Less than a year ago, investors were gaming out what would happen when billions of dollars of bonds reached maturity dates, leaving borrowers potentially crushed by costly refinancings. Now, those fears are fizzling away, with companies rushing to sell debt to a buoyant market.

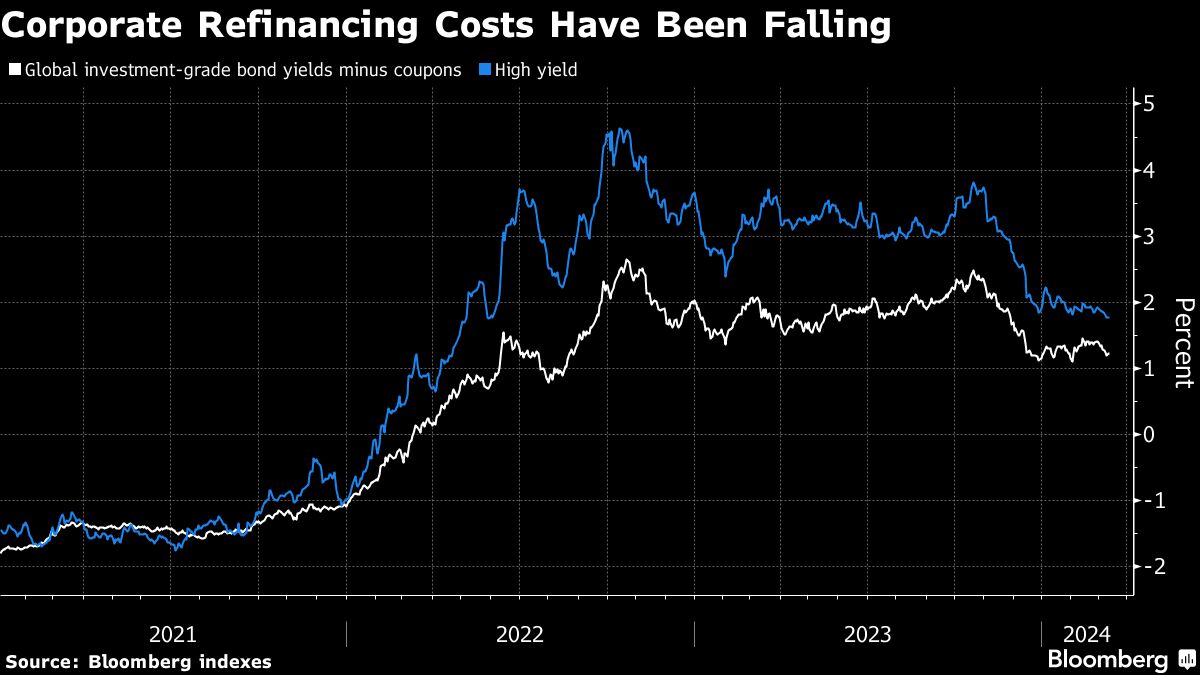

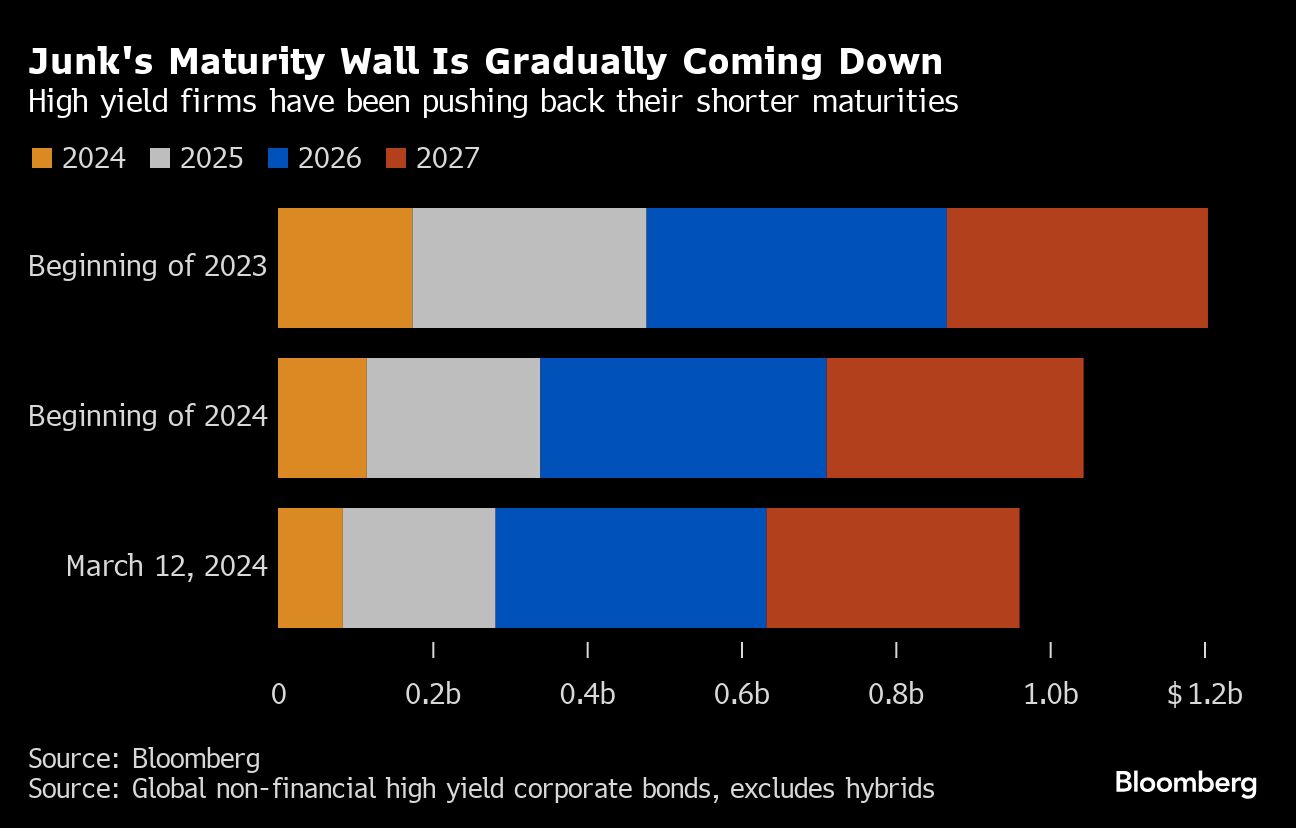

The implied cost of refinancing junk-rated bonds is now at its lowest since May 2022, based on global corporate bond indexes compiled by Bloomberg. For investment-grade firms, it’s the cheapest since summer 2022, when a series of central bank interest rate hikes was just beginning. Those falling costs have spurred a wave of corporate bond sales and, in turn, pushed back the so-called maturity wall of debt coming due.

The turnaround has come as rate cuts are built into forecasts for the summer, lowering underlying borrowing costs and creating a risk-on mood among investors — many of whom have piles of cash to put to work. And companies are seizing on the ebullience while it lasts, with the supply of corporate bonds globally now running almost 30% ahead of last year and — by a narrow margin — the fastest pace in more than a decade, based on data compiled by Bloomberg.

“The ‘refinancing penalty’ is still high, but significantly lower than it was last year. In the short term that makes supply more likely,” said Viktor Hjort, global head of credit strategy and desk analysts at BNP Paribas. Refinancing rates are no longer at the level that would have destabilized businesses, he said.

By Bloomberg’s analysis, a company selling junk-rated bonds to replace existing ones would now add 177 basis points to its annual interest bill, compared with 463 basis points in October 2022. That’s calculated by looking at the difference between the coupon companies pay on existing debt and the yield, which is used as a proxy for the cost of tapping the new issue market. It’s a similar picture for investment grade debt.

