Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The Social Security Amendments of 1983 was signed into law by President Ronald Reagan. It placed the system into long-range actuarial balance based on the trustees’ best-estimate assumptions. In that 1983 snapshot, long-range actuarial balance meant that the present value of future system revenues was projected to be equal to the present value of projected system benefit liabilities for the next 75 years. The system’s emerging trust fund plus future system revenues was projected to be sufficient to pay out the benefits anticipated under the amended law for at least the next 75 years.

Fast-forward to 2023. There have been no significant changes in the law as amended in 1983, but the January 1, 2023 snapshot actuarial balance calculation under the trustees’ then-current best-estimate assumptions showed a long-range actuarial deficit of 3.61% of taxable payroll over the next 75 years, or a funded status of about 79.3% if system assets (including the present value of projected system revenues) were simply divided by system liabilities and not expressed as a percentage of the present values of future taxable payrolls.

What caused the system’s measured funded status to deteriorate from 100% to 79.3% over the past 40 years? And more importantly, what actions will Congress take to reform the system to address its current actuarial imbalance and increase the program’s sustainability?

The answers to those questions are critically important to current and future retirees in the United States and are, therefore, important to advisors who are frequently tasked with planning for their clients. Before discussing the causes of the system’s financial deterioration and their implications for future reform, let’s take a quick look at the system’s financial picture.

Current financial projection

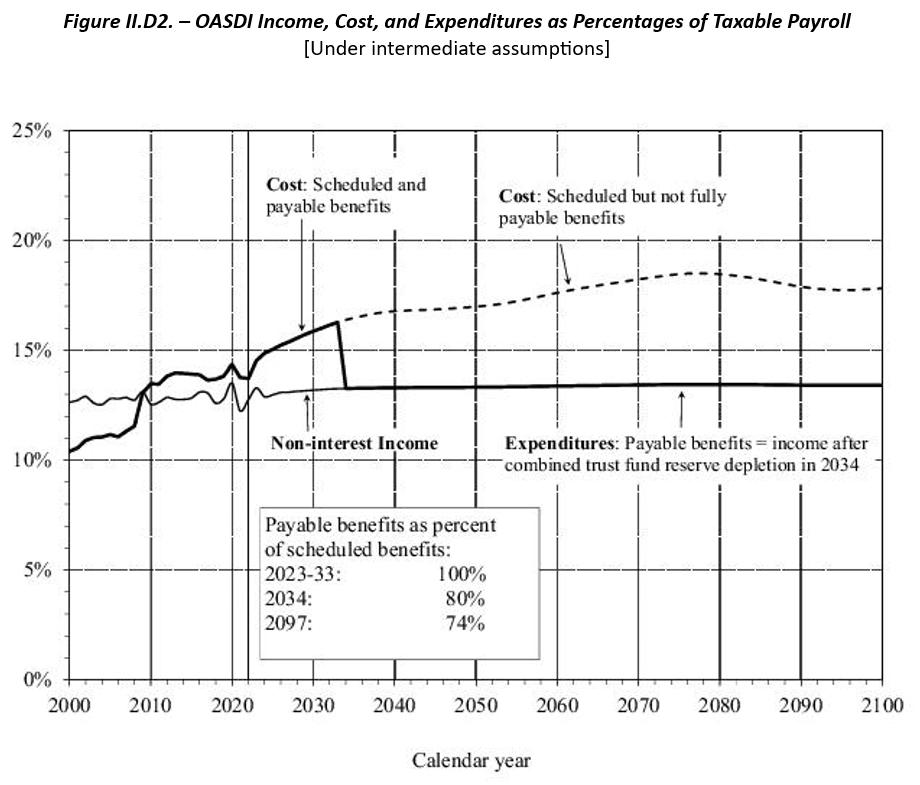

The following exhibit from the 2023 Trustees Report shows projected system income, costs and expenditures as percentages of taxable payroll under the trustees’ intermediate (best estimate) assumptions. System income is expected primarily from FICA taxes with a small percentage (about 1% of taxable payroll at the end of the projection period) from taxation of benefits.

As of January 1, 2023, trust fund assets were about $2.8 trillion, which were expected to fully fund shortfalls of costs over income until about 2034, at which time only 80% of scheduled benefits for that year are projected to be funded (decreasing to 74% at the end of the 75-year projection period).

This exhibit shows that if Congress takes no action prior to 2034, benefits are expected to be reduced across-the-board by 20% after the $2.8 trillion trust fund has been exhausted (with higher across-the-board increases projected after 2034). This is essentially the default reform option against which other options should be measured.

