Bond Traders Need to Price In Risk of Future Fed Hikes, Citigroup Says

Bond traders have come more in line with the Federal Reserve’s trajectory for the upcoming easing cycle. Strategists at Citigroup Inc. say what’s missing now is traders hedging the risk of a very brief easing cycle followed by rate increases shortly thereafter.

Citigroup, whose economists expect the Fed’s first rate cut in June, sees some potential for the next few years to mirror what happened in the late 1990s. In 1998, the US central bank cut rates three times in rapid-fire succession to short-circuit a financial crisis brought on by the Russian debt default and the near-collapse of hedge fund Long Term Capital Management. The Fed then began a cycle of rate increases in June 1999 to contain inflationary pressures.

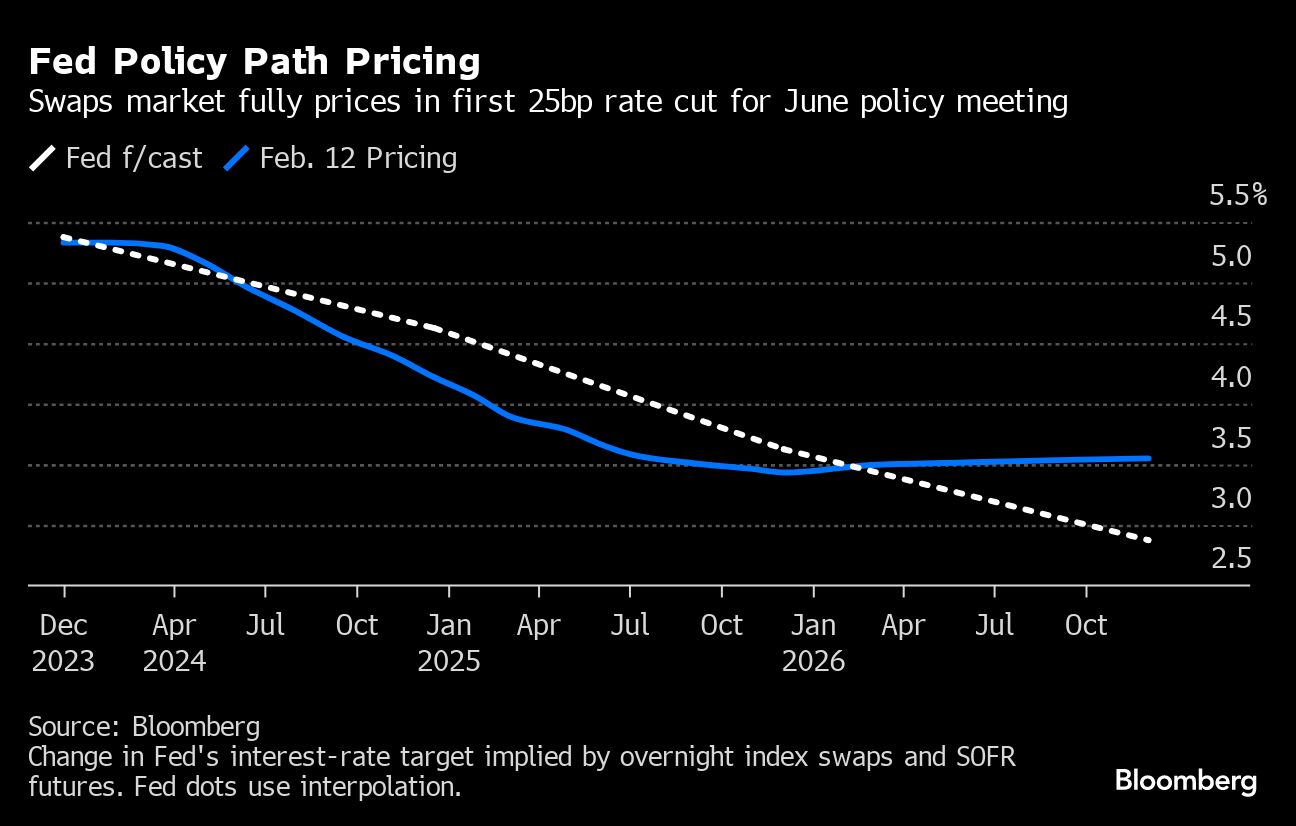

Swaps traders now predict the Fed carrying out just four or possibly five quarter-point rate cuts in 2024, slightly more than the three penciled in by policymakers in their most recent quarterly rate forecast, known as the dot plot. Last year, traders expected as many as seven such moves this year.

“The market should price in some risk of future hikes – look to 1998,” Jason Williams, global market strategist at Citigroup, wrote in a note. This cycle “could be more akin to the 1998 easing cycle, which was short-lived and led to more rate hikes. If inflation does not return to a consistent 2% the upside tails around future Fed hikes should increase from this very depressed level.”

If inflation proves to be sticky, the debate about the Fed’s so-called neutral rate — which balances supply and demand — could resurface and spark the Treasury yield curve to steepen, Williams said.