While investing strategies should be consistent, changes in markets and the economy make some advice more relevant than it was in the past. Below are the top 10 things I’m telling clients:

While investing strategies should be consistent, changes in markets and the economy make some advice more relevant than it was in the past. Below are the top 10 things I’m telling clients:

1. Get real! Many clients have come to me recently heavily invested in bonds yielding 4% to 5%. In fact, some say they can live off the income and never touch principal. I hate to burst people’s “feel good” bubble, but my advice is to “get real,” as in after-tax, inflation-adjusted thinking. After taxes, they may be getting 2.7% to 3.3% and most, if not all, of that will be eaten up by inflation.

Treasury Inflation Protected Securities (TIPS) solve the inflation part of the misconception, but not the taxes. Though TIPS offer a 2% real yield, they are taxed on nominal returns. So, if we end up with high inflation, taxes could eat up most or all that return.

2. You have a ton of cash and that is your riskiest asset. The old and rather dark story goes that if a frog is dropped into a pot of boiling water, it will jump out. But if the frog is dropped into a pot of nice comfortable cool water that is slowly heated, it will not notice the gradual change in temperature and will stay in the pot until it boils.

Holding cash is, metaphorically speaking, like that frog in the pot of cold water. It felt great in 2022 when both stocks and bonds had large losses, but the pot has been heating up since then. The inverted yield curve has some cash and money market accounts earning 5%, though that’s unlikely to last as the Fed has signaled it will lower the Fed funds rate this year, which will impact cash and money market yields. The markets will control intermediate and longer-term yields. I’m telling clients to minimize cash or, in other words, jump out of that pot before it starts to boil.

3. Your goal is not to die the richest person in the graveyard. More often than those who are heavily in cash and bonds, many clients come to me with very aggressively weighted stock portfolios. It’s predictably irrational behavior. In bear markets I see people more conservatively invested, and in bull markets like we have today it’s the opposite. There are two factors at play in this dynamic. The first is that inertia results in low stock exposure in a bear and high stock exposure in bulls. The second is that we time markets poorly. Data shows this is especially true for advisors.

I acknowledge to clients that stocks are likely to outpace bonds in the very long run yet urge them to look at the consequences should we have a grizzly bear rather than these teddy bears we’ve had in the last quarter century. As fellow Advisor Perspectives author William Bernstein puts it, “if you’ve won the game, stop playing.” I tell clients to take some risk off the table if they’ve won the game.

4. No, you won’t have nerves of steel after a stock plunge. When I see a client with an unnecessarily risky portfolio, it often follows that they are sure they will have the courage to rebalance when the bear market comes to wreak investing havoc. That’s a bright red flag as it reveals they haven’t thought through the pain they would be feeling with the next bear, which will be caused by something that has never happened before.

The client who admits they only hope they would have the courage to rebalance has thought through some of those consequences such as not being able to buy that vacation house or send the kids or grandkids to college. I urge them to go back to their March 2020 statement and see if they rebalanced during the 33 days ending March 23, 2020, when stocks fell 35%. When someone comes to me with a 100% stock portfolio and feeling fearless, I won’t even take them on as a client.

5. Investing should oscillate between boring and painful. In bull markets, I have people come to me who are really enjoying their investing. That’s because it’s fun and exciting to look at the portfolio and those gains in up markets.

But during a bull market, all that is needed is occasional rebalancing. That’s not even in the same zip code as fun and exciting; it is a boring time to invest. The bear market, on the other hand, is painful and rebalancing during one is excruciating. That’s a very good sign. I tell clients they will likely get some pleasure, or at least some relief, from selling during a bear as it stops the pain. But pleasure in investing is a very bad sign.

6. You have a lot of funds; but you aren’t diversified. I see clients with dozens of mutual funds and ETFs. While this is an improvement over clients who once came to me with hundreds of individual stocks; it still isn’t very diversified.

I argue that with one total U.S. stock index fund and one total international stock index fund, investors are as diversified as they need to be. Buying a non-total fund such as a value fund is picking parts of the market to outperform on a risk-adjusted basis. Naturally now I’m seeing more clients come to me overweighted in large-cap growth-tech stocks. And, of course, William Sharpe’s Arithmetic of Active Management proves an ultra-low-cost, cap weighted, total-stock index fund must beat the average dollar invested in active management, which translates to a virtual certainty to beat most investors.

7. Bond funds are not riskier than bonds. Since the “bond bubble” burst in 2022, many clients want bonds instead of bond funds. They tell me that’s because they know they will get their money back. While true, it’s an illusion since no one knows how much spending power it will provide. Mathematically, if you own a five-year bond within a fund or directly, the economic loss from a rate increase is the same.

I pose this question to clients: “How could a laddered bond portfolio of thousands of bonds be riskier than owning a few dozen?” Clearly there are some times bonds are better than bond funds such as holding TIPS until maturity. And now, some bond funds present an opportunity to recognize income as a long-term capital gain.

