Two major events are shaking up the asset-management world. Blackstone Inc. raised $1.3 billion for its first retail private equity fund, targeting those who have at least $5 million to invest. Separately, BlackRock Inc. is buying Global Infrastructure Partners for $12.5 billion, a major foray into alternative investments. The acquisition will make it the second-largest manager of private infrastructure assets.

After blowing past major milestones — the pair now manages over $1 trillion and $10 trillion, respectively — Blackstone and BlackRock need to show investors they still have a good story to tell. The two deals showcase just that.

Not every dollar earned is deemed equal. In private equity, for instance, being able to fund raise and earn management fees has become more valuable than notching superior fund performance.

As private equity groups enter 2024 with record a $2.8 trillion in unsold investments, analysts are brushing away potential gains from asset sales. After all, initial public offering markets remain anemic; so do global M&A activities.

HSBC Holdings Plc, for one, calls realized capital gains on portfolio exits “low quality,” while praising the “sticky and hence high quality” nature of fee-related earnings. In its sum-of-the-parts analysis, earnings from asset sales get a 25% valuation discount, while those from management fees receive a 50% premium.

Institutional investors are fed up by private equity firms that continue to ask for more money, with few exits in sight. Some sovereign wealth funds and state pension providers have told the managers that they want their money back before committing to upcoming raises. Recently, a few are creating so-called evergreen funds. They are more difficult to manage, but allow investors to redeem more easily.

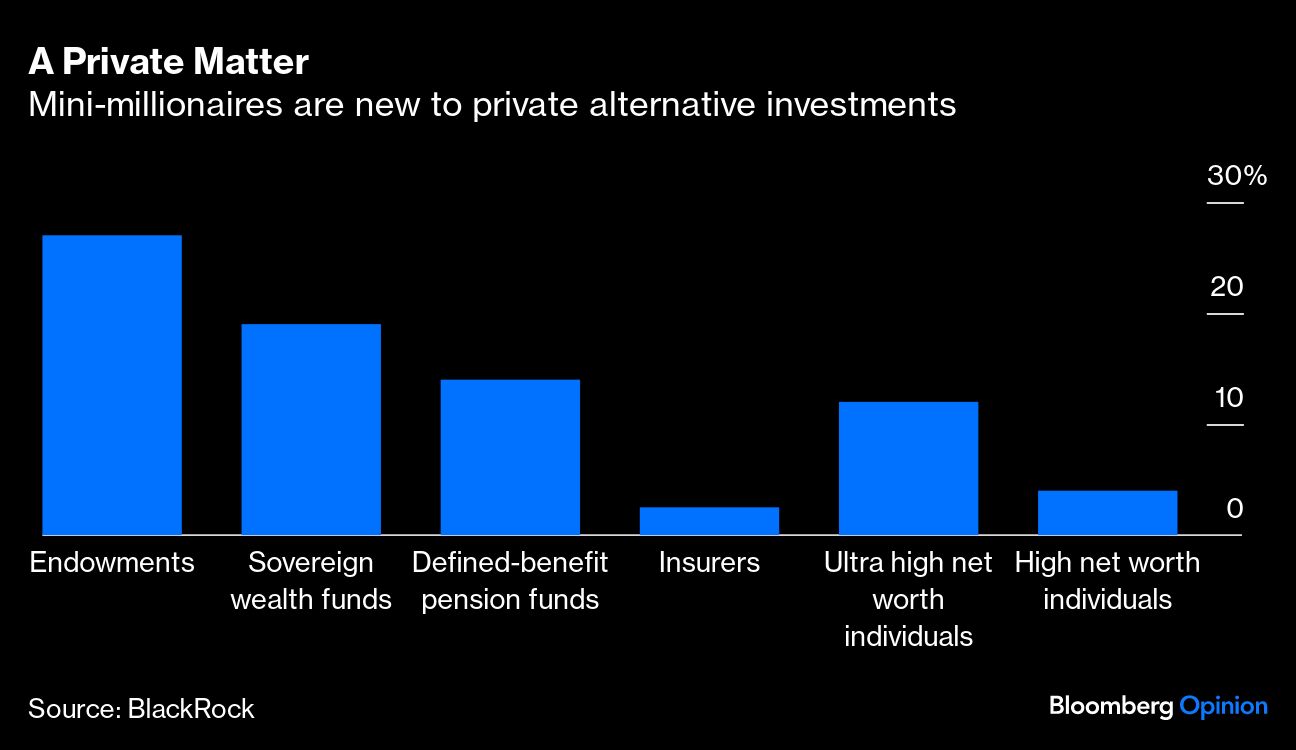

Seen in this light, Blackstone’s dash for mini-millionaires is a no-brainer. They are easy cash cows. The wealthy that Blackstone’s retail PE fund is targeting have only 11% to 13% of their assets invested in alternatives, versus 26% to 28% for endowment funds.

By the same token, BlackRock may also want more of the “high quality” earnings that Blackstone enjoys. Fees earned by alternative asset managers are more sticky, because their investments have a much longer time horizon than stocks, and investors are mentally prepared to be patient.

The revenue-sharing deal that BlackRock struck with GIP, which holds stakes in airports in Sydney and London, is telling. It would receive 100% of the management fees, but only 40% of the performance fees from future GIP funds. It’s a sign that BlackRock wants the “sticky” earnings.

By its own account, BlackRock is seeing dramatic industry shifts. In the core US exchange trade funds space, the iShares ETFs are losing ground to Vanguard and aggressive rivals such as JPMorgan Chase & Co. and Dimensional Fund Advisors. Meanwhile, price wars are widespread. When BlackRock launched its first Bitcoin ETF in January, it started off at a 0.3% annual fee, which was already below analyst expectations, but had to lower to 0.25% after smaller peers undercut it.

Perhaps this is the peril of an asset manager under the constant scrutiny of public investors. If it was privately held like Vanguard, it would be only responsible to investors in its funds, allowing more focus on delivering returns. But as a publicly listed entity, it has to worry about earnings quality. In the world of Blackstone and BlackRock, raising money is becoming more important than making money for clients. Their ultimate loyalty has to be to their shareholders.

A message from Advisor Perspectives and VettaFi: Advisors: You're Invited to Exchange! Nothing would be a better start to the new year than if you joined us at Exchange, an in-person conference for members of the financial services community in Miami, Florida on February 11-14th. For a limited time, we're offering you a free Exchange ticket!* Register today with code WINTER24 to claim your pass.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

More Evergreen Topics >