While bonds and bond funds are recovering a bit this year, 2022 resulted in large losses, whether you held individual bonds to maturity or owned a bond fund.

While bonds and bond funds are recovering a bit this year, 2022 resulted in large losses, whether you held individual bonds to maturity or owned a bond fund.

But, if you own bond funds in a taxable account, it is possible to turn some of the SEC yield into long-term capital gains taxed at lower rates, which could save a bundle. Here’s how.

Let’s look at the Vanguard Total Bond (VBTLX). As of December 12, 2023, it had an SEC yield of 4.61% but the distribution yield was only 3.49% as of December 1, 2023. Though off by 11 days, those dates are close. The SEC yield is roughly 1.11 percentage points higher than the distribution yield. The SEC yield of a bond assumes the investor holds the bond to maturity. In other words, the bond fund now holds bonds that are trading at a discount but, without defaults, will mature at par. Thus, some of the gain is from coupons and some from accretion of the principal.

Indeed, as of November 30, 2023, Vanguard shows the fund has an unrealized loss of 12.07% of the fund’s NAV. My hypothesis was that, all things being equal, the bond fund’s NAV would likely increase closer to the $100 par as the underlying bonds moved closer to maturity. I ran that by a Vanguard spokesperson who confirmed and replied:

As you pointed out, for bonds issued prior to the huge upswing in rates, the coupon is lower than the prevailing market rate, so they’re generally trading at a discount. For lower coupon bonds, less of the return will come from the coupon payment and more will come from capital appreciation going forward.

Next, I wanted to examine whether that expected increase in NAV would be considered a capital gain or ordinary income. Vanguard understandably declined to respond to this specific tax question.

Clearly, buying a bond directly at a discount would result in eventually paying taxes assuming the accretion of that discount was more than the 0.25% annually allowed by the IRS. Yet the vast majority of the 10,719 underlying bonds in this $302.4 billion fund (all share classes) were bought before the 2022 surge in interest rates which is why the fund shows a large unrealized loss.

