The world’s biggest miner BHP Group Ltd. grew powerful by building dominant positions in producing the minerals of the future. That makes the challenges it’s facing with two key clean-tech ingredients a sobering lesson for the energy transition.

Nickel and copper have long been recognized as vital components of a decarbonized economy. The former helps to cram energy into the lithium-ion batteries used in electric vehicles and grid-scale power storage cells. The latter is used almost everywhere electricity flows — from wires, motors and turbines to heat exchangers and transformers.

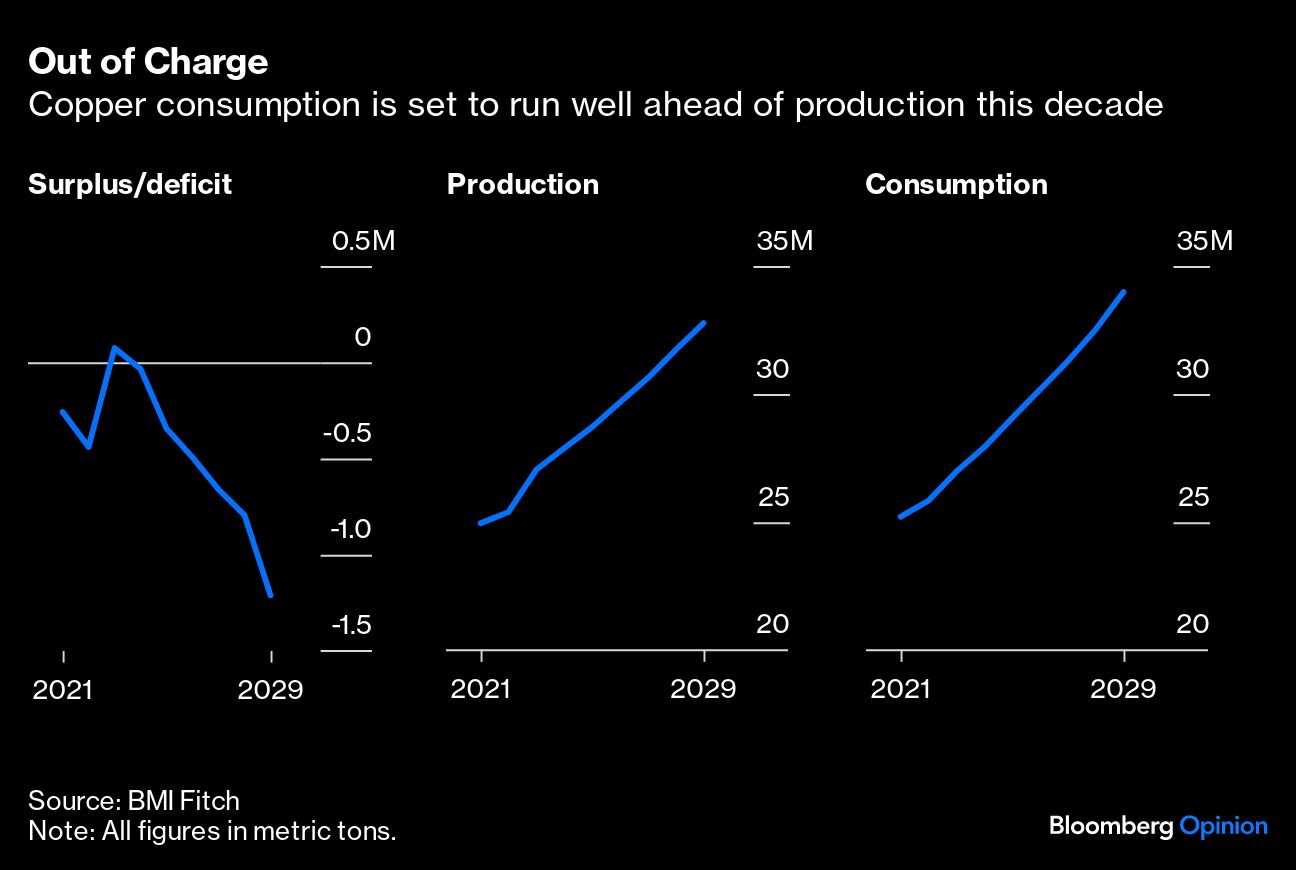

Annual nickel supplies need to grow from about 3.4 million tons currently to more than 5 million tons in 2030 to keep the world on a path to net zero, according to the International Energy Agency. Copper must go from 25 million tons to 35 million tons. Ideally, we should be seeing supply of both metals expanding at a rapid clip, with the emphasis most strongly on copper, where miners produce about 10 metric tons for every ton of nickel.

The scenario that’s playing out is close to the opposite. Chinese companies refining battery-grade nickel from the red soil of eastern Indonesia are flooding the market, sending prices down about 40% over the past 12 months and pushing about half of global production into losses. While copper prices have fallen about 7.7% over the same period, almost every mine is churning out profits. That’s still not sufficient to induce more production to come onstream, however. Fitch Ratings Inc. estimates that supply will be falling 1.2 million tons short of demand by 2029.

The most prominent bad news in BHP’s first-half results Tuesday is likely the $2.5 billion impairment to an Australian nickel business that’s been struggling for many years before briefly forecasting better prospects from the EV battery revolution. “We did not anticipate, nor did the rest of the market, the rapid growth of Indonesian supply,” Chief Financial Officer David Lamont told investors Tuesday. The unit might end up being mothballed until signs the market is recovering.

