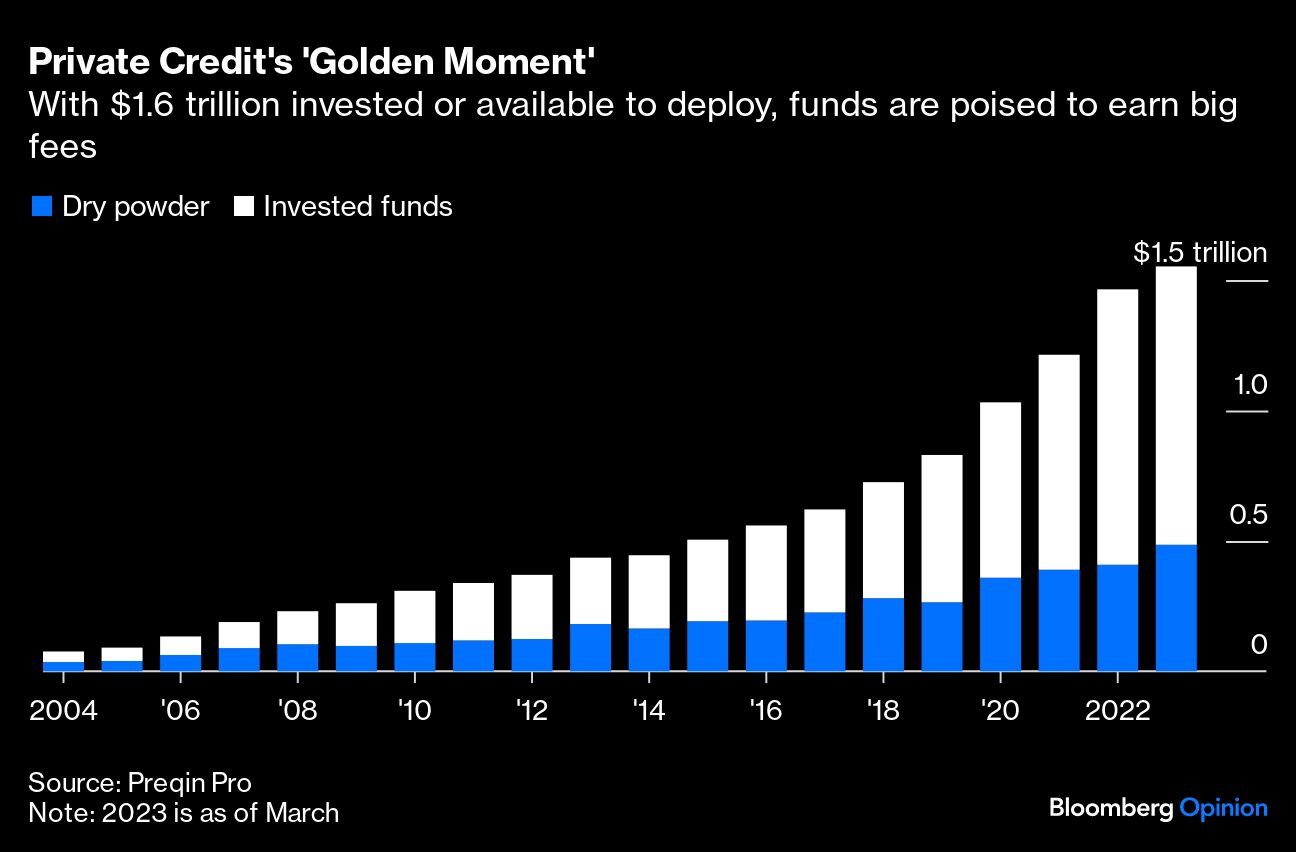

The $1.6 trillion private credit market is enjoying a “golden moment,” in the words of one Blackstone Inc. executive, as banks retreat from risky lending and investors flock to funds offering double-digit returns on corporate loans. But those jumping on the bandwagon shouldn’t forget private credit fees are very lucrative too. As this asset class goes mainstream and mints billionaires, investors — aka limited partners — should insist on lower costs, and oppose incentives that can reward managers for little effort.

