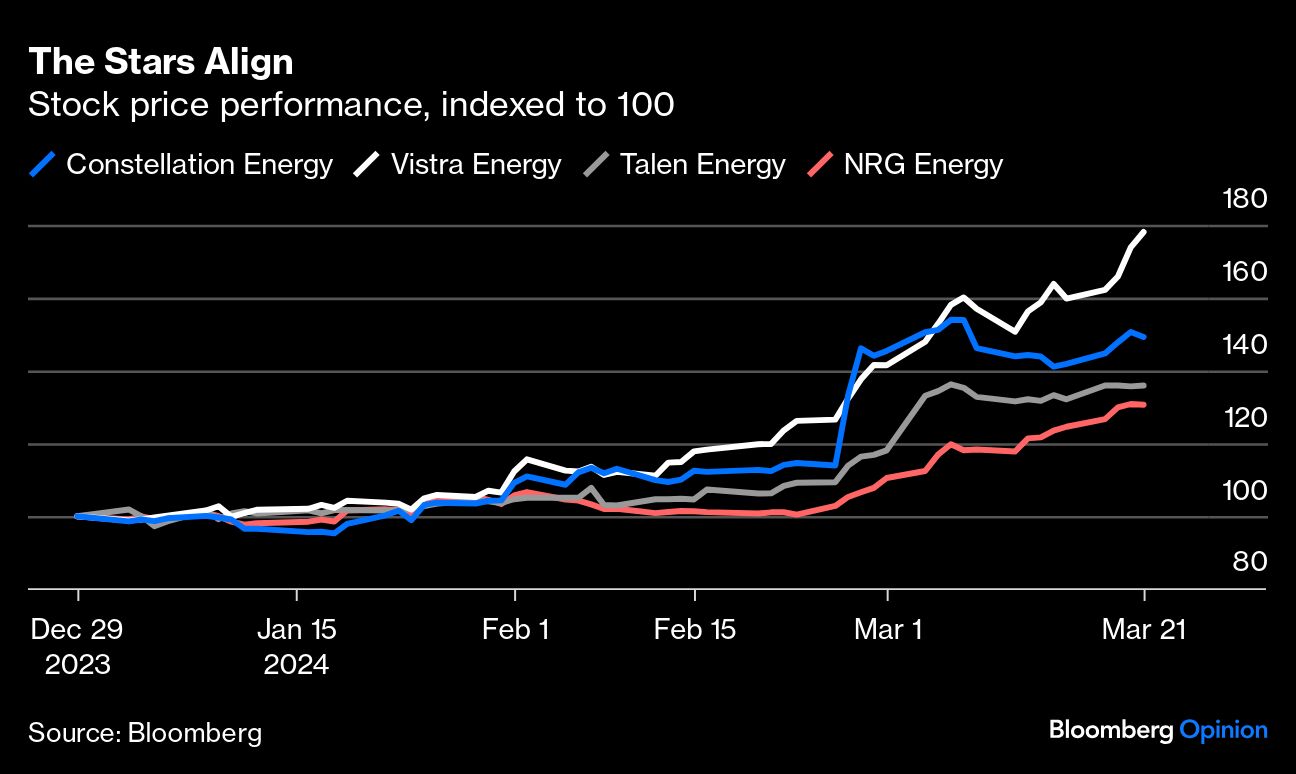

Artificial intelligence is shining its aura on one of the most benighted corners of the stock-market. While two AI hardware firms top the S&P 500 leaderboard so far this year — Super Micro Computer Inc. and Nvidia Corp. — a close third is Constellation Energy Corp., which runs the sort of nuclear power plants that were cutting edge maybe half a century ago.

While human intelligence needs regular doses of water, snacks and sleep, the artificial kind devours electricity pretty much non-stop. Forecasts of US data centers’ power consumption tripling by the end of the decade have sparked life into the stocks of independent power producers, or IPPs, like Constellation. Their rally heralds a profound shift in US energy, with implications extending to nuclear power, the wider grid and household electricity bills.

