An RIA-Friendly Life Insurance Strategy for Retirement Security (Part Two)

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

In the first installment of this series, I pledged to unveil a retirement strategy with such merit that it warrants widespread adoption by the investment advisor community. Let's delve into the compelling case for this approach.

Figure 1 All sides agree: We have a crisis.

Context: An unaddressed crisis

The retirement-security crisis in the United States has garnered bipartisan attention, with key figures like Bernie Sanders, Ben Carson, Elizabeth Warren, Marco Rubio, Rand Paul, and Patty Murray highlighting its urgency. Even artificial intelligence, represented by ChatGPT, emphasizes the inadequacy of retirement savings, particularly due to the decline of defined-benefit plans: “The decline of defined benefit plans has left a void in our social safety net that 401(k)s and other defined contribution plans simply cannot fill."

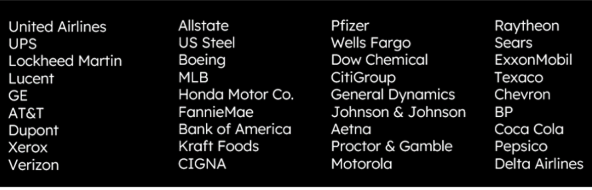

Figure 2 A sampling of companies that have frozen or terminated their defined benefit plans.

ChatGPT's astute analysis identifies the root cause – the disappearance of defined-benefit pensions, which were a cornerstone of the postwar middle-class dream. This shift has left many Americans ill-prepared for retirement, especially with the rise of defined-contribution plans like 401(k)s, which lack the crucial element of providing a lifetime monthly paycheck.

A surprising answer: A bright new option

In part one, I explored the challenges facing life insurance policies and alluded to the subject of this installment, defined-benefit life, as a groundbreaking solution. This innovative strategy aims to eliminate common concerns associated with life insurance while creating a new avenue for strengthening retirement security, uniquely addressing the shortcomings of existing choices.

While it is not a pension, defined-benefit life is designed to replicate the economic structure of a defined-benefit pension, offering a personal, private context that defines an individual's retirement income. With a robust system for policy management, it provides annual reports detailing premium adjustments, builds tax-advantaged wealth, and, at retirement, can offer decades of tax-free income.

First priority: Lower costs to maximize tax-advantaged wealth building

In part, the key to defined-benefit life's success lies in minimizing the cost of providing life insurance. By adhering to IRS guidelines and maintaining the minimum life insurance necessary, this strategy ensures a low-cost structure while preserving the tax advantages of life insurance.

In developing defined-benefit life, I will ask and answer three questions:

1. How can we eliminate the excessive fees that are often associated with life insurance?

2. How can we guard against policies becoming impaired due to interest crediting that is lower than originally projected?

3. Can we reduce the essence of a defined-benefit pension plan down to the individual level while retaining tax advantages that seasoned investors would recognize as having no equal?

Answering these questions leads to a new type of retirement security vehicle, one that can be characterized as having:

- The economic structure of a defined benefit pension;

- Reiterated in a personal, private context;

- Focuses on a predefined retirement income;

- Incorporates a system for policy management that annually advises on premium adjustments required to keep the policy on track for the desired retirement income;

- That builds wealth year-over-year without current taxes; and

- Provides decades of income that is income tax free.

What emerged from answering these questions is a vehicle that looks like nothing else, and that has advantages nothing else can match. I recognize that this is a strong assertion, but here is why it’s accurate.

Incredible tax advantages

- Tax-free death benefit. All life insurance policies provide at least a minimum life insurance benefit which the insured’s named beneficiaries are entitled to receive income tax-free.

- Tax-deferred growth. The systematic investments made into a life insurance policy, referred to as the premiums (insurance has its own vocabulary), accumulate inside the policy’s cash value and are added to by monthly interest credited either at a fixed rate declared by the insurance company, or calculated as a percentage of the performance of one or more stock indices.

- Tax-free income. For obvious reasons, this is the tax benefit that sophisticated investors find most appealing. Income is tax free because withdrawals are taken in the form of loans that are made against the cash value. The interest rate on these loans is exceedingly favorable, typically spinning out money annually at a zero-net-cost. The total amount of money taken in the form of loans can be multiples of the policy’s cost basis, yet it remains income tax free. At the insured’s death, the remaining insurance value is paid to the named beneficiary income tax free.

Imagine a 35-year-old I will call Steve. Steve allocates $10,000 annually to defined-benefit life through age 64. That investment of $300,000 might grow to, say, $1,200,000. At age 65, Steve begins to take annual withdrawals via policy loans in the amount of $75,000 a year. Let’s assume that Steve lives all the way to age 100. Over those 35 years, he would have received $2,625,000 income tax free.

