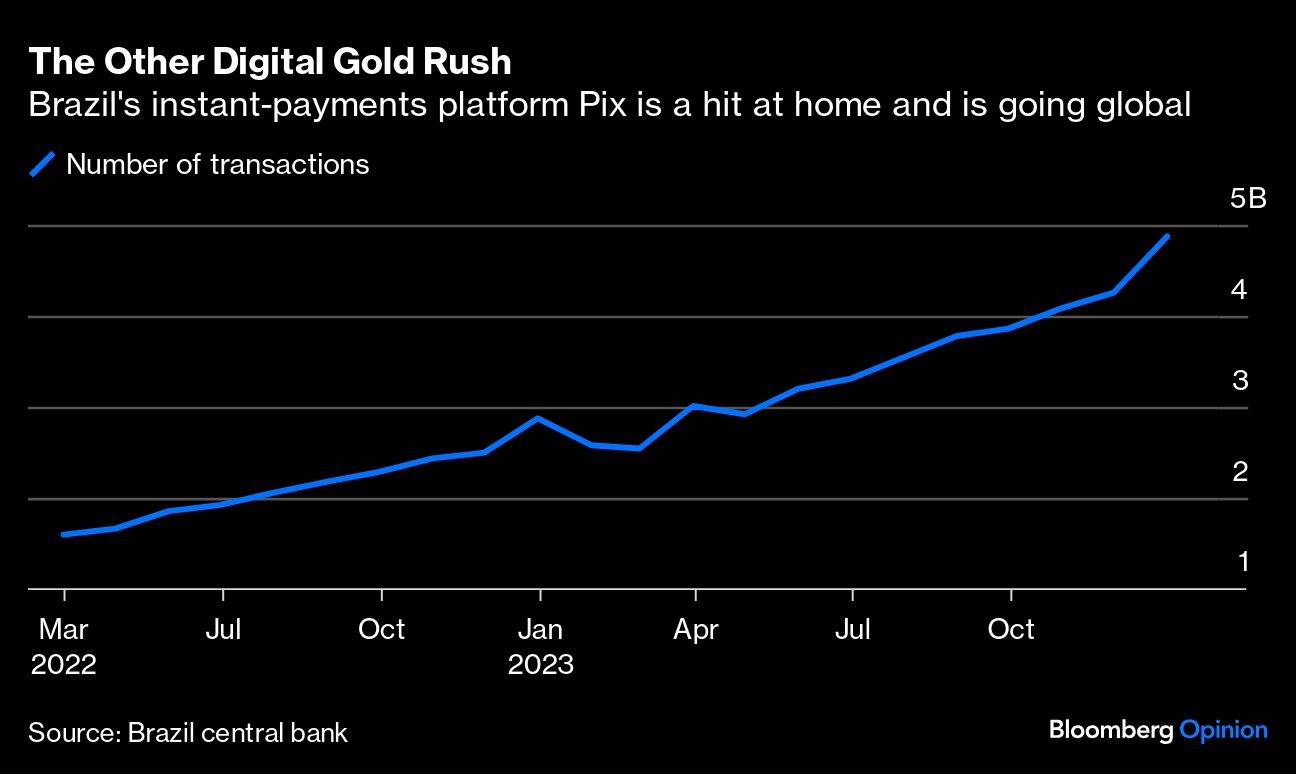

A new form of digital money is going viral, capturing tens of millions of users, billions of transactions and the attention of global central banks. No, not Bitcoin, which is trading at around $68,000 and closing in on a fresh all-time high. Instead, I’m talking about Brazil’s cheap instant-payment system Pix. And the latter just might have a better claim to signposting the future than the cryptocurrency.

Launched in 2020, the initial idea behind Pix — as with all good fintech solutions — was to boost financial inclusion, loosen the grip of a concentrated banking system and make payments quicker and more efficient. It’s succeeded at remarkable speed: It’s been used by 160 million people, or 80% of Brazil’s adult population, as well as 13 million firms, and now beats credit and debit cards as the country’s preferred payment method. The plan is to take it global at a time when central banks are experimenting with payment overhauls and digital currencies to keep a grip on tech disruption.

Think of this as the flip side to Bitcoin’s “fear of missing out,” which is back with a vengeance after the approval of spot exchange-traded funds — essentially a shiny and more accessible wrapper for a token that’s still much more suited to hoarding and speculation than paying bills or generating predictable returns. Whereas the crowd-driven populism of Bitcoin is all about sticking two fingers at family, friends and financiers who caution against buying what Warren Buffett dubbed “rat poison squared,” Pix is shamelessly institutional: It’s a fiat payment system run by the central bank; you need a bank account to use it and participation by commercial banks is mandatory. And there isn’t a blockchain in sight.

Yet Pix is still futuristic in its own way, and doubtless healthier for the economy than the current buying of volatile tokens or memecoins like Dogecoin or Pepe in the hope that a greater fool will eventually come along and buy them back at a higher price. An International Monetary Fund study notes Pix transactions settle near-instantaneously and at a cheaper rate than other alternatives: It’s free for individuals and costs around 0.33% for merchants, which is lower than fees of around 1.13% for debit cards or 2.34% for credit cards — and lower than the 3.99% levy proposed by Meta Platforms Inc.’s WhatsApp payments system.