If you need to sell your home in the next few months, I’d get on with it. As we enter the spring selling season, it’s becoming increasingly clear that the period during which sellers had the leverage in the housing market is over.

The surge in mortgage rates last year led most potential sellers to hold onto their homes and their rock-bottom borrowing costs. Would-be buyers found little available inventory and watched prices climb despite terrible affordability.

But the “5 Ds” that motivate moves — divorce, downsizing, diapers, diamonds, and death — don’t sleep for long, regardless of what’s happening with loan rates. For some homeowners, those life events have occurred and moving can’t be put off any longer.

Listings of homes for sale are now rising at a seemingly accelerating pace. New listings climbed 9.8% in the four weeks ending Feb. 18 on a year-over-year basis, the biggest increase in two months, according to real estate brokerage Redfin Corp. That’s pushing active inventory higher in many markets. It’s rising particularly quickly in south Florida, with Punta Gorda and Cape Coral-Fort Myers both showing a more than 100% gain from a year ago, according to Lance Lambert of ResiClub, which provides research and analysis on the housing market.

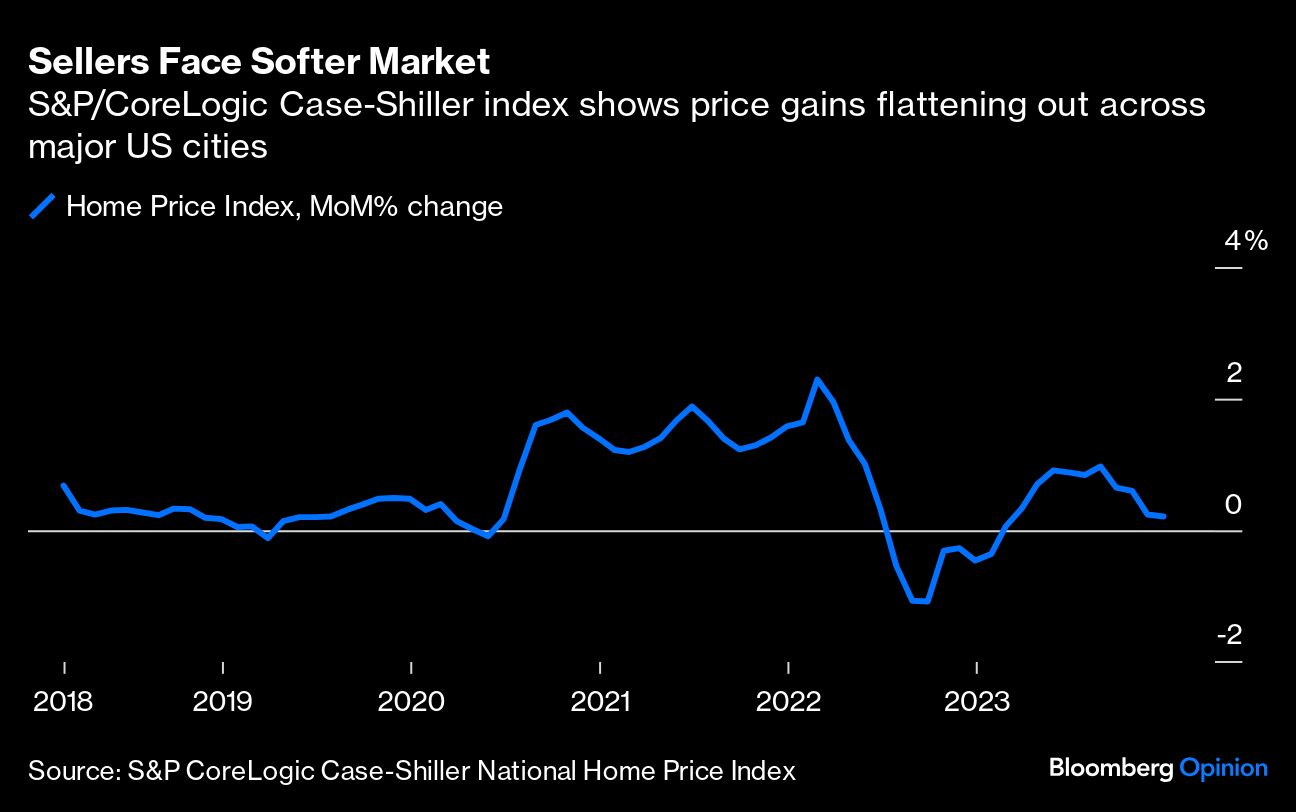

The pressure on prices is easing as more homes hit the market. The S&P CoreLogic Case-Shiller Home Price Index barely budged in November and December after appreciating strongly in the middle of last year. Real-time data show conditions softening further. Mike Simonsen of Altos Research notes that the percentage of homes for sale that cut their asking price last week rose sequentially, something that hasn’t happened in recent years until much later in the spring. If this keeps up, the share of homes with price cuts will be above year-ago levels in a few weeks.

The culprit for the recent softness is the rise in borrowing costs. There was a growing view in December that the Federal Reserve would ease policy significantly in 2024. That pushed 30-year mortgage rates down into the mid-6% zone and likely contributed to optimism among home sellers. But with economic growth stronger than anticipated so far, those rate-cut expectations have been dialed back, and mortgages have moved above 7% again. Home affordability and buyer enthusiasm have been negatively impacted, contributing to the rise in inventory and weakening price trends.

Sellers who had hoped to transact in a market with falling mortgage rates are finding that their bargaining power isn’t as strong as they thought, and they might have to be more flexible on price.

New homes are another factor working against sellers. The stock that builders have for sale is close to the highest in 15 years, and healed supply chains mean they can now start and complete houses faster than a year ago. If existing-home sellers get stubborn on price, they’ll lose deals in many markets to builders who aren’t as willing to sit and wait.

So, what does this mean for you if you haven't listed your home yet but plan to? Geography matters as inventory trends differ a lot by metro. Trends are looking particularly ominous in many Florida markets, but less so throughout the Northeast and Midwest, where homebuilders are also less active.

Lower mortgage rates would help, but even if the Fed started easing in May or June, the current levels price in market expectations of about 150 basis points of policy cuts through the end of 2025. Even if borrowing costs do eventually head a lot lower, it’s looking unlikely for the spring season.

This dynamic means that flattening or modestly declining home prices later this year can’t be ruled out, though we will see price growth on a year-over-year basis through at least the summer due to the gains already locked in. Continued economic strength should limit the downside.

For sellers, the key is to realize that the tide is turning in many markets in favor of buyers, and, if you want to transact, it might take more concessions than you expected even a couple of months ago.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

More Divorce Topics >