If Congress acts prior to 2034, reform options addressing the short-term (next 20 years) financial picture include increases in revenue and/or decreases in benefits for current or near-term beneficiaries. If Congress desires to grandfather benefits for such beneficiaries, then actions addressing the short-term cash-flow situation will involve primarily increases in revenue. The longer Congress waits to implement such changes, the larger the group of potentially grandfathered beneficiaries.

If Congress decides to increase revenues and decrease benefits so that actuarial balance is achieved at a level projected future cost and income rate for both for the short and long term (say, for example, with a level projected cost and income rate of 15-16% of taxable payroll), reform will likely involve both revenue increases and benefit reductions for both current and future beneficiaries.

Primary causes of Social Security’s funded status deterioration since 1983

There are two primary causes of the decline in Social Security’s measured funded status since 1983:

- The assumptions adopted in 1983 were too optimistic (and continue to be too optimistic); and

- Congress failed to address the system’s funded status decline since 1983.

I will discuss each of those causes.

1. The assumptions adopted in 1983 were too optimistic

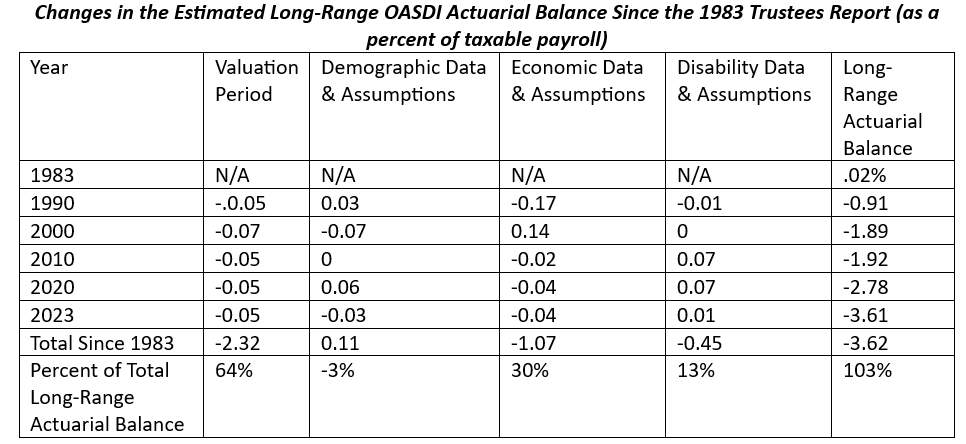

The Office of the Chief Actuary at the SSA annually summarizes the changes in the system’s long-range funded status in Table 1 of Actuarial Note Number Year.8 (The most recent is 2023.8). This actuarial note is entitled DISAGGREGATION OF CHANGES IN THE LONG-RANGE ACTUARIAL BALANCE FOR THE OLD AGE, SURVIVORS, AND DISABILITY INSURANCE (OASDI) PROGRAM SINCE 1983. This document breaks down the sources of the system’s funded status deterioration since 1983. It is essentially a gain/loss analysis by source for the system (and includes the effects of assumption changes). I’ve excerpted results for several years and totals from Table 1 of Actuarial Note 2023.8 below.

The key takeaways from this exhibit include:

- The system’s funded status (long-range actuarial balance) has declined continuously over the past 40 years due to outcomes that were less favorable than assumed (and changes in those assumptions).

- Of this decline, 64% is attributable to actuarial losses (differences between actual experience and assumed experience) generated from annual changes in the valuation period (discussed in more detail below), while about 30% of the decline is attributable to actuarial losses attributable to overly optimistic economic data and assumptions.

- Demographic data and assumptions, which are frequently cited as a major factor in the system’s funded status decline since 1983, have had a small positive effect (gain) as have legislative changes and methods and programmatic data changes (not shown above).

- Even if all assumptions are realized in the future, the system’s funded status is expected to keep deteriorating under current law because of the actuarial losses associated with the annual change in the valuation period (or “valuation date creep”).

- Because the system’s funded status is measured over a 75-year period, the shortfalls expected after the end of that period under current law have been ignored each year until subsequent years’ valuations. This valuation approach implicitly assumes that annual system income will be equal to annual system expenses for years after 75. In the 2023 Trustees Report, the annual shortfall of the cost rate over the income rate projected for years after 75 was almost 5% of taxable payroll under the Trustees best-estimate assumptions, as is shown in the figure above. Clearly, this implicit assumption that system costs will equal system revenue for years after 75 has been and continues to be an unreasonable assumption under current law.

