As Federal Reserve officials prepare for an in-depth conversation about its balance sheet at next week’s meeting, Wall Street strategists can only agree that all of the plans being discussed by the central bank carry some growing risks.

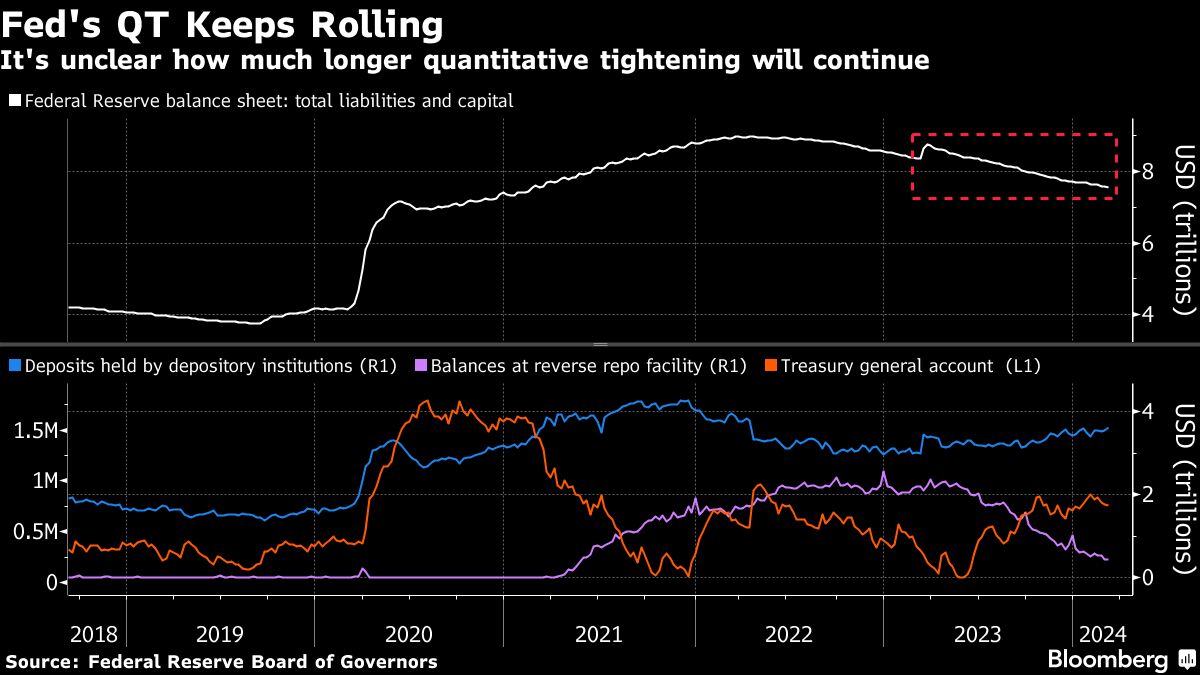

While a handful expect the Fed to announce or even begin slowing the unwind of its balance sheet — a process known as quantitative tightening, or QT — as early as May, others don’t see a tapering starting until the second half of the year. The divergence comes from the myriad variables that could affect the timing of slowing QT, from the drainage of the reverse repurchase agreement facility to the emergence of funding strains brought on by a scarcity of bank reserves.

Policymakers like Dallas Fed President Lorie Logan have said the central bank will likely be able to slow the pace at which it shrinks the balance sheet as the RRP facility empties, and slowing the pace doesn’t mean the central bank will stop QT altogether. Central bankers in 2019 learned a lesson when a different overnight market rate soared five-fold to as high as 10% and the central bank was forced to intervene.

“We’re nearing a point where QT starts to exceed the reduction in the Fed’s reverse repo facility and liquidity starts to drain as a result,” Peter Boockvar, chief investment officer at Bleakley Financial Group wrote in a note to clients. “That is more relevant now than whether the Fed cuts once, twice, three times or not at all this year off a 5.33% effective fed funds rate.”

One issue Wall Street is largely in agreement with is that when the time comes to taper QT, the Fed will lower the reinvestment cap for its Treasury holdings to $30 billion per month from $60 billion per month. Otherwise, Deutsche Bank and RBC Capital Markets see tapering starting around July with QT stopping sometime in the first half of 2025. Yet Barclays Plc and TD Securities expect the central bank to only slow the runoff before stopping altogether after about three months — their QT start dates vary.

What the Strategists Say

Bank of America (Mark Cabana, Katie Craig)

- Base case is QT slowdown in May but a slower pace of RRP depletion would mean a later timing of the tapering.

- See $200 billion to $250 billion threshold as the Fed’s key for the RRP and expect that level to be breached in 3Q 2024, driven by the April tax date and build in the Treasury General Account come from bank reserves instead of the reverse repo facility, in addition to Bank Term Funding Program repayment and official guidance on QT preferences.

- Debt limit could temporarily reverse effects of QT later in the year as the TGA will have to drop, which would mean less bill supply and easier funding.

Barclays (Joseph Abate)

- Now sees the Fed beginning to slow down its balance sheet unwind in September and concluding QT by the end of the year.

- Timing remains a mystery due to various outstanding questions, including how long the Fed wants to taper rolloffs before ending them, at what level reserves move from ample to scarce and what happens to the distribution of reserves across banks.