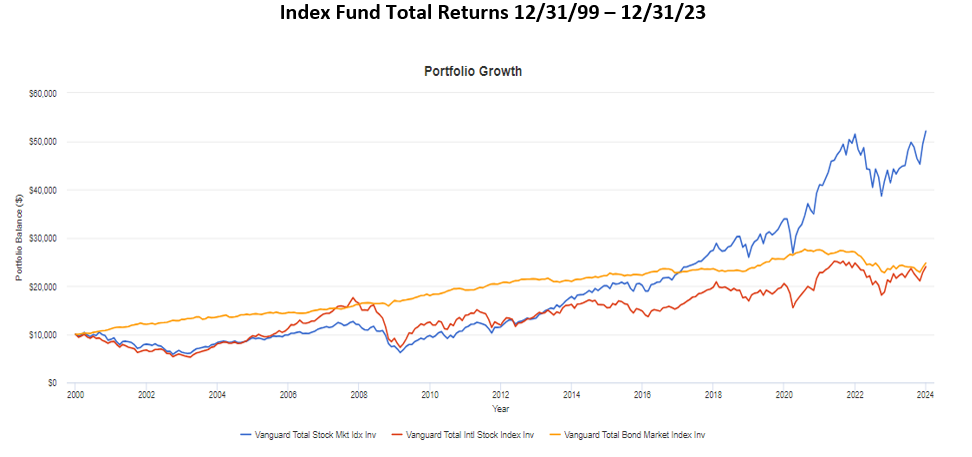

8. High-quality bonds and bond funds are not risky. The worst year in the history of the bond market was 2022, as rates surged in response to high inflation. Statistically speaking, it was the equivalent of the stock market plunge during the Great Depression. The iShares Core US Aggregate Bond ETF AGG total return was -13%. The silver lining was that it ended with the opportunity for investors to get higher yields. I’m not suggesting being greedy and buying long-duration bonds (as both Schwab and Silicon Valley Bank tried).

But with a little perspective, that 13% loss in a year was less than the 20% loss in the stock market on black Monday in 1987. The following chart comparing stocks to bonds puts that bond bubble in perspective compared to stocks.

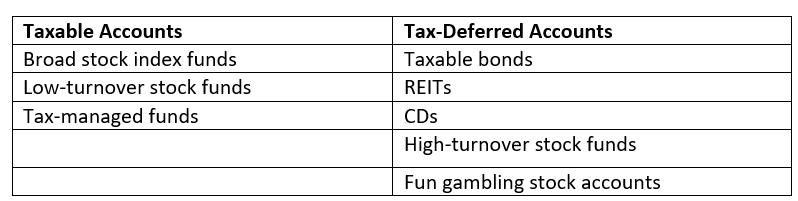

9. Your assets are not located in the most tax-efficient manner. Equities should go in the taxable and tax-free accounts first, but asset allocation always comes before asset location. REITs and stocks are best held in Roth accounts.

Even CPAs get this wrong. We are taught that stocks are for the long run and 401K(k)s and IRAs are for many years into the future. But owning stocks in tax-deferred accounts turns a long-term capital gain into ordinary income at higher rates. Owning stocks in the taxable account generally throws off less income than bonds and that dividend income is taxed at a lower rate.

10. I’ve always said investing was simple; I never said taxes were. While I believe in the keep it simple stupid (KISS) principle, taxes never fail to complicate things. My own portfolio is far more complex than I’d like. Far more complex than the asset location mentioned above are analysis of what to sell and when as well as withdrawal strategies.

Taxes present opportunities such as capturing dividend income and long-term capital gains at a zero-percent tax rate. Yet they also present costly traps such as one dollar of extra income costing thousands of dollars by triggering the next tier of the Medicare income-related monthly adjustment amount (IRMAA). That’s why I review a client’s tax return to find opportunities and avoid tax traps. I also find ways to contribute to charitable causes in a more tax-efficient way as well as some things the clients’ CPA may have missed such as neglecting to subtract U.S. government interest on the state tax return.

What I’m telling clients in 2024 is a lot of the same things I’ve been saying for years. But recent markets always cause me to emphasize some advice more. With the stock market near an all-time high, I emphasize different things than in March of 2020 during the COVID plunge.

But one timeless nugget of wisdom is that consistency rules the day. Emotions and expenses are the enemy of the investor and advisor alike. I always tell clients “I don’t know the future and that is the single most valuable advice I’m giving you.”

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion-dollar companies and has consulted with many others while at McKinsey & Company.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Read more articles by Allan Roth

While investing strategies should be consistent, changes in markets and the economy make some advice more relevant than it was in the past. Below are the top 10 things I’m telling clients:

While investing strategies should be consistent, changes in markets and the economy make some advice more relevant than it was in the past. Below are the top 10 things I’m telling clients: