translate them to growth. Meta is expected to deliver bigger revenue gains this year, with estimates at 17%, compared with 12% for Alphabet. Net earnings growth at Meta is expected to be roughly twice as strong.

RBC Capital Markets wrote that Meta is “clearly outperforming” Alphabet, its biggest rival in the market for digital advertising, citing its own analysis of spending in the digital ad industry in an April 3 note. RBC raised its price target on Meta to $600 from $565, saying that its outperformance over Alphabet prompts a higher multiple.

Meta is scheduled to report its first-quarter earnings results on April 24 after the market close. Top of mind for investors is ad revenue growth, how AI solutions are working and how the company can monetize products such as Reels.

“I’m dying for updates on all of that,” said Scott Acheychek, CEO of Rex Shares LLC.

Meta’s dominant position has also been put into sharp relief by struggles at its social-media peers. Both Pinterest Inc. and Snap Inc. have reported weak sales, putting the stocks in negative territory for the year, while the newly public Reddit Inc. has failed to generate much excitement from analysts.

Bernstein’s Mark Shmulik wrote that mid-sized social platforms could be “structurally disadvantaged and too sub-scale to compete” in Meta’s shadow.

“What hope is there for the smaller social players including Reddit to reach engagement, monetization, and profitability levels seen over at Meta — the North Star?” he wrote, starting coverage on Reddit with an underperform rating.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.