Albert Edwards, Societe Generale SA's chief global strategist, hasn't been the top-ranked Extel survey macro analyst for the past 20 years because he's an optimist. He's famed for his permabear outlook, predicting "ice-age" negative western bond yields mimicking the lost decades of growth that Japan suffered. Yet, in person, he’s far from the apocalyptic Grinch his research notes might suggest. His penchant for wild, flowery shirts (check out his X profile) reveals a cheerful disposition. Nonetheless, there’s no doubt he can skewer lazy group-think or counterproductive financial policies with alacrity.

Edwards, 62, started in the City of London 40 years ago as a Bank of England economist after completing a masters degree in economics at Birkbeck, University of London. But he cites his three-year stint as an asset manager at Bank of America Corp., coinciding with the 1987 Wall Street crash, as fundamental to how he thinks — and writes — about the world.

Back in the day, forests-worth of research documents were piled high on fund managers' desks, fated never to be read. His concise and iconoclastic style is the opposite of that highbrow fodder. While cheerfully admitting his economic calls are often wrong, at least Edwards is never dull. Challenging the consensus by diving deep into obscure data is what his followers appreciate, providing a reality check for portfolio managers seeking to test their in-house thinking. I, for one, look forward to his doomster scribblings, although I reckon his pessimism is currently a bit overdone. However, his dismay about the likely repercussions of central bank interference in setting the price of money in recent years is spot on.