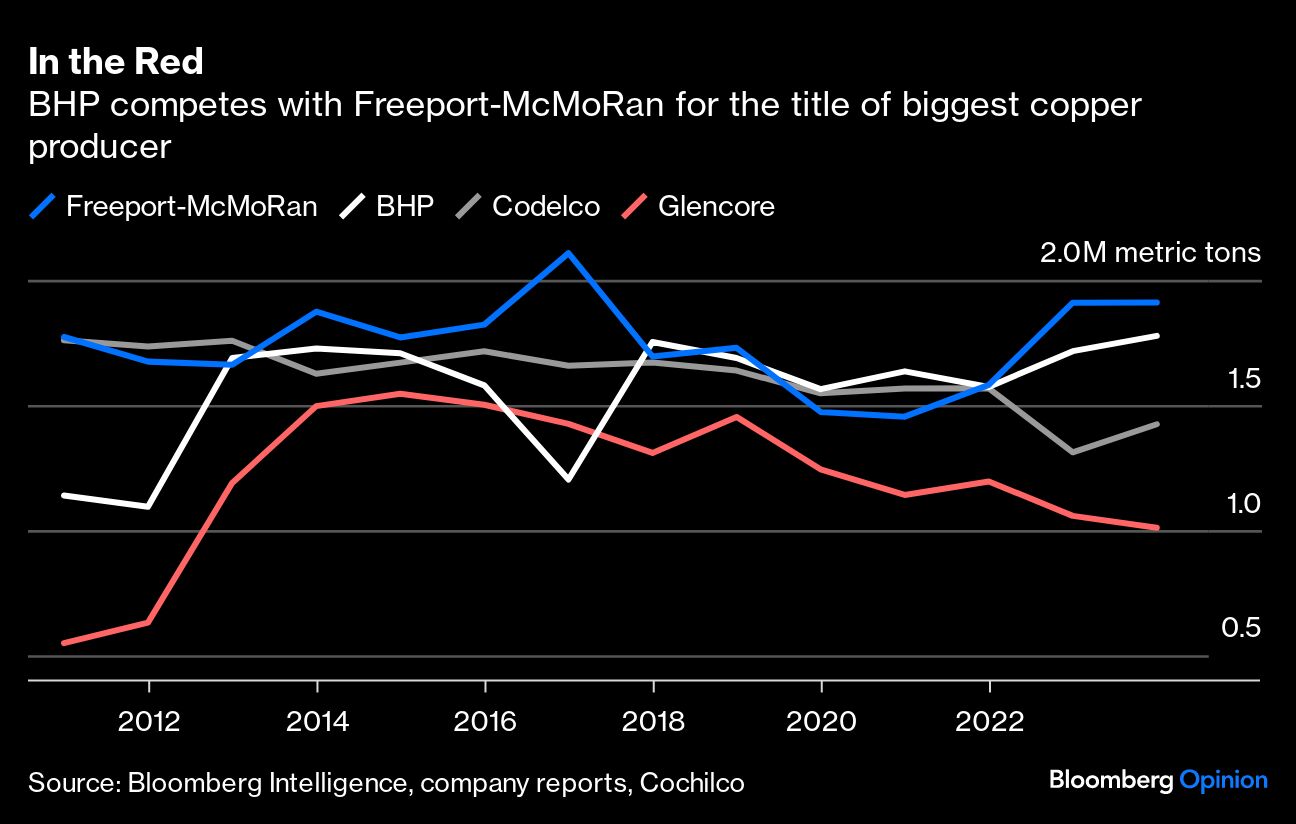

And yet the more favorable news on copper is not all that much better. BHP owns the world’s biggest copper pit, Escondida, and occasionally challenges Freeport-McMoRan Inc. for the title of largest producer — but its plans to address the looming supply deficit as the world shifts to clean energy don’t match the scale of the problem.

Some promising drilling results near its underperforming Olympic Dam mine in the state of South Australia and progress on ore-processing at Escondida look like they’ll consume about $1 billion a year this year and next. That’s far less than the $10.6 billion that’s being spent in the long term on getting BHP’s Canadian potash project into production. Indeed, if you add the $2.5 billion nickel impairment to the $1.4 billion of capital spending in that division this year, the battery metal is gobbling up nearly as much shareholder value as the $4.2 billion capex that’s being dedicated to copper.

The closest thing to an upgraded target comes from South Australia, where we might be seeing over 500,000 tons of copper a year by the end of this decade, compared to a forecast range of 310,000 tons to 340,000 tons this year. The shortfall in the global copper market by then, however, will be an order of magnitude larger.

It’s not going to be enough. Some $250 billion needs to be spent on growth by 2030 to meet demand from the transition to net zero, BHP’s Chief Executive Officer Mike Henry told an industry conference in Barcelona last May. In a global market where it produces about one ton out of every 14, BHP would need to be spending north of $2.5 billion a year to shoulder its share of that burden — but guidance this year comes to $0.9 billion.

The trouble is, BHP doesn’t have many attractive candidates to fix copper’s supply problem. At Cerro Colorado north of Escondida, there may be as much as 6.1 million tons of copper awaiting exploitation — but operations were suspended in December because the mine in its current form is too small, and might need billions spent on water desalination if it’s to operate again. The Resolution venture with Rio Tinto Group in Arizona looks even more promising on paper, but approval has got tangled amid opposition from local First Nations groups.

That’s worrying. Slumping prices for nickel and lithium mean that electric vehicles have far better prospects than the current gloom in the market would suggest, as materials costs fall and encourage wider adoption. Copper has the opposite problem. Current prices are great for miners — but they make every product that will drive the decarbonization of our economy a little more expensive. That can only slow the shift to zero.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by David Fickling