As revivals go, this is Lazarus level. The last time IPPs — which produce and sell wholesale electricity competitively, distinct from regulated utilities — were this hot was about 25 years ago. Deregulation in the 1990s spurred a frenzy of power-plant construction and electricity trading that reached an apotheosis (of sorts) with Enron Corp. Then came a combination of regulatory backlash, cheap shale gas — which sunk power prices — and electricity demand flatlining after 2007. Many IPPs fell into bankruptcy and investors largely deserted the sector (see this). To understand how unloved they were, consider that Vistra Energy Corp. is up 78% this year — and still trades at only about 8 times forward Ebitda with a free cash flow yield of nearly 13%.

Such metrics offer some comfort that IPPs aren’t yet into bubble territory.

Perhaps more importantly, there is an actual deal to point to between Big Tech and a power generator. Talen Energy Corp. announced earlier this month that it was selling a datacenter, co-located with a nuclear power plant in Pennsylvania, to Amazon.com Inc.’s web services arm. Amazon also signed a long-term power supply agreement with the plant at an undisclosed price but assessed by analysts to be in the $70-per-megawatt-hour range, a significant premium to prevailing electricity futures, which are more like $40 or $50. That premium likely represents a mix of implicit carbon pricing — since nuclear power is emissions-free — and an expectation of rising power prices in general, says Andy DeVries, a utilities analyst at CreditSights.

Co-located nuclear power is tailor made for AI, given reactors run about 90% of the time and so do datacenters. Being onsite also means avoiding the hassle and costs of using the local grid: While $70-ish would be a premium to current wholesale electricity prices, it is way lower than average commercial tariffs on grid-supplied power, more like $110 in Pennsylvania. This is clearly an intriguing opportunity for other IPPs with nuclear plants, such as Constellation and Vistra.

Talen’s deal also jerked life back into the moribund shares of NuScale Power Corp., the floundering developer of small modular reactor, or SMR, technology — though only briefly. Having virtually tripled, seemingly on hopes of an AI-led shopping spree for SMRs, it fell back again as folks presumably remembered NuScale’s costs and cash burn after its US pilot project was canceled last year (see this).

Still, AI’s potential impact on SMRs is a fascinating topic, not least because, like electricity demand writ large, nuclear power’s prospects have looked so poor for so long. One thing holding back a new wave of reactors is that they usually require some sort of government help — such as loan guarantees or cost-recovery in utility bills — to offset the risks around construction and power prices. But if any industry has a need for reliable, decarbonized power and the balance sheet to commit to long-term supply contracts, it is Big Tech.

For now, this is mere speculation. Datacenter owners are, by and large, not yet considering nuclear power, according to comments from Marc Ganzi, chief executive of DigitalBridge Group Inc., which develops and invests in IT infrastructure, during a recent NextEra Energy Inc. analyst conference. Ganzi has stressed, however, that his customers — behemoths like Nvidia and Microsoft Corp. — want the sort of “energy independence” that comes with co-located data centers or self-contained microgrids. These offer not just lower-carbon energy but also a hedge against the strains that test, and occasionally overwhelm, the US power grid.1