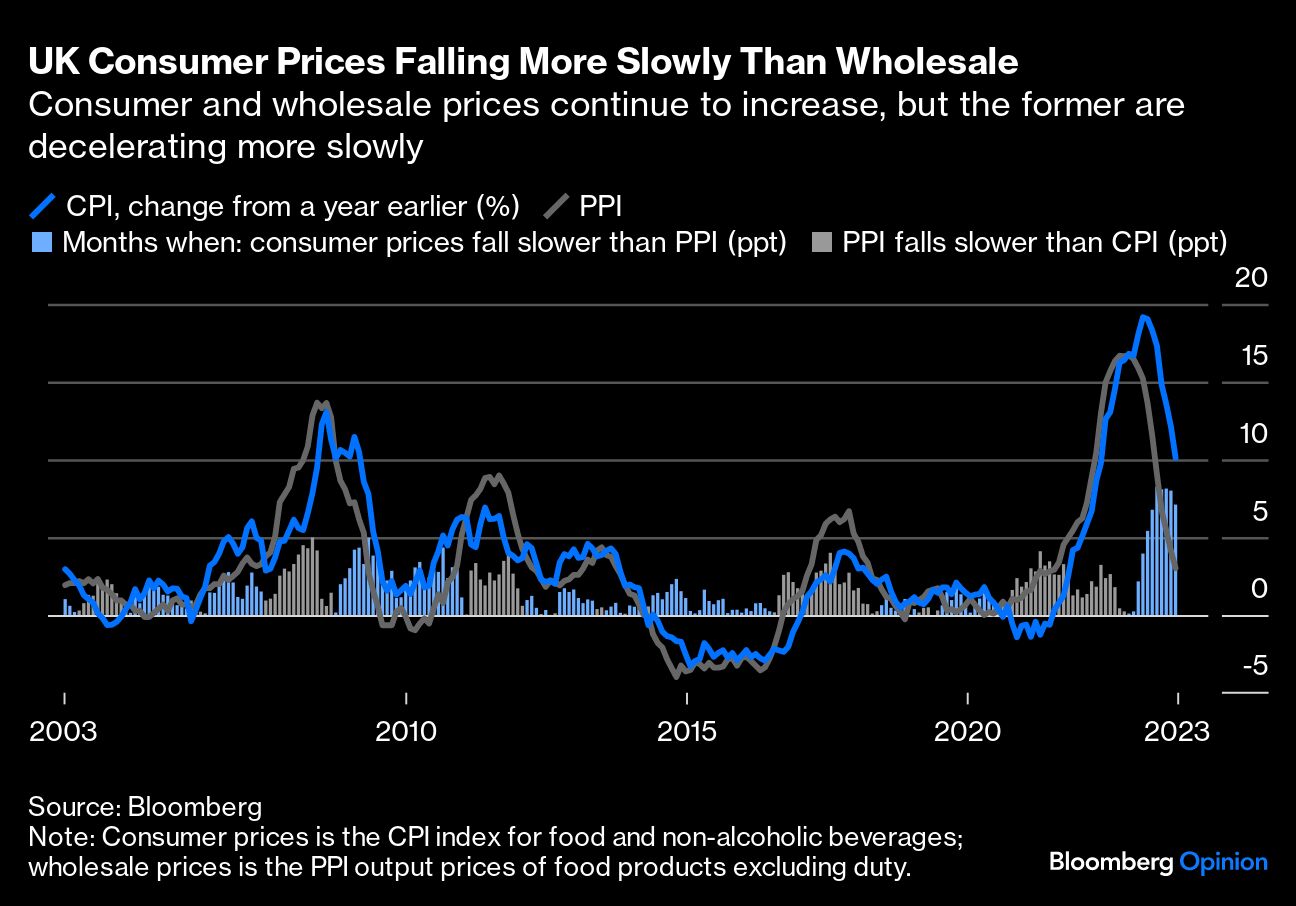

One of his current peeves is how corporates have gamed the sharp upswing in inflation to boost margins, profiting from so-called greedflation. As a consequence, consumer prices have probably risen more than is warranted, with excess savings accumulated during the pandemic making consumers less price-sensitive — but it's a hard point to prove. Edwards suspects margins are being boosted again as food prices decline because those reductions aren’t being passed on. The highly competitive UK supermarket sector has come under particular scrutiny, but regulators are missing the real culprits — large food and goods producers. Inflation is falling at a suspiciously slower pace in this cycle than previously.

