An uncontrolled popular urge to speculate in financial markets is giving regulators a headache everywhere. It is especially worrying in India, where trading in futures and options is now more than 400 times bigger than the underlying cash-market turnover. This is a slow transfer of wealth from the real economy to a financial elite, the full impact of which may only be felt when it’s too late to stop it.

The Securities and Exchange Board of India’s crackdown on social media influencers peddling advice is a losing battle. Although nine out of 10 individual traders are losing money, retail investors can’t get enough of derivatives. A smartphone-led gamification of investing is complete.

It wasn’t always like this. Until the early 1990s, financial markets and mavens never had a large sway over the country’s economy or public imagination. People kept their money at state-owned banks. Direct stock ownership was rare. Those with surplus savings bought slips of paper from the Unit Trust of India, a black box of an investor that regularly paid 20%-25% as dividends on capital. That was the extent of middle-class Indians’ greed for yield.

Things began to change when the economy opened up. Harshad Mehta, a flashy Mumbai stockbroker, acquired the moniker of “Big Bull.” He became the first Indian to buy a Lexus LS400, and in early 1992 took out an eight-column newspaper ad with the headline: “Harshad Mehta is a liar,” implying, of course, that he was just the opposite. By the end of that year, however, Mehta had been arrested for masterminding a huge securities scam. The erosion of public confidence in a market that had only recently started accepting foreign institutional money led to a slew of changes: electronic trading, guaranteed settlements, replacement of paper-based share certificates with account entries to stop counterfeiting, and — starting in 2000 — exchange-traded derivatives.

It is this last reform that has become too much of a good thing. The SEBI’s research shows that more than 80% of individual traders dabbling in options are men. They’re mostly young: The 20-to-30-year-old age group is witnessing the biggest surge. For the few who’re lucky to turn a profit, anywhere between 15% to half of their take is going toward paying brokerage, clearing fees, exchange and regulatory charges and taxes. As for the 89% of traders losing money, transaction costs are making their pain worse.

A recent study in the Lancet shows a 73% increase in suicide deaths between 2014 and 2021 among Indian men earning roughly between $6,000 and $12,000 annually, enough to qualify them as affluent. Men who are poorer or richer have seen a smaller jump in suicide rates. It isn’t possible to draw a definitive link with speculative trades gone wrong, but newspaper reports do suggest stock-market losses are driving even young professionals to distress.

The lure of easy money is becoming irresistible amid high unemployment, stagnant wages and continuous media exposure to the conspicuous consumption by the wealthy, a lethal combination of temptation and desperation. Asking brokers to only take on clients who have the adequate risk appetite will be largely a performative exercise. Regulating individual traders’ access to leverage may be the only prudent solution.

Those who decry any such limits as draconian worry about investor sentiment. The nation’s stock market recently topped $4 trillion to become the world’s fifth largest by value of listed shares. Besides, the 500% surge in the number of India’s futures and options traders since 2019 is part of a pandemic-induced global phenomenon. Options, particularly short-dated contracts, are also the hottest thing on Wall Street.

There is a difference, however. While a much-awaited US-listed Bitcoin exchange traded fund may soak some of risk-taking excess, Indian regulation and taxation has taken the air out of cryptocurrencies, choking off local digital-asset exchanges. The entire burden of retail speculation is on equity options.

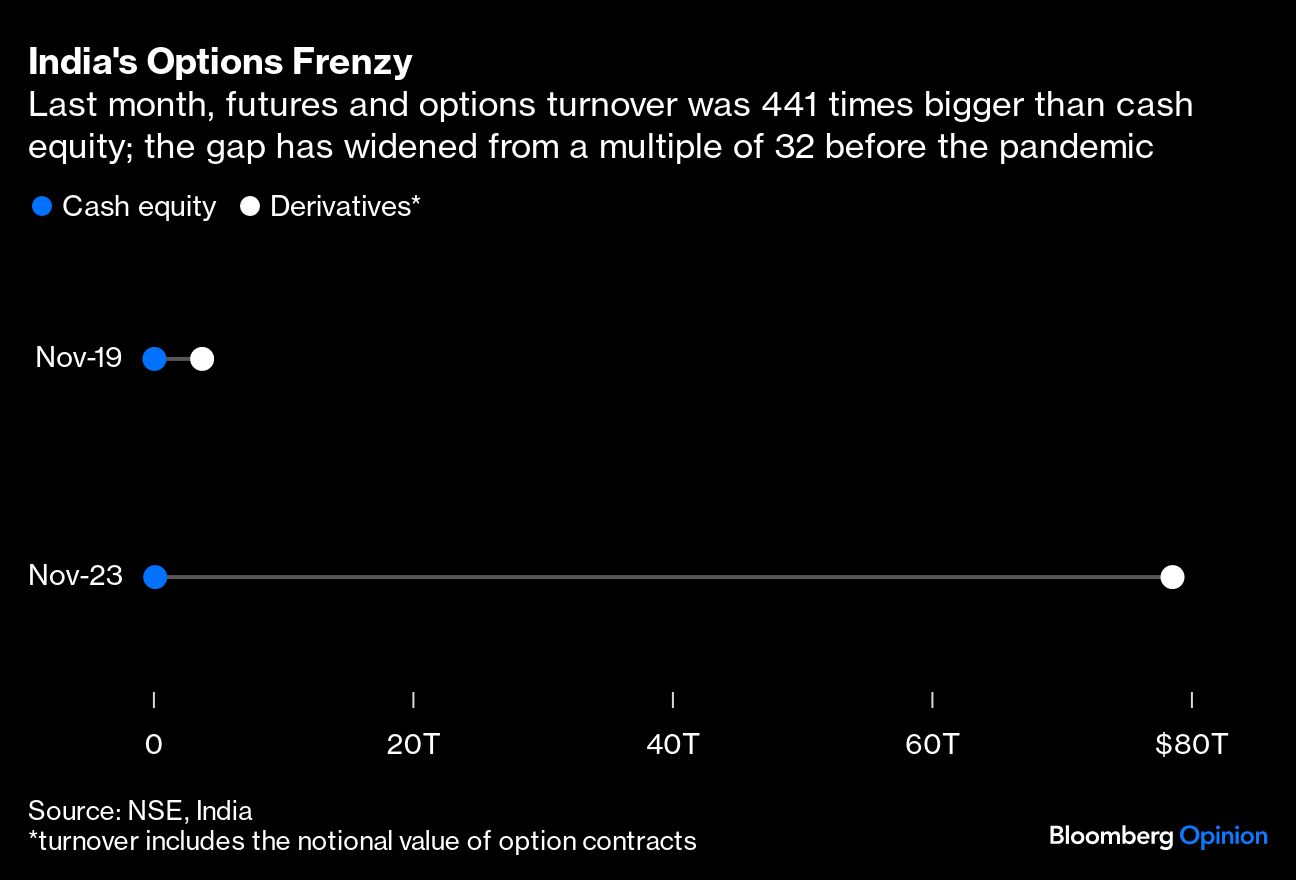

Unlike cryptocurrencies, which are yet to demonstrate any social utility, the main benefit of derivatives is that they offer low hedging costs to investors. But while that’s a good enough reason to keep them well lubricated, it doesn’t mean drowning them in a deluge of liquidity. Last month’s total turnover of $78 trillion from futures and options on indexes and stocks trumped the $178 billion from shares changing hands on India’s National Stock Exchange by a multiple of 441. No other major market in the world is as lopsided.

Every day witnesses the expiry of some highly traded contract in a flurry of last-minute activity. Brokerage apps are lobbying to extend trading hours to 9 p.m. local time, even though traditional intermediaries are opposed to idea. If the markets are open, it will be impossible to wean day traders away from their terminals.

And to what end? Harshad Mehta’s Lexus got auctioned. The middle class could lose its peace of mind. The money flowing as transaction costs would (leaving aside the government’s share) go to stockbrokers and exchanges. While too much concentration of wealth and power in the hands of a narrow financial elite is not a great outcome anywhere, premature peak finance can be especially damaging to a developing country that still needs to churn out a lot more real output to get rich.

Market trends are shifting – is your investment strategy keeping pace? Join industry experts as they delve into the equity and bond markets, offering insights into the 2024 outlook. Register for our Market Outlook Symposium, on December 14th at 11 am ET. Click here.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Andy Mukherjee