- Still expects RRP to be empty at the end of April, but ending QT will depend on where fed funds and SOFR are trading relative to the Fed’s administered rates, and liquidity conditions.

CreditSights (Zachary Griffiths)

- Base case is Fed announces it will begin tapering its QT program in June, and absence of market stress and a strong economy could make for a longer taper this time around.

- Analysis suggests Fed has another 12-18 months of balance sheet runoff at the current pace before bumping up against prior QT cycle lows.

- By the time the Fed started tapering QT in early 2019, there were already mounting pressures in short-term funding markets, including repo rates moving above the upper fed funds limit toward the end of 2018.

Deutsche Bank (Steven Zeng, Matthew Raskin, Brian Lu)

- Fed to continue unwinding its balance sheet at the current pace until balances at the RRP reach $100 billion to $150 billion this summer, which is sometime around June/July.

- At that point, QT will likely continue at a reduced pace into 2025.

- Cite various indicators that suggest reserves remain abundant and funding stress is low, from measures of liquidity relative to GDP, recent Fed survey results, reductions in leveraged short positions, and narrow range of SOFR distributions.

Goldman Sachs (Praveen Korapaty and others)

- Continue to expect a slowing of QT runoff starting in May.

- Range of indicators suggest system-wide liquidity may still be “sufficiently” above scarce levels, suggesting limited urgency to adjust the QT pace and banks haven’t used emergency liquidity provision facilities like the Standing Repo Facility “in significant amounts” in recent months.

- But RRP balances continue to decline rapidly and officials signaled they’d rather slow the pace of QT before facility is completely depleted.

JPMorgan (Teresa Ho and others)

- Fed will announce slowing of QT at the June meeting to begin in July with a reduction in Treasury runoff to $30 billion from $60 billion.

- Expects process to run through end-2024, stopping when overnight RRP balances drop TO $300 billion and bank reserves are $3 trillion.

- On balance sheet composition, “the Fed will not begin actively reinvesting its MBS paydowns to keep its balance sheet stable until early-2025” while “it would take years to reweigh the SOMA in line with the overall Treasury market duration.”

Morgan Stanley (Efrain Tejeda)

- Sees Fed initiating taper in June, moving the Treasury cap to $30 billion from $60 billion while leaving the MBS level unchanged at $35 billion.

- Expects QT to end in early 2025 when reserves are about $3.2 trillion.

- “Significant uncertainty surrounds the ultimate size of the balance sheet and the end of QT, and the Fed has clearly said it will monitor market conditions to determine when to stop,” citing SOFR-IORB spread, usage of the Standing Repo Facility as indicators of reserve scarcity.

NatWest (Jan Nevruzi, John Briggs)

- Base case is for Fed to begin tapering QT in June and running through September, but are also seeing increasing odds the Fed will simply slow pace of balance sheet rundown and continue through the year.

- Still, expect June taper start because “the Fed doesn’t really have to (and likely doesn’t want to) figure out how far QT can go through a trial and error process - there is no need to relive the repo spike of 2019 and the Fed will likely err on the side of caution.”

- Depleting RRP “is in the cards for sometime this year.”

RBC Capital Markets (Blake Gwinn, Isaac Brook)

- See Fed starting to taper QT in July and fully stopping in the first half of 2025, with risks of an even longer timeframe.

- Any market impact of the tapering timing/speed should be isolated to the front end given that it’s almost entirely a bill supply story.

- Risks to earlier end to QT do still exist, the biggest may be related to the uneven distribution of reserves and small- or medium-sized banks start experiencing scarcity even as the aggregate supply remains abundant.

- Standing Repo Facility and greater adoption of sponsored repo “do help lower (but don’t eliminate) the risk of acute shortages in underlying liquidity or balance sheet capacity.

SocGen (Subadra Rajappa)

- Believes Fed will wait until mid-year to lower SOMA cap on Treasury run-off from $60b to $30b, announcing in May and starting in June.

- “A slower run-off pace will help the redistribution of liquidity and enable the Fed to continue QT for longer.”

- Sees Fed continuing to run off balance sheet until QT stops in early 2025.

TD Securities (Gennadiy Goldberg, Molly McGown)

- Expect the Fed to start tapering QT in May and be “fully discontinued” in August, though recent official comments hints that tapering period may be longer than markets currently anticipate.

- Rapid decline in RRP usage underscores the need for the Fed to release a plan on QT soon, and with reserves now just 12% of GDP, policymakers need to clarify how large a buffer they intend to hold above the minimum level.

Wells Fargo (Michael Pugliese and others)

- Fed will announce plan to slow QT at its June meeting, though wouldn’t be shocked if officials moved announcement to May.

- Expect runoff caps to be reduced to $30 billion for Treasuries and $20 billion for MBS on July 1, with the slower pace running until end-2024.

- Sees RRP balances at $200 billion by year-end with bank reserves around $3.1 trillion.

Wrightson (Lou Crandall)

- Sees Fed announcing QT tapering at June meeting, effective with July rollover — to $30 billion from $60 billion for its Treasury holdings — with the risk that the process is more drawn out than assumed.

- Risk of later start date even higher as Fed officials don’t see this as a pressing issue in the near-term, and developments in the front-end argue for waiting longer before slowing pace of runoffs.

- Cash draining from RRP facility is spilling back into the banking system, which may have led to a softening in overnight unsecured rates and banks would be more willing to shed reserves.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Alexandra Harris