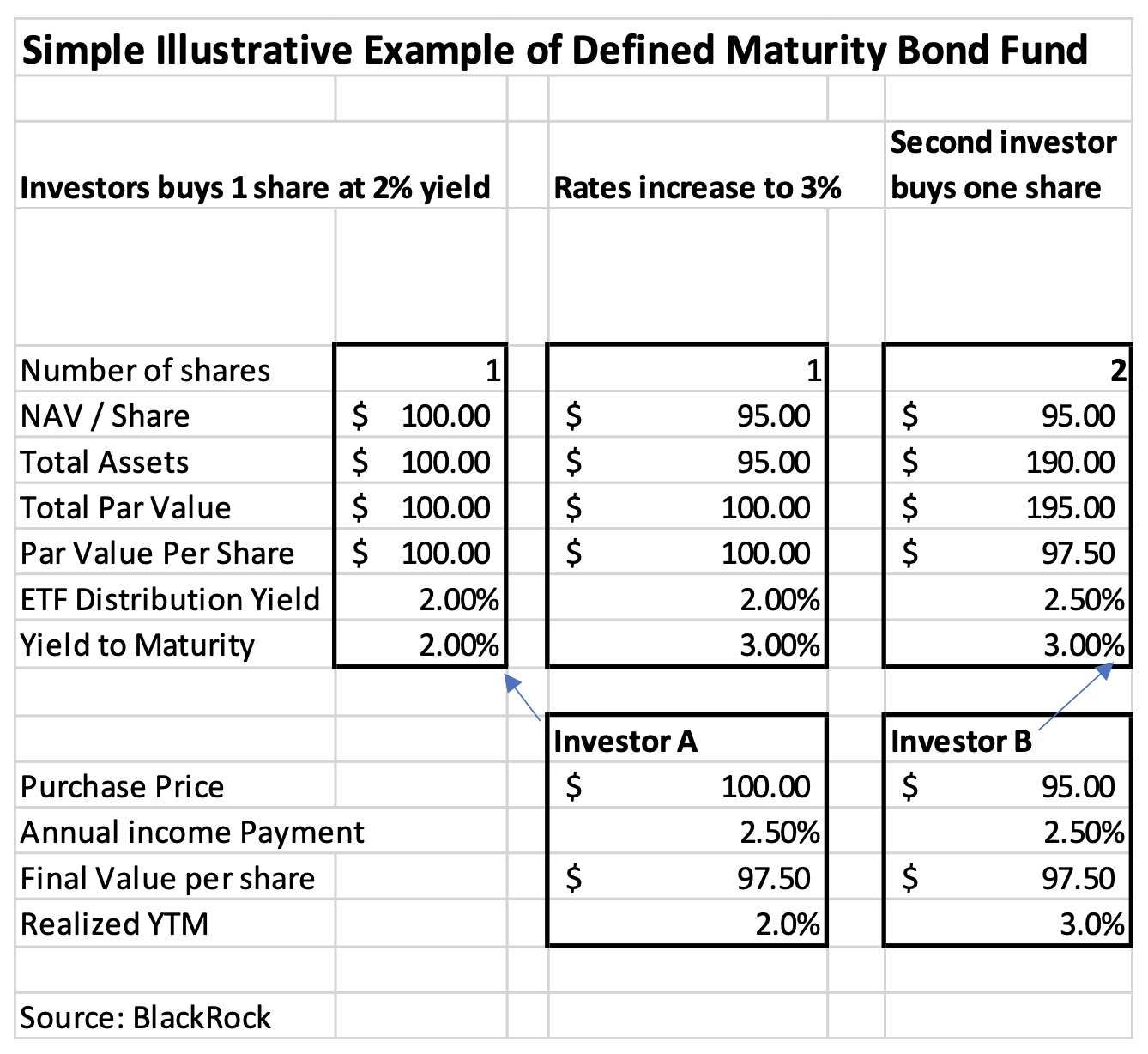

I turned to Karen Veraa, head of U.S. iShares fixed income strategy at BlackRock. She provided a document with this simple example. Understand that these numbers are rough and for illustrative purposes and assume the fund starts with one investor buying one bond.

Investor A buys a defined-maturity bond fund owning one 5-year bond bought at par ($100) with a 2% annual yield. Then rates immediately rise one percentage point to 3% and the value of the bond and bond fund decline by 5% to $95 a share. Investor B comes in and buys one share for $95 and will get a 3% yield to maturity. The fund buys a second 5-year bond for $95. Because that second bond is bought at a discount, the fund accretes that discount and pays out 3% on the second bond and 2% on the first, or a total distribution yield of 2.5%.

If no one moved in or out of this bond fund over the next five years, Investor A will get that 2% yield to maturity, but that will come in the form of a 2.5% annual distribution (taxed as ordinary income) and a capital loss in five years of $2.50, or about 0.5% annually. Investor B gets the 3% yield to maturity in the form of a 2.5% distribution yield and a capital gain in five years of $2.50, or 0.5% annually.

Investor B gets 0.5 percentage points of his 3% yield both deferred and taxed as a long-term capital gain as low as zero percent. The highest federal long-term capital gains rate is 20%, while the highest ordinary income tax rate is 37%. Possible net investment income tax (NIIT) applies to both, so that’s a wash.

Back to the real world

The conceptual example above from Blackrock explains the concept of how an investor can come into an existing bond fund with an unrealized loss and get some of their yield in the form of a capital gain.

Most bond funds aren’t defined maturity and maintain a relatively constant duration. And, as noted, the Vanguard Total Bond fund has hundreds of billions in bonds with an average maturity of 8.7 years and duration of 6.1 years. Most of those bonds were purchased at higher prices and, as they move closer to maturity, the underlying bonds will move closer to par. Net positive cash flows could cause the fund to buy bonds at a discount, raising the distribution yield, but it would be a much smaller proportion than the simple example where new money caused the fund to buy twice the number of bonds.

The 12.07% unrealized loss in the Vanguard Total Bond Fund would presumably decline over time if intermediate-term interest rates stay stable. Assuming the fund doesn’t experience huge inflows causing it to buy massive amounts of bonds at a discount, the vast majority of the annualized 1.11 percentage point differential between the SEC yield and distribution yield over the next year would come as a long-term capital gain. The investor gets a double benefit in both deferring the interest income (had they bought the bonds themselves) and paying those deferred taxes at a much lower long-term capital gains tax rate.

The same concept is true for any bond fund that has unrealized losses. The iShares Core U.S. Aggregate Bond ETF doesn’t release the unrealized loss of the underlying bonds in the fund but likely has a similar unrealized percentage loss as the Vanguard Total Bond fund as it follows only a slightly different version of the Bloomberg Aggregate Bond Index.

