For most of the summer, the chatter in the bond market about swelling US deficits — and the depressing effect it was having on the price of Treasuries — was incessant.

Few, if any, were more vocal on the topic than Ed Yardeni, the godfather of the bond vigilantes. Investors, Yardeni said back in August, “are quite concerned.” The price action seemed to underscore the angst. By October, the yield on the benchmark 10-year bond had soared above 5% for the first time in 16 years.

Then, almost just as quickly as they rose, yields plunged — all the way back down to near 4%. So what happened to all the hand-wringing about reckless government spending and the ballooning national debt? Sure, the bond rally was sparked by a different development — speculation the Federal Reserve will start cutting interest rates next year — but still, the tough vigilante talk disappeared rather abruptly.

Yardeni is unfazed. Deficit concerns, he argues, don’t manifest themselves in the market consistently, day after day. When something pulls investors’ attention elsewhere — like the mounting evidence that the economy is slowing — they will backburner those worries. The jitters remain, though, Yardeni says.

The “vigilantes will be back,” Yardeni, the founder of Yardeni Research Inc., said in an interview. The surge in government spending in recent years and the jump in interest rates is creating a dangerous fiscal mix, he said. “This is not an issue that will go away unless it’s fixed. If anything, the deficit outlook is probably worse than is being anticipated.”

There are plenty of skeptics out there who saw the summer rout in Treasuries as something of a one-off event. Prominent in this camp is Steven Major, a perennial bond bull at HSBC Holdings. While he acknowledges that he didn’t anticipate the market impact this year of the bond-supply increase, he’s adamant that over time the deficit is a sideshow.

“Supply can have a short-term impact, when there is an imbalance with demand,” Major said, “but over the longer-run it is not the main driver of bond yields.”