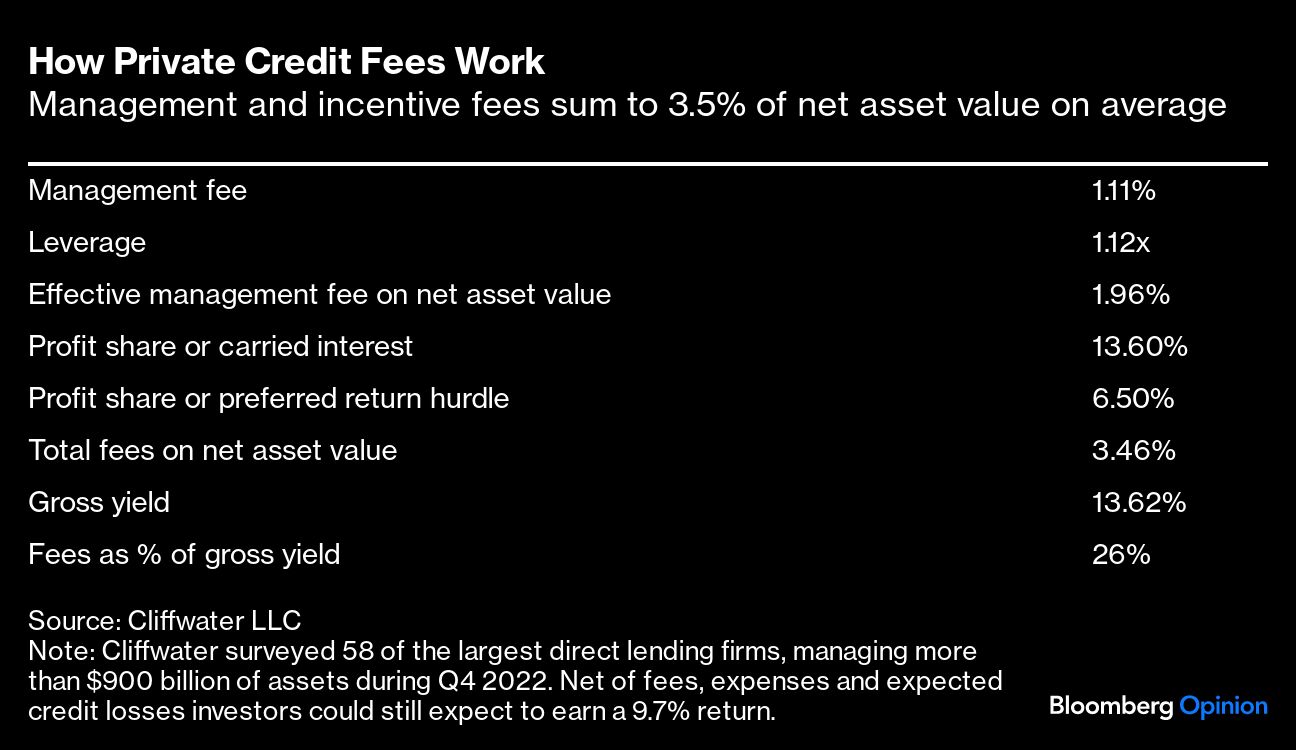

From a fee perspective, private credit is a sweet gig. There’s a 1% to 2% asset-management fee1, plus a further take of around 15% of profit once a specified return threshold is exceeded, typically around 6%. Once that triggers, a “catchup” ensures the managers receive their share of the entire profit, not just the income in excess of the hurdle.

A 6% hurdle might have made sense when interest rates were near zero, but it represents little challenge now that US and UK benchmark rates are above 5%. Private credit loans have floating interest rates, so borrowers are often paying 10% once a spread is included. In other words, managers can’t really fail to get their performance bonus, providing defaults don’t spoil the party.

“If you have a credit fund that is now enjoying 500 basis points of excess return because the base rate has gone up, that basically all flows into that accrued incentive fee bucket,” Michael Arougheti, co-founder of private credit giant Ares Management Corp. told investors in September. Fixed hurdle rates are “well-entrenched market conventions” and “nobody” is trying to impugn their value, he added.2

Of course, the fact that private credit funds are easily meeting performance hurdles implies clients are doing well too. But I’m not alone in wondering wonder why this financially sophisticated industry doesn’t use flexible incentive hurdles instead, to prevent fund managers automatically winning the lottery just because interest rates increase.