What this means

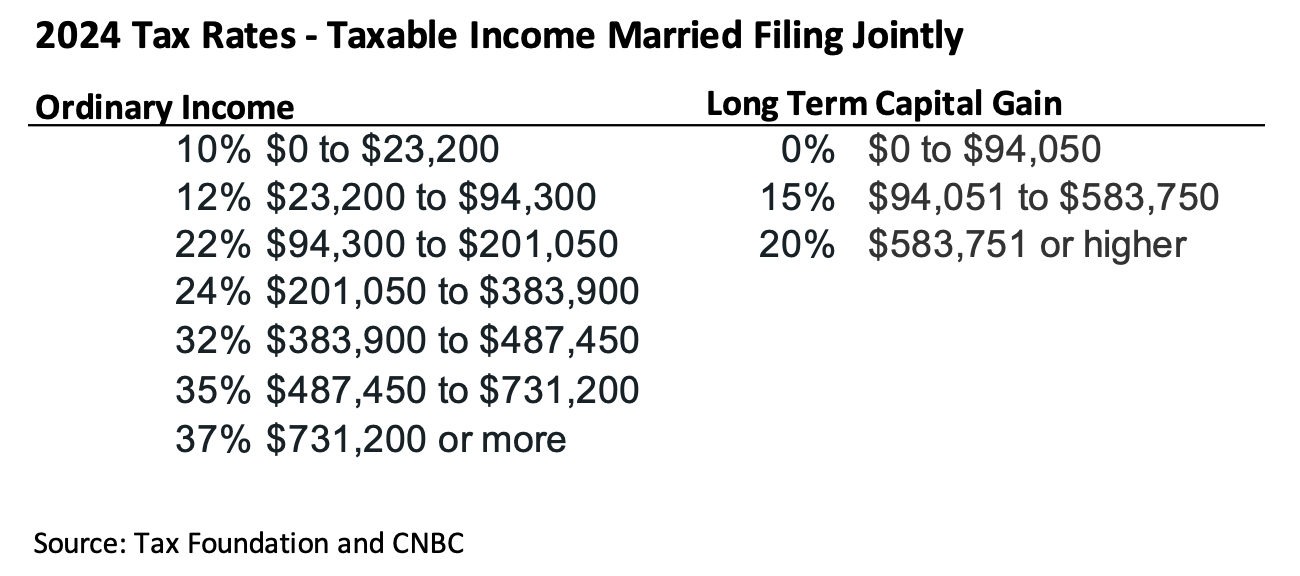

The tax savings with this strategy could be huge. Not only is part of the SEC yield on a bond fund deferred, but much of it could be taxed at a lower rate or even be federal tax-free assuming a long-term capital gain. For example, in 2024, a couple filing jointly with taxable income of 94,050 would pay no federal taxes. This means they could make at least $123 ,250 (including that long -term capital gain) given that the standard deduction is at least $29,200 that year. Even a taxpayer in the 37% marginal tax rate could cut the tax rate to 20%.

All of this is because when you buy an open-ended bond fund (either a mutual fund or an ETF) you don’t own the specific bonds. You own a percentage of the entire bond portfolio and, if the entire bond portfolio has losses, a new investor can harness some of those tax losses.

Of course, we don’t know what future intermediate-term interest rates will be and the top economists have a horrible track record in predicting those rates. If interest rates do increase over the next few years, this gain in NAV will not be realized. But the same would happen to a laddered bond portfolio that owned the bonds directly, assuming they reinvested in a new rung of that ladder when the existing bonds mature.

What this also means is, if rates go down and a bond fund has an unrealized gain with the distribution yield higher than the SEC yield, owning the bond fund would result in the investor recognizing higher ordinary income and deferring a capital loss. This was the case during most of the 40-year bull bond market.

Conclusion – Better than the Holy Grail

As someone recently told me, deferring taxes is the holy grail of tax planning. If that’s true, then this is even better because it both defers and substantially lowers the deferred tax bill.

I’ve always said investing is simple, but I never said taxes were. Check out the bond fund you are using and make sure it has an unrealized loss and had a substantial intermediate- to long-term bond portfolio before rates surged in 2022. Finally, confirm with your tax advisor that they agree with this tax treatment.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion-dollar companies and has consulted with many others while at McKinsey & Company.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Read more articles by Allan Roth

While bonds and bond funds are recovering a bit this year, 2022 resulted in large losses, whether you held individual bonds to maturity or owned a bond fund.

While bonds and bond funds are recovering a bit this year, 2022 resulted in large losses, whether you held individual bonds to maturity or owned a bond fund.