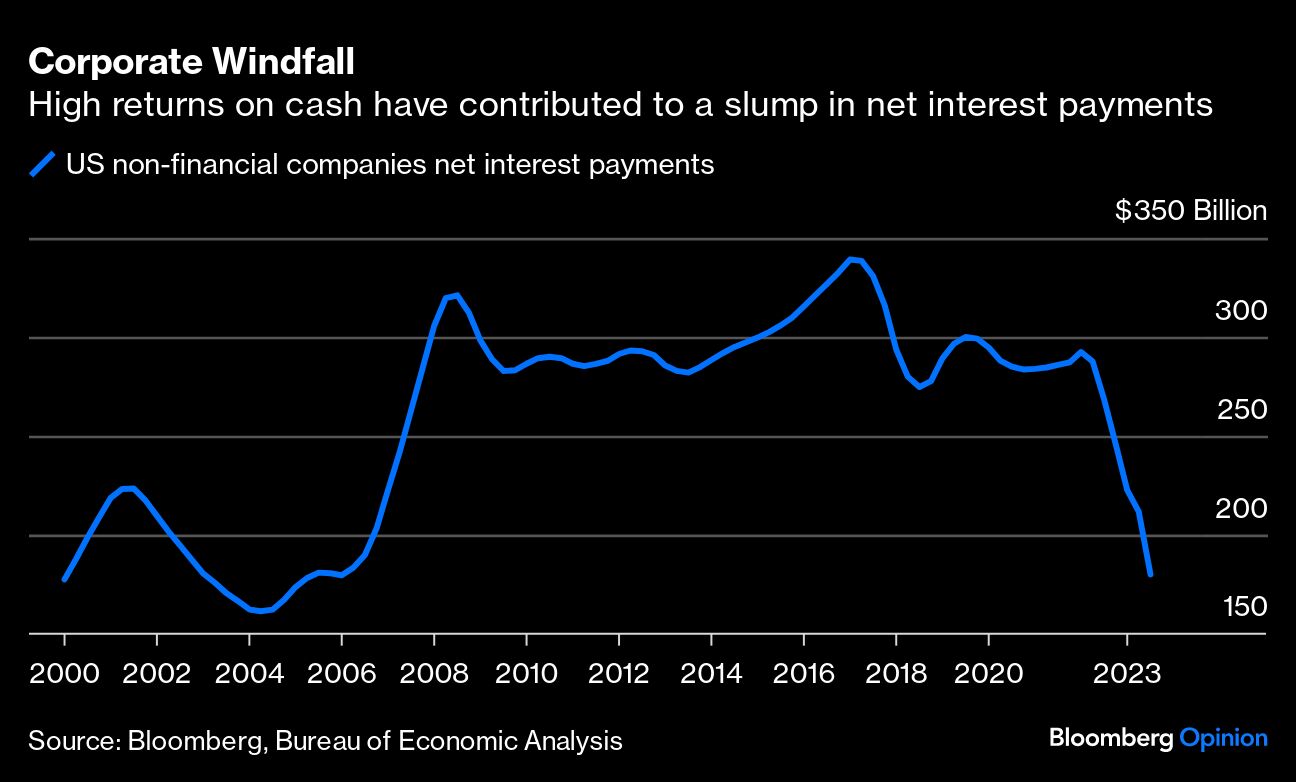

Another anomaly currently bugging Edwards and his team is the way that much higher official interest rates aren't affecting corporate behavior nearly as much as the Federal Reserve might have expected. Large firms with ready access to debt capital markets are benefiting from having raised debt at super-low interest rates during the pandemic. They’re now parking cash that earns more in interest than the coupons they pay bondholders — providing a windfall, but one that will prove temporary.

Edwards says he's not as bearish as he has been — the ice-age is over — but he says the medium-term outlook remains unclear, and that excessive central bank interference over the past 15 years has just delayed a financial reckoning. He reckons Europe is already in recession, with the US not far behind. Though not a monetarist economist, he finds it bewildering that policymakers are ignoring sharp declines in both money supply and bank lending, as those contractions increase the risks of a hard landing. I couldn’t agree more.

He’s sticking with the argument that a US recession always accompanies an inverted yield curve in the Treasury market, even though short-term rates have started to fall closer to lower long-dated yields. He reckons governments and central banks are unlikely to stand aside and allow some Schumpeterian creative destruction from a downturn, which could correct some of the misguided policies of the last decade. The pandemic saw governments gleefully cross the fiscal Rubicon and pump money straight to households; central bankers may have thrown monetary policy into reverse but the fiscal splurge continues unabated.

Too many zombie firms will need bailing out to limit rising unemployment. So he expects a "clattering" of rate cuts — and even a return to quantitative easing as deflation reappears. The Netherlands and Belgium are already experiencing negative inflation; he’s very bearish on China’s economy and how that might exacerbate deflation globally.

His ice-age thesis was mocked for years — until it was proven to be prescient when interest rates tumbled and the universe of bonds with negative yields swelled to a peak of $18 trillion three years ago. He now looks for US 10-year yields to retrace back below 2% after climbing to 5% in mid-October, though he’s not predicting a return to 2020’s record low 0.65%.

Edwards envisages a collapse in tech stocks similar to the 2001 rout. Many companies have never been through a downturn, as even the 2008 global financial crisis brought benefits to the new economy. With tech contributing a third of US equity market value, and the Magnificent Seven having risen by two-thirds this year, elevated valuations could run out of road. He sees worrying signs of layoffs and bankruptcies in the logistics sector that will presage downward earnings revisions. Still, he’s optimistic that a cathartic clear-out will benefit value stocks as investors eschew cyclically driven equities masquerading as growth stories.

Until then, Edwards recommends hiding in the safety of longer-duration fixed income and gold. These might not be the most exciting recommendations available on Wall Street, but that’s not why investors listen to him. Rather, it’s the forensic quality of his analysis and contrarian approach they rely on to challenge their thinking. The world could do with more voices willing to challenge the financial orthodoxy.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.