Cevian Capital AB’s $1.3 billion bet on UBS Group AG is unusual in more ways than one. The Stockholm-based investment firm is typically a quiet activist, working behind the scenes to steer management thinking. This time it’s being very public about what looks like a straightforward value play.

Cevian’s backing, which it revealed on Tuesday, is a big vote of confidence for the Swiss bank. The stake might be just 1.3% of UBS’s shares, but it’s about 10% of the fund’s assets under management. The investor has been talking to UBS’s management since before it started building its stake in April. Relations are friendly now, but things could get frosty if UBS fails to fulfil Cevian’s grand hopes, which look hard to reach.

Lars Förberg, Cevian chief executive officer, told Bloomberg TV on Tuesday that UBS’s management was doing an excellent job integrating former rival Credit Suisse after its emergency takeover and things were heading in the right direction. Förberg thinks UBS can catch up with the current valuation of Morgan Stanley within two to three years, which would roughly double the Swiss bank’s share price.

The key to that thesis, though, is more growth and better profitability in UBS’s wealth business, which Förberg called the largest truly global money manager for the rich. (Morgan Stanley has more assets, but it’s very focused on the US.) One big question is whether wealth remains a slam-dunk strategy for banks: For more than a decade, ultra-low interest rates and vast quantities of central bank money held volatility down and lifted asset prices up. That world may be gone for good.

UBS shares have already jumped by more than 50% since Credit Suisse’s failure in March, but Förberg said the “downside protection on UBS is immense.” Another partner at Cevian told Swedish TV on Tuesday it was “impossible to lose money” on the bank, according to Bloomberg News. If that’s not tempting the fickle gods of finance, then I don’t know what is.

So what could go wrong? UBS has made a strong start to carving up Credit Suisse, but in many ways its work so far has been the easy part. It made faster headway than expected in the third quarter on cost cuts and sales of unwanted assets, but it was helped by the many Credit Suisse bankers who walked away rather than waited to see if they would keep their jobs.

The challenge in wealth management is different: UBS is trying to keep large chunks of Credit Suisse’s wealth teams and clients, while reducing risk and bolstering compliance to avoid the kind of scandals that Credit Suisse generated. Success on this front will take a while to show.

The job of merging the core Swiss domestic banks is also tricky and politically sensitive: Cutting costs and staff will need to be handled carefully. It’s a more traditional and thus complicated integration job.

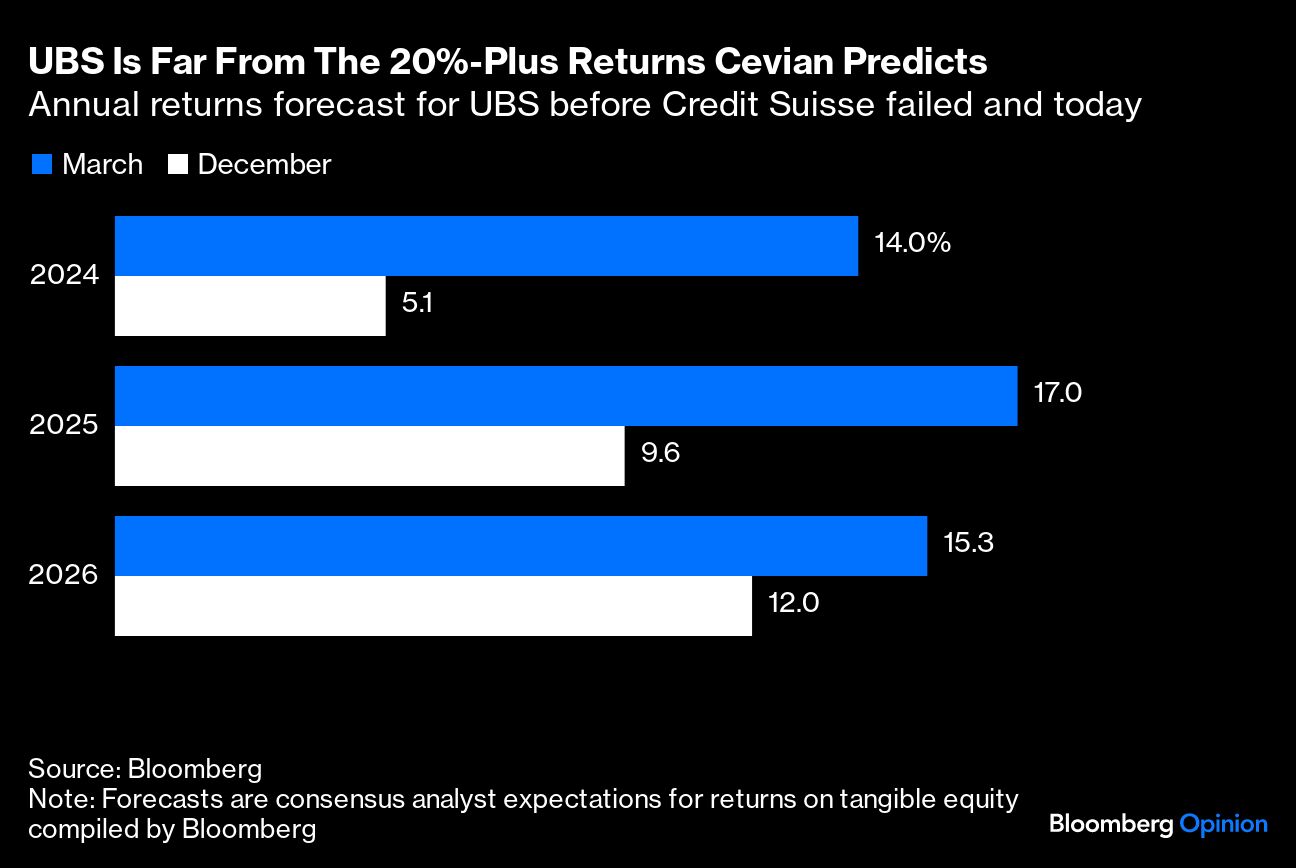

Assuming this all goes to plan, UBS expects to make a return on tangible equity of about 15% by the end of 2026. Cevian said the bank should make returns of 20%-plus. That’s ambitious — and where Cevian’s activism and pressure on the management will start to matter.

Before Credit Suisse went down, UBS was riding high in valuation and performance terms. Back then, analysts were forecasting a return on tangible equity of 17% for 2025 slowing to 15.3% in 2026. Now consensus forecasts compiled by Bloomberg are for 9.6% in 2025 and 12% the year after.

To reach the heights envisaged by Cevian, UBS needs the global wealth bandwagon to keep rolling and to grab a bigger and more profitable share. Looking after the world’s rich has been a great business since the financial crisis with central bank support proving such a tailwind that it’s been blamed for exacerbating inequality.

The next decade is unlikely to look the same. Some investors expect the years ahead to be much more volatile in markets and economies with more variable inflation, geopolitical shocks and generally higher interest rates. That’s a world that could be more lucrative for market makers and banks offering hedging and risk management than for wealth management.

For Cevian and UBS, the hope will be that if such conditions take a toll on wealth, the world’s rich will be happy to pay more for good advice on how to protect their money.

One route to a higher valuation could be to move the bank’s listing to New York — Cevian made a 20% gain on CRH Plc by convincing the Irish building-materials company to do just this. For now, Förberg says UBS’s Swiss listing is “appropriate.”

UBS’s stock is currently worth 1.1-times its forecast tangible book value in a year’s time, which compares with 2.1-times for Morgan Stanley. There is definitely room for UBS’s share valuation to improve, but generating the 20%-plus returns needed to double it looks like a long shot.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul Davies