This would be far better than just arbitrarily increasing the hurdle, which might backfire if rates tumble again and managers then feel compelled to take more risk.3 Yet notwithstanding some exceptions, incentive hurdles linked to overnight reference rates haven’t caught on.

It seems like everyone in finance now wants to offer private credit, even though investors are typically constrained in how much they can allocate to non-public investments. But fees haven’t compressed as much as one might expect. The industry is dominated by a handful of large firms that in theory can achieve economies of scale and pass those benefits onto limited partners via lower fees. On the other hand, investors may have less ability to negotiate with these giants, whereas smaller, lesser-known funds may face more pressure to cut fees to attract capital.

Direct-lending fund fees are around 3.5% on average, not including 0.5% of administrative expenses, according to Cliffwater LLC research. In contrast, an actively managed bond fund might charge roughly 0.4% in fees.

Of course, overseeing a private credit fund requires more labor and effort than investing in public debt; it starts with originating loans, due diligence and negotiating covenants, then monitoring performance, and restructuring credits when things get dicey.

"The fee element is important but it's not necessarily the most critical element when selecting the right private credit manager,” Thibault Sandret, head of private credit at bfinance, an investment consultancy, tells me. “And if the fee structure is ultra-friendly to limited partners you need to ask yourself why. I do not believe all general partners are equal or that this market will be commoditized. The best private debt managers can achieve attractive risk-adjusted returns thanks to their privileged access to deal flow and their ability to avoid any credit losses."

It’s no coincidence that private credit fees are similar in design to those charged by private equity — many investment firms offer both, and they use private loans to help fund their buyouts.

Private credit fees are lower than PE’s 2% management fee and 20% profit share; another welcome difference is that private credit typically charges fees only on invested capital rather than committed capital.

That’s just as well, though, because private credit funds also target less lofty and more predictable returns than a PE owner, which must increase the value of a portfolio company when it’s sold. In contrast, a private debt manager only needs to worry about getting interest and capital returned to them, and they’re often first in line to get paid in bankruptcy. As Blackstone founder Steve Schwarzman opined in September, if you can earn a 12% return for lending to companies, “what else do you want to do in life?”

While incentive fees give the fund manager some skin in the game, I sometimes wonder whether a bonus is necessary at all. KKR & Co. and Carlyle Group Inc. aren’t demanding profit incentives on new European direct-lending vehicles , for example.

Incentive fees aren’t the only thing private credit investors need to watch out for. Publicly traded business development companies (BDCs) — closed-end private credit funds aimed at US retail investors — often charge management fees based on gross rather than net assets. In other words, there’s a levy on the assets acquired with debt, not just the ones purchased with investors’ money. Of course the fund manager has to oversee all the assets, regardless of how they were funded, but the effect is to inflate the total fee earned.

“There’s really no question that lower fees would benefit retail shareholders of BDCs,” Robert Dodd, BDC analyst at Raymond James, told me. “Regrettably these are set at ‘what the market will bear’ rather than structured de novo based on what is appropriate for the asset class and its target returns.”

Fees for non-traded BDCs tend to be lower; BCRED, Blackstone’s private credit fund for wealthy individuals, sets a good example: it charges a management fees of 1.25% on its $26 billion of netassets, plus a modest 12.5% of investment profits.4

But Schwarzman’s firm is still doing fine. Launched in early 2021 when interest rates were at rock bottom, BCRED only needs to exceed a 5% return to trigger incentive payments, which of course it has achieved comfortably. Hence the giant fund is still on track to earn almost $750 million in management and incentive fees this year by my calculation.5

It truly is a golden era for private credit managers. Investors should require they outperform for those rewards.

1Depending on whether you're referring to gross or net assets.

2Ares donate a portion of its incentive fees to charity.

3Some alternatives are explored in this Macfarlanes study.

4Blackstone Secured Lending Fund, its publicly traded BDC, also has a low management fee.

5Total fees were more than $550 million in the first nine months of this year.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Chris Bryant