2. Congress failed to address the system’s funded status decline

Despite calls from the Trustees for congressional action to address the system’s declining funded status, for almost 30 years Congress has taken no action. And it is not as if this problem was hidden in the OASDI Trustees’ reports. For example, in the 1996 OASDI Trustees Report (1996!), the Trustees said:

Although the combined trust funds are well financed over the next 10 years, the OASDI program is not in close actuarial balance over the full 75-year projection period and therefore does not meet the long-term solvency test. The estimated actuarial balance is a deficit of 2.19% of taxable payroll over the next 75 years, based on the intermediate assumptions. The combined OASI and DI Trust Funds would become exhausted in 2029 without corrective legislation. At that time, annual tax revenues of the combined trust funds would be less than expenditures by 3.87% of taxable earnings and would be sufficient to cover only 77% of annual expenditures.

and

In view of the lack of close actuarial balance in the OASDI program over the next 75 years, we again urge that the long-range deficits of both the OASI and DI Trust Funds be addressed in a timely way….It is important to address both the OASI and DI problems soon to allow time for phasing in any necessary changes and for workers to adjust their retirement plans to take account of those changes. We believe there is ample time to discuss and evaluate alternative solutions with deliberation and care. The size of the long-range deficit is such that long-range balance could be restored within the framework of the present program. Nonetheless, the magnitude of any required changes will be smaller the sooner they are enacted.

Similar statements were also made in the 1994, 1995 and most subsequent reports.

Had more timely Congressional action been taken, some combination of benefit cuts and/or revenue enhancements would have been adopted to restore the system’s long-range actuarial balance. Since no benefit reductions have been enacted, system income has been insufficient to fund system benefits for at least the past 30 years.

Implications for future system reform

There are four implications and associated policy actions to consider:

1. Address expected shortfalls after 75-year projection period.

A significant portion of the 75-year “valuation date creep” problem can be attributable to assumed future longevity increases and other demographic assumptions. Therefore, much of the valuation date creep can be addressed by increasing the system’s normal retirement age and indexing it in the future with assumed longevity increases. This solution was recommended to address this issue by the 1994-1996 Advisory Council. Its report said, “The long-term actuarial balance of Social Security should not be adversely affected solely by the passage of time.” (see Social Security History (ssa.gov))

2. Increase system income revenue.

In addition to increasing FICA tax rates for all workers going forward, it may be necessary to increase income subject to FICA tax and increase income from taxation of benefits. Some of these increases, targeted at higher paid workers and beneficiaries, may be justified because of less-favorable-than-assumed economic experience since 1983.

3. Reduce benefits for some current and near beneficiaries.

As discussed above, Congress failed to increase revenues during the past 40 years. Therefore, a good argument can be made for decreasing benefits for current beneficiaries (especially those more financially well-off) since they avoided paying higher taxes during most of their working careers. Such decreases (such as temporarily freezing cost-of-living increases or increases in taxes on benefits) will also be perceived as being fairer to younger generations of taxpayers whose taxes under most reform options are likely to be increased and their benefits reduced.

4. Implement automatic adjustment to maintain actuarial balance.

To maintain system sustainability and avoid periodic significant disruptions (like the disruption we will see with the upcoming system reform), it makes sense to implement automatic adjustment mechanisms in tax rates or benefits to maintain the system’s actuarial balance on a going-forward basis. Future Congresses can, of course, make non-automatic changes to the program if necessary.

Conclusion

Social Security’s funded status has deteriorated rapidly since 1983, primarily because of the valuation-date creep. Unfortunately, Congress has failed to address this emerging deterioration, and we are now facing a sticky problem to place the system back into actuarial balance. It is my hope that the next round of system reform addresses the lessons learned from the past so that current problems are not repeated in the future.

Social Security sustainability can be significantly improved by designing program benefits that are expected to represent a level or nearly level cost in the future if all assumptions are realized, with automatic adjustments in costs/benefits occurring if assumptions are not realized. The Canadian Pension Plan has successfully used such an approach since 1997.

Because Social Security is typically a major component of a client’s retirement plan and because financial advisors are frequently tasked with helping their clients develop such plans, advisors need to be aware of Social Security’s current and future financial condition and likely-to-be-enacted reforms.

Ken Steiner is a retired actuary with a website entitled "How Much Can I Afford to Spend in Retirement?"

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

More Fixed Income Topics >

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.