Roth-like tax treatment with better benefits

You probably recognize the tax treatment of defined-benefit life as being similar to a Roth IRA. But with defined-benefit life, one gains the additional benefits of:

- No cap on contributions;

- No reporting requirements; and

- Insurance protection that Roth vehicles do not provide.

The enrollment process

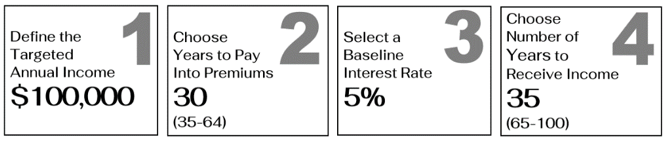

Defined-benefit life initiates with a life insurance application. But in addition, the policy owner makes four key decisions that shape the policy's management and utilization in retirement. These decisions, once set, provide a structured framework for achieving financial security. The policy owner must define:

1. The amount of desired annual retirement income.

2. The number of years investments (premiums) will be made into the policy.

3. A baseline interest rate assumption that the policy owner expects the policy to earn over the course of its lifetime, and,

4. The number of years the policy owner wishes to receive income commencing at retirement.

Figure 3 The Four Decisions Made at Time of Application

Mark, a software company executive, is like many of his generation. He has little faith in Social Security, and he recognizes the imperative to take personal responsibility for his retirement security. Mark is attracted to the tax advantages of defined-benefit life, its flexibility and the life insurance benefit that will provide additional financial security to his wife and young twin boys should he die prematurely.

Mark decides to target an annual retirement income of $100,000 beginning at age 65. He decides that he will pay into the policy through age 64. For an interest rate assumption, he selects 5%.

Finally, Mark defines a period of 35 years to receive income, from age 65 through 100.

Figure 4 Mark's defined-benefit life strategy assumptions.

Based upon a 5% rate-of-return projection and a minimum amount of life insurance, Mark’s insurance agent, Jason, explains that a monthly investment of $1,500 is required to fund the strategy. As the funding vehicle, Jason suggests an indexed universal life policy. For interest crediting, Mark chooses a 50%-50% allocation to growth strategies based upon the performance of the S&P 500 and NASDAQ 100. Mark’s policy is underwritten and approved, and his four key decisions are memorialized.

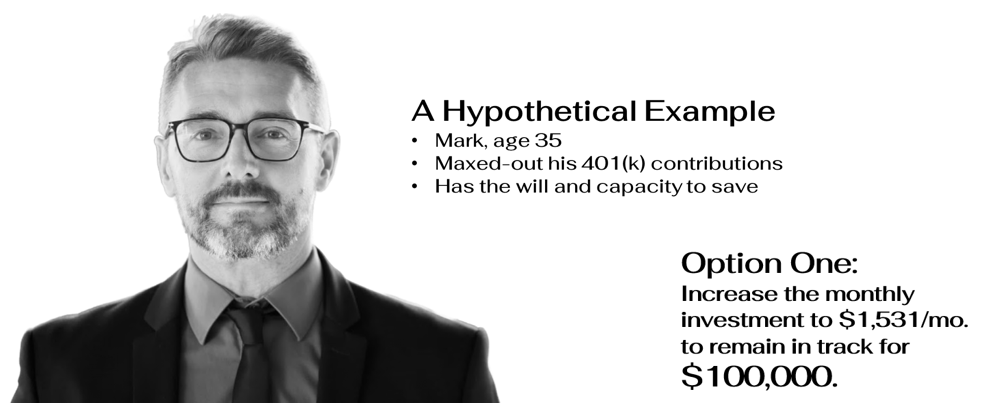

Year one: Interest is lower than the baseline

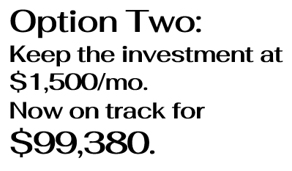

Assume that in its first year the policy earned 4%. That is obviously less than the baseline interest rate assumption. Mark’s defined-benefit life annual report will provide two options. Option one is to raise his monthly investment to $1,531 to remain on track for his desired $100,0000 income

Option two informs Mark of how his plan changes if he does not increase his monthly investment. With no change in the monthly premium, Mark will be on track for a slightly smaller income, $99,380. Mark decides to increase his monthly investment to $1,531.

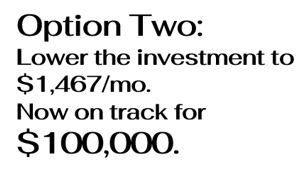

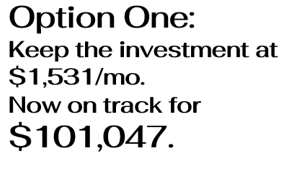

In year three, Mark’s policy earns an interest rate of 7.5%, more than the 5% baseline. Again, the defined-benefit life policy management system recalculates two premium adjustment options for Mark’s consideration: Option one is to keep the premium unchanged at $1,531 per month and now be on track for a higher annual income – $101,047. Or Mark can reduce his investment to $1,467 per month to be on track for the original targeted annual income of 100,000.

This monitoring and recalculation process occurs annually. With it Mark is always empowered with the information he needs to make a good decision. If he chooses to make the adjustments suggested, he essentially makes it a certainty that he will receive his targeted income. Was that not the key benefit of a defined-benefit pension?

Interest crediting post-retirement is equally important as pre-retirement. This is one reason I argue that a conservative baseline interest rate should be selected and maintained throughout the life of the plan.

The economic methodology employed in this system of policy monitoring and management is simpler (there are no actuarial considerations, for instance), but fundamentally identical to the economic model of a defined-benefit pension. In line with my design objective, it has been brought down to the level of an individual investor.

Funded by life insurance and consumer-oriented

Defined-benefit life is a solution for a lifetime financial security that, in one or more key areas, other vehicles fall to offer. The totality of its advantages is so compelling that investment advisors should integrate it into their practices. They even can use defined-benefit life as a strategic tool for acquiring new clients.

How?

Defined-benefit life may help you recruit the children of your older clients. Affluent investors who are still decades away from retirement will be attracted to a strategy for wealth building and future retirement income that is tax-free. In this context, what alternative would you recommend to them that would be superior to defined-benefit life? Your clients who are grandparents may wish to give a financial boost to grandchildren. A grandparent can allocate an amount of savings to cover policy funding for a predetermined number of years.

Solving seemingly intractable problems

Think back to the problems with life insurance that I outlined in part one of this article. Each of them is solved by defined-benefit life. This is a noteworthy outcome. I described how life insurance policies get in trouble when interest crediting is less than projected.

Defined-benefit life reverses the common tendency of agents to highlight aggressive cash value projections. Defined-benefit life should be viewed as way to deliver stable and predictable income, an efficient approach for increasing a client’s foundational or “floor” type income. In this context, a conservative baseline interest rate assumption – in the range of 3% to 5% – is advisable. A conservative stance makes it more likely that only small adjustments (or no adjustments) to the premium investment will ever be needed.

Because it is not an investment, defined-benefit life should not be compared to investing. It should be thought of as an alternative to safe money savings vehicles or fixed income options. None of those alternative safe money vehicles will match the tax and other advantages that defined-benefit life offers.

If the policy owner makes the required premium adjustments, the defined-benefit life strategy should never result in lapsed policy. When intervention to adjust premiums occurs early and frequently, i.e., annually, it takes only small adjustments to keep the policy on track. This is the reality that has been missed across multiple generations of universal-life insurance policies. It is when policies are neglected for five years or 10 years or more that the accumulated investment deficit becomes so large that it is unrealistic for most clients to come up with the lump sum required to stabilize the policy. This sad outcome should no longer happen.

Marketing defined-benefit life

Figure 5. Jennifer and Alex are Digital Humans, part of the innovative lineup of educational tools that support client’ understanding of Defined Benefit Life.

No effort is made to disguise the fact that defined-benefit life is life insurance. On the contrary, it is disclosed as soon as the client sees the logo with the tag line, An innovative life insurance solution. In the unlikely event they even wanted to, financial professionals who will offer defined-benefit life will not be able to disguise the fact that it is life insurance. That is because the innovative digital tools that have been developed for education and marketing plainly and proudly proclaim this fact: only life insurance can offer all the benefits that defined-benefit life provides.

When you see TikTok or other advertisements that aggrandize or hype indexed-universal life, remember that it is not the life insurance policy that is the problem. Rather, it is the misuse of the policy and misleading marketing that account for justifiable criticisms.

I began my career in life insurance. Along the way, and at a time when the interest rate climate was much different, I invented the first life insurance strategy utilizing tax-free policy loans for generating supplemental retirement income. Due to the structural decline in interest rates that unfolded over subsequent years, generations of universal-life policies failed to materialize as they were projected to. That is why defined-benefit life is so important to me. It is the culmination of work I began decades ago, and a solution to a problem that has long plagued the life insurance industry.

Are you intrigued by defined-benefit life? If you have questions about it, I would love to speak with you. Please reach out by email or telephone. My mobile number is 978-375-3400, and my email address is [email protected]. I am eager to promote the advantages of defined-benefit life to as many advisors as possible.

Defined-benefit life stands out as a compelling solution to the retirement-security crisis, offering a unique combination of tax advantages, flexible management, and lifetime income benefits. Its innovative approach addresses the shortcomings of traditional retirement plans and provides a promising path towards a secure financial future.

Wealth2k® founder, David Macchia, is an entrepreneur, author, and public speaker whose work involves improving the processes used in retirement-income planning. He is currently creating solutions to mitigate the threat to human financial advisors that is posed by emerging AI competitors. His website is www.wealth2k.com.Top of Form

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits