Special purpose acquisition companies have for too long existed in a regulatory gray area. With new rules approved last month, the Securities and Exchange Commission has provided needed clarity for these entities and their investors.

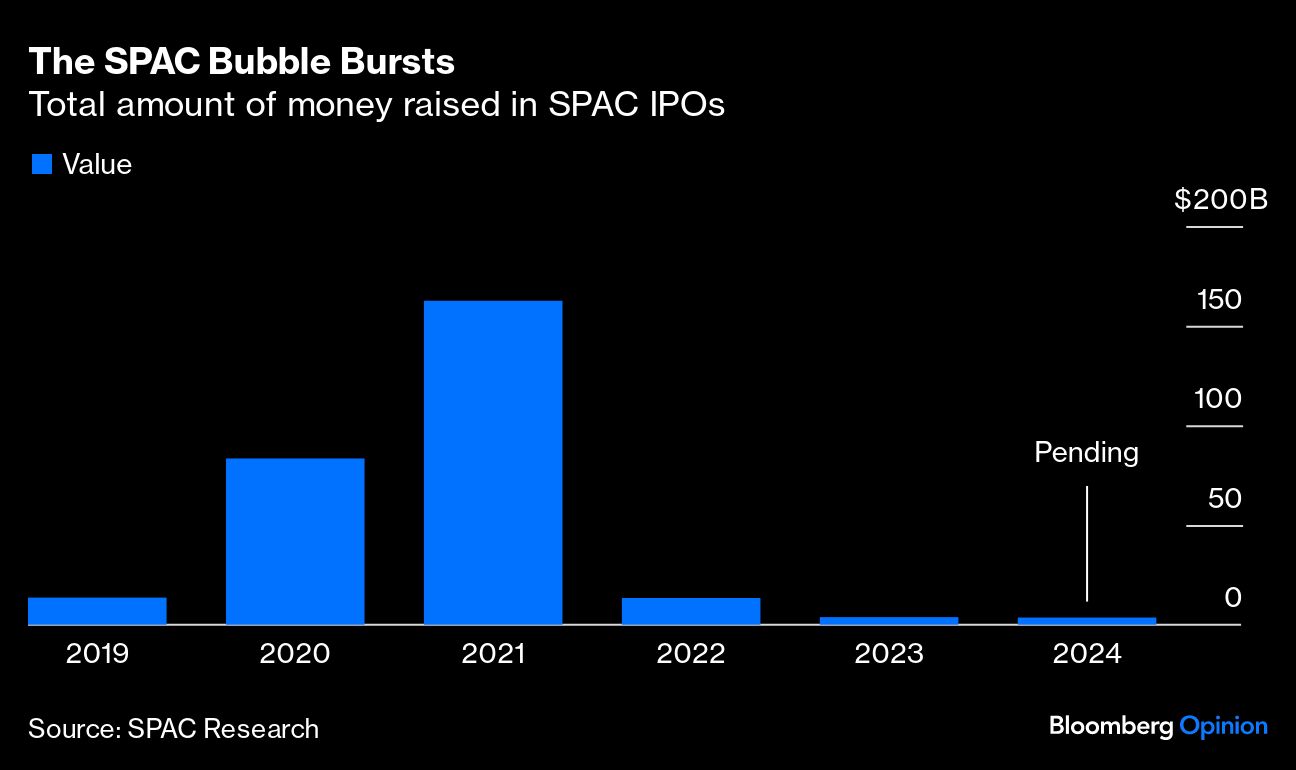

SPACs, sometimes called blank-check companies, tend to thrive in periods of market euphoria — think 2007 and 2021. Sponsors, often hedge funds or private equity companies, raise money on the public markets with a promise to use the funds to take over an as-yet-unidentified private company, typically within two years.

