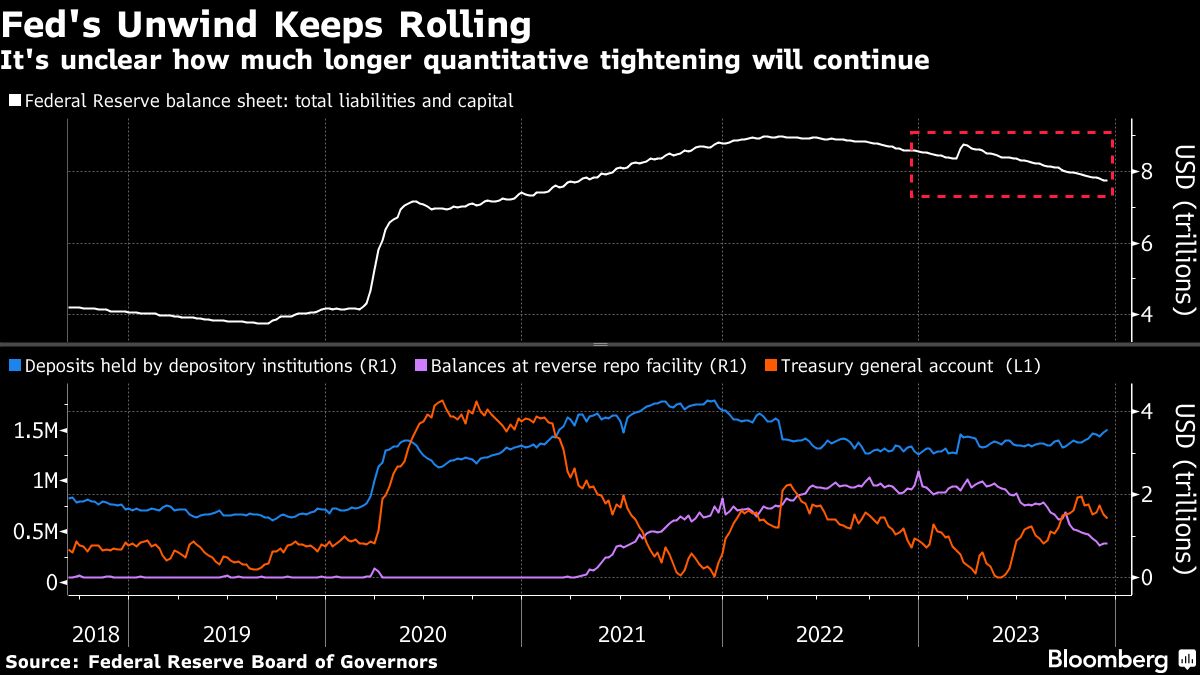

The Federal Reserve is trying to find the right time to start deliberating about how it will extract itself from its balance sheet unwind, a signal that the end might be closer than previously expected.

In the minutes of last month’s Federal Open Market Committee meeting, several participants suggested it would be appropriate to begin discussing the technical factors that would determine when the US central bank slows the pace of its balance sheet runoff, a process known as quantitative tightening. Participants remarked the Committee’s plans indicated it would slow and then stop shrinking its balance sheet when reserve balances are “somewhat above the level judged consistent with ample reserves.”

A debate has been simmering in recent months over whether the Fed is misjudging how much it can tighten without causing dislocations in places like the market for overnight repurchase agreements, part of the essential plumbing of the financial system.

While bank reserves — currently at $3.48 trillion — are well above the levels seen when the Fed started unwinding its balance sheet in 2022, there’s concern that the amount of reserves is not as abundant as policymakers believe. Central bankers in 2019 learned a lesson when a different overnight market rate soared five-fold to as high as 10% and the central bank was forced to intervene.

“As they say, everyone has a plan until they get hit,” said Blake Gwinn, head of US interest rate strategy at RBC Capital Markets, which sees the Fed winding down QT in mid-2024. “The last go-round they got ‘hit’ by the September 2019 repo blowout and immediately reversed course,” Gwinn said.

For over 18 months, the Fed has been letting as much as $60 billion in Treasuries and as much as $35 billion in agency debt holdings mature every month.

The last time the central bank attempted to halt its balance sheet unwind in 2019, it was only letting as much as $30 billion in Treasuries and as much as $20 billion in agency debt run off — nearly half the size of the current plan. In May of that year, the Fed slashed the reinvestment cap for Treasuries to $15 billion before eliminating the limit entirely in August, while continuing to let its mortgage-backed securities holdings roll down.

Even before that, money market rates had already been signaling that reserves were scarce. The effective fed funds rate — the central bank’s policy target — was moving higher, along with other short-term rates, and required policymakers to adjust their tools in order to maintain control.

Recently, after roughly four years of orderly trading — with banks and fund managers locking in funding at the end of each month, quarter and year — volatility has erupted again. Gyrations in repo rates sent one benchmark to a record in the past week, while the market for short-term loans collateralized by Treasuries fluctuated.

To be sure, the latest disruptions were of a lesser degree than those four years ago and required no intervention. Still, the recent episodes shine a light on the increasingly delicate balance between the Fed, banks and other institutions that helps the overnight funding market function properly.

Volatility in short-term funding markets can hinder central bankers’ ability to manage monetary policy. Funding dysfunction also poses risks to the broader economy by potentially pressuring borrowing costs for the government and beyond — at a time when benchmark interest rates in the US are already at two-decade highs.

“The Fed is like a scout: they always want to be prepared,” said Gennadiy Goldberg, head of US interest rate strategy at TD Securities. “On the one hand, the earlier prep for ending QT is a good thing. On the other, they have to figure out how to do so without signaling to markets that the end of QT is nigh,” Goldberg said.

A message from Advisor Perspectives and VettaFi: The crypto landscape is on the brink of a revolution. Are you prepared for what's coming in 2024? Dive into expert insights on the future of crypto and its influence on next year's market. Join us at the Crypto Symposium on January 12th at 11 am ET. Click here to register.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Alexandra Harris