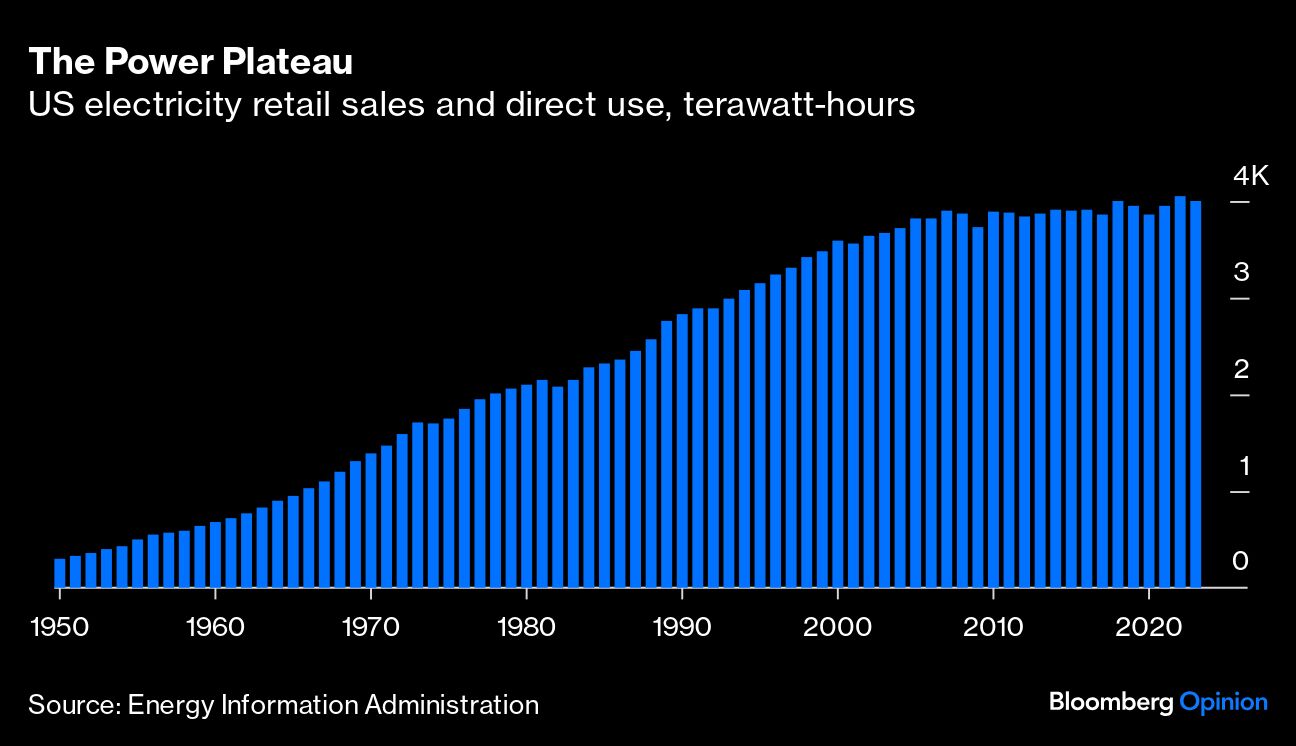

This need for energy insurance adds a further layer of complexity here with ramifications for our entire energy system. As it stands, estimates of extra power demand from data centers by 2030 add up to about 5-6% of current US electricity consumption — which hardly seems a huge shift in the needle.

Datacenters are, however, just one, acute element of a broader transformation. Consider: if data centers take an extra 200 terawatt-hours of demand by 2030, that would be the equivalent of 46 million electric vehicles on US roads.2 Since Bloomberg NEF projects 42 million actual EVs on US roads then, that is like doubling the fleet. Beyond transportation, the energy transition requires the electrification of industrial processes — including exotica like producing hydrogen — and heating via the mass deployment of heat-pumps. These all offer tremendous efficiency gains versus combustion of fossil fuels but also demand green, affordable, reliable electricity.

In that context, the proliferation of data centers as AI takes off should be seen as the vanguard of a broader revival in electricity demand. Renewables development should benefit broadly given Big Tech’s net-zero goals. Yet nuclear and natural gas should also benefit to some degree from reliability concerns — which in turn can cut both ways for traditional utilities managing grids. The other side of the coin is the challenge posed as incoming demand finally moves a needle that’s been dead for the best part of two decades.

1"The problem isn't that the US and Europe cannot create enough generation capabilities, we can generate power. But ultimately, it's our ability to transmit power, interconnect that power and then bring it into a high-density environment like a data center... Our ability to generate energy independent holistic solutions for our hyperscale customers is where we're going. If we can do that, again this is looking around corners. This is the next paradigm shift in digital infrastructure." (Marc Ganzi, CEO, DigitalBridge Group speaking at Deutsche Bank's annual media, internet and telecom conference, March 11, 2024).

2This assumes each EV travels 13,000 miles per year at an average efficiency of 3 miles per kilowatt-hour, resulting in annual power consumption of 4.33 megawatt-hours per vehicle. This is a modified version of a calculation made by Andy DeVries, utilities analyst at CreditSights.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.