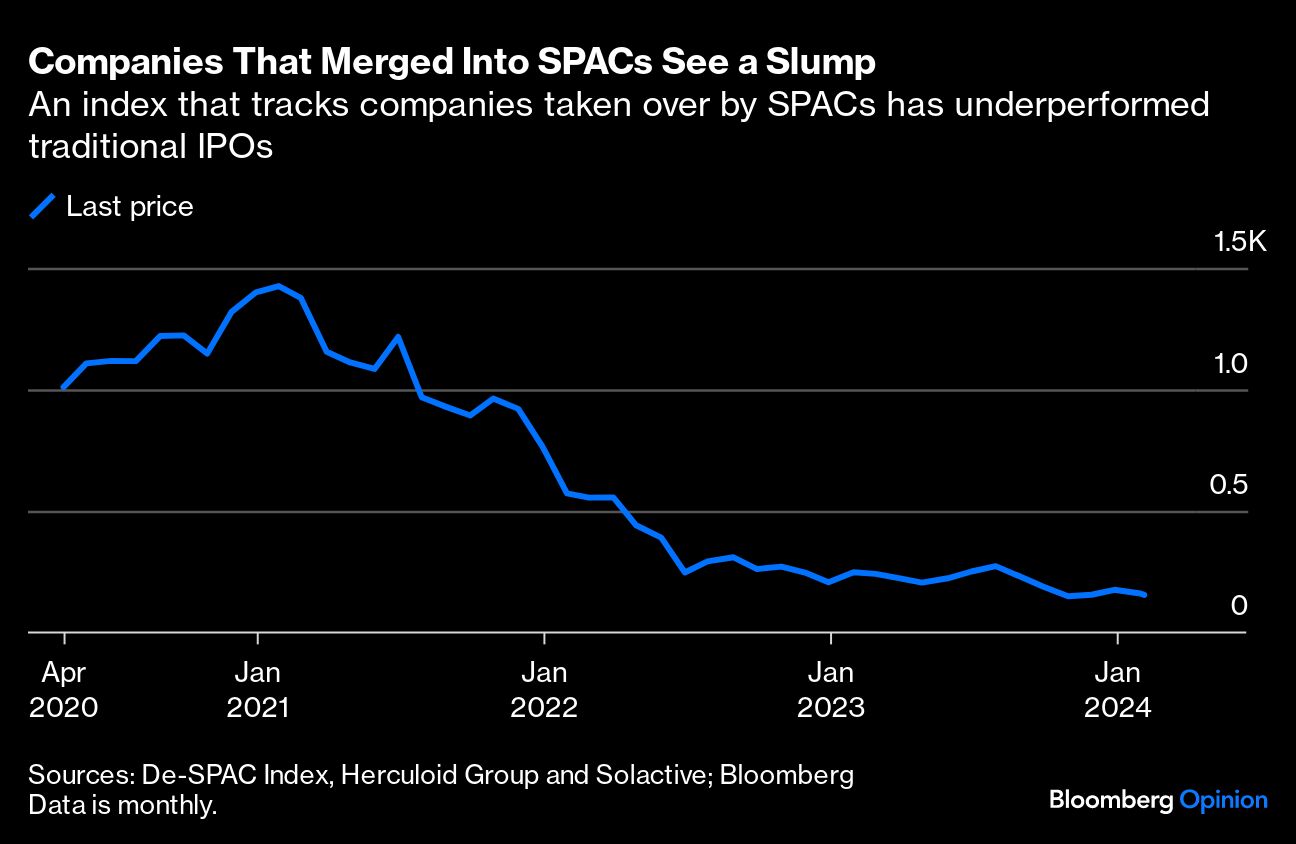

Because the eventual deal is designed as a merger instead of an initial public offering, it’s not clear if target companies are required to abide by standard disclosure rules. Public offerings are one of the few exemptions from a 1995 law that gives companies “a safe harbor from liability for forward-looking statements.” That means most of a company’s statements about the future — say, about a merger — are protected from liability if they turn out not to be true. Not so with IPOs. SPACs have thus become a way to bring unprofitable, early-stage companies to the public market based on business projections that likely wouldn’t pass muster in traditional offerings. Partly as a result, some have quickly gone bankrupt.

The new rules eliminate such regulatory arbitrage and will ensure that SPAC investors have the same safeguards as those in IPOs. Sponsors will also have to disclose more information about their compensation, conflicts of interest and shareholder dilution. Those costs add up: One study found that, for the median SPAC analyzed by the authors, sponsor compensation and other fees siphoned off about $3.33 for every $10 share held by investors.

Critics of the SEC’s approach make two main arguments. On one hand, they say that the rules — even before they were approved — had the effect of killing SPACs and depriving retail investors of the ability to get a piece of exciting early-stage companies. On the other, they say the new rules are unnecessary because most SPAC sponsors are already disclosing information about their compensation and conflicts and aren’t providing irrational projections to investors.