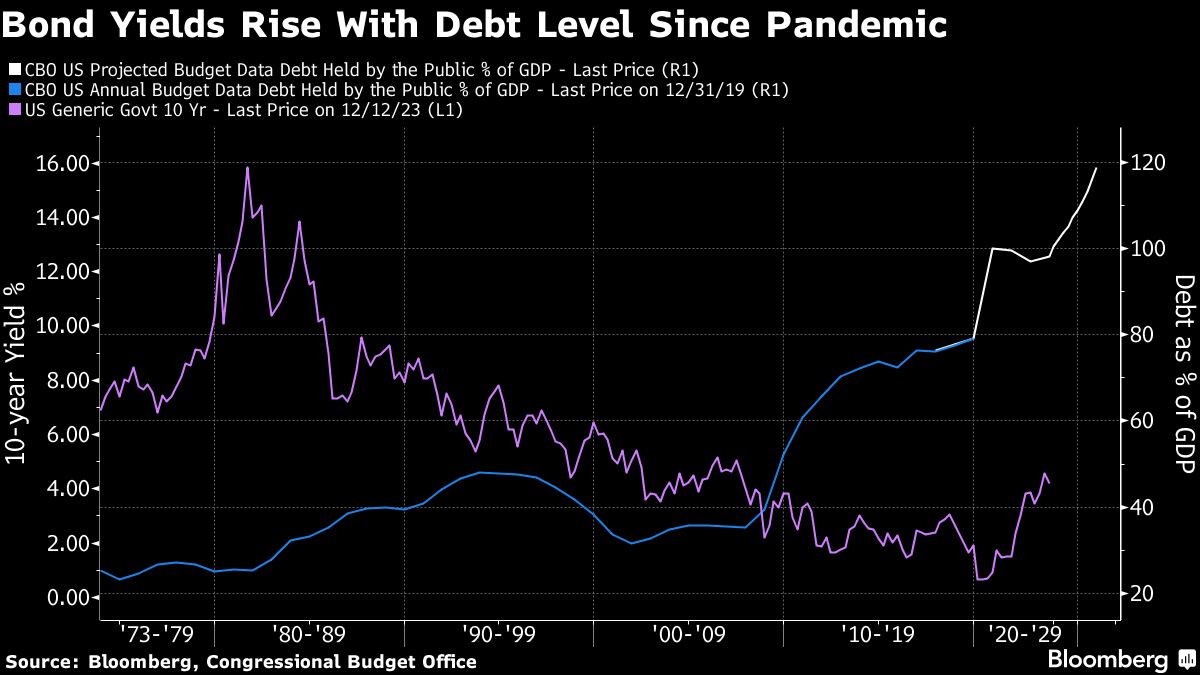

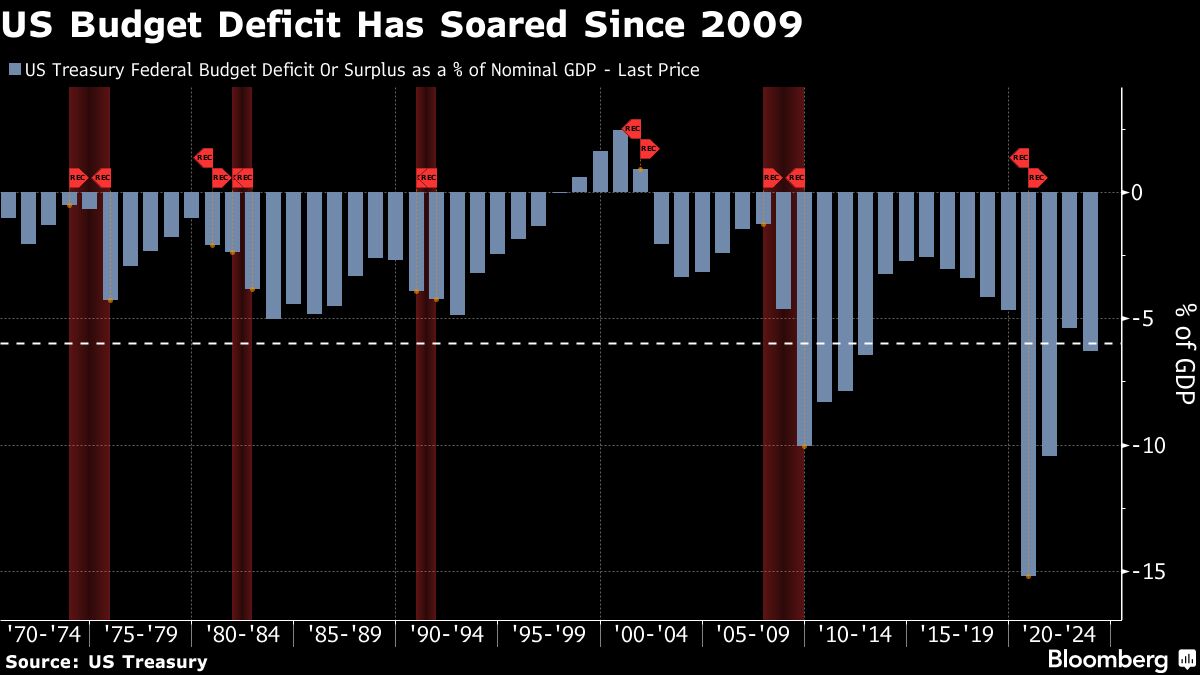

The selling intensified in August after Fitch Ratings stripped the US of its AAA credit rating. There was nothing novel about the rationale — primarily, the swelling deficits — and yet the move re-sharpened investors’ focus, at least briefly, on the magnitude of the spending imbalance.

Fitch estimates the government will post a deficit equal to more than 6% of gross domestic product this year, a number larger than any posted in the six decades before the global financial crisis. That it comes amid a year of strong economic growth — which tends to lift revenue and hold down expenses — makes it all the more jarring.

At least to Yardeni and like-minded types. He says he can tell the supply concerns haven’t truly gone away because his clients now closely monitor bond auctions for signs of strong or weak demand.

“In the past, you could leave supply out of the pricing model,” he said. “But now, you have to be aware of how the auctions are going; you have to be aware of the political developments; you have to have a sense of where the deficit is actually going.”

Yardeni heaped praise on Janet Yellen, the treasury secretary, for her handling of the auctions. He called her decision to scale back the size of longer-maturity bond sales while ramping up issuance of short-term T-bills “clever.” The move, while not without risk, further juiced the bounce-back rally over the past two months.

There’s been a “realization that the Treasury can fine tune, it can manipulate the bond market by simply reducing the supply of long bonds for a while,” he said. “The market seems to have settled down pretty well here.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Ye Xie