The upshot has been a boom in sales of new corporate bonds, with JPMorgan Chase & Co. calling issuance in Europe “relentless” over the past month. “This has, bluntly, taken us by surprise,” wrote strategists including Matthew Bailey.

It’s especially reassuring for lower-rated companies that need to refinance debt they sold during the easy-money era. Junk issuers generally aren’t as diversified as their investment grade peers in terms of the range of maturities in their debt stack, according to Federated Hermes senior portfolio manager Nachu Chockalingam.

Refinancing “has a bigger impact in high yield as a larger chunk is taken out,” Chockalingam said. “The market typically doesn’t want debt to become current, that is less than 12-months long. If companies are taking that away, investors are quite happy.”

To be sure, some firms may still struggle. Debt costs remain elevated, with a high degree of uncertainty about the timing of rate cuts and the macroeconomic outlook. Yields on global high-yield bonds are more than a percentage point above their five-year average, which could prove too expensive for some.

Overall though, the picture is brighter, with companies now facing less immediate debt needs.

At the start of last year, global non-financial companies with at least one junk rating had just over $300 billion bonds maturing in 2025 — a total that has now been slashed to under $200 billion. And companies are also dealing with debt due in 2026: they’re staring down a maturity wall of about $350 billion for that year, down from around $390 billion at the start of 2023.

“Companies have been able to term out their debt,” said Mohammed Kazmi, portfolio manager and chief strategist at Union Bancaire Privee. “It’s not a wall but a staircase as companies have taken the opportunity to access the new issue market.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Tasos Vossos