Across Wall Street, analysts and investors had cheered 2023 as the year of emerging markets, only to be burned by a relentless climb in US Treasury yields. Now, as the Federal Reserve looks set to end its most-aggressive monetary tightening campaign in a generation, they’re at it again.

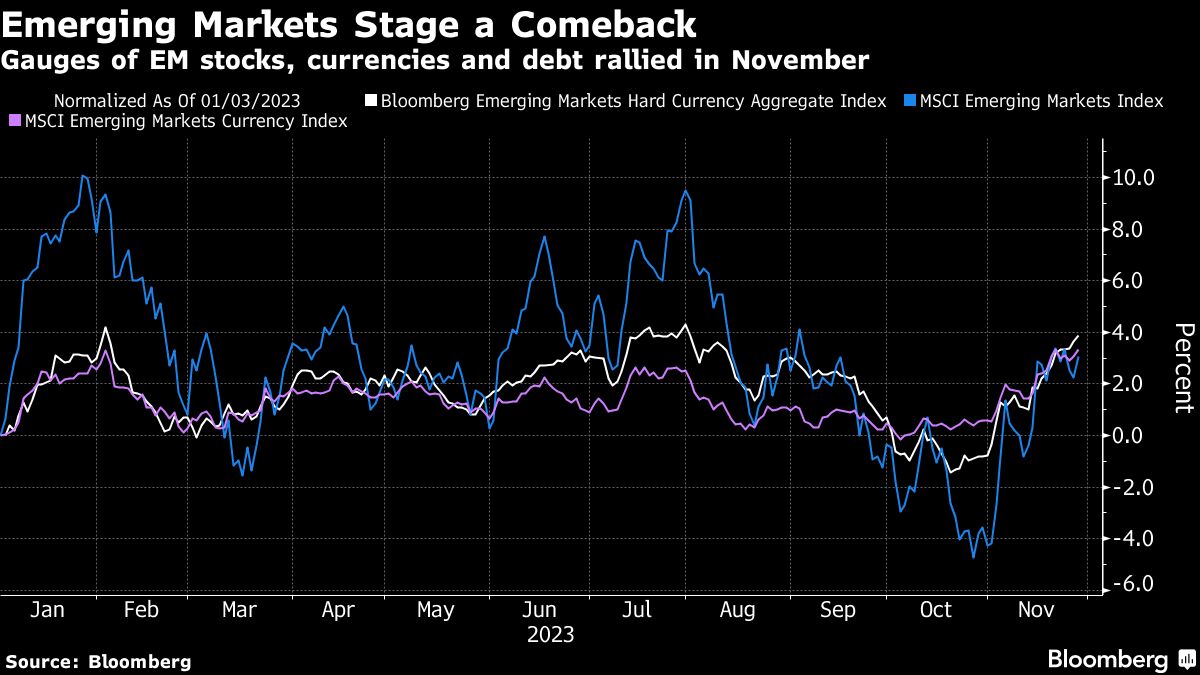

Euphoria is already spreading through developing-nation assets, spurring a 7.9% rally in stocks and a 6.7% run-up in sovereign bonds last month. Investors are also pouring cash into the world’s largest exchange-traded fund tracking emerging debt — a signal that mom-and-pop retail traders and sophisticated risk-takers alike are once again taking on the risky asset class.

“I’m very fundamentally positive,” said Pramol Dhawan, Pacific Investment Management Co.’s head of emerging-market debt. “EM is an under-owned asset class, but when you look under the hood and you dig a little bit deeper, then this is an asset class you should want to own.”

Pimco was among a large cohort of asset managers on Wall Street a year ago that expected the asset class to outperform in 2023 as major central banks pivoted and China’s economy reopened.

But, at times, the bulls were blindsided as Beijing struggled to stoke growth and 10-year US yields briefly topped 5% thanks to resilient economic data and a still-hawkish Fed. Emerging assets have swung dramatically in 2023.

“We came into 2023 thinking that this was gonna be the year for fixed income, and it clearly has not been what we expected,” said Gorky Urquieta, co-head of the emerging markets debt team at Neuberger Berman. “But 2024 looks like it will be.”

Now, as the new year approaches, Wall Street is renewing its optimistic chorus. Goldman Sachs and Morgan Stanley are both calling for double-digit returns for developing-nation sovereign dollar bonds in 2024. Pimco, whose emerging-market local currency and bond fund has outperformed 95% of peers in the past year, still favors domestic debt.

But even as the stars seem to align for the bull case, some investors remain unconvinced that emerging markets will rally from current levels.

Uncertainty lingers around China’s growth outlook — though President Xi Jinping is attempting to send a pro-business message before the country’s 2024 growth target is likely decided at the upcoming Central Economic Work Conference.

Swings in the US Treasury market over the past two months have also stoked some skepticism as traders try to gauge the Fed’s path ahead. While traders price in a chance of interest-rate cuts in 2024, Chair Jerome Powell has maintained a more cautious tone.

“Investors should take caution,” said Sylvia Jablonski, chief investment officer of Defiance ETFs. With US rates still far from stable, the next few months will prove crucial as the Fed solidifies its policy stance, she said. “We must see how this narrative plays out.”

To Brad Gibson, co-head of Asia-Pacific fixed income at AllianceBernstein in Melbourne, it comes down to math. At times when an investor could collect a yield of about 5% by owning a US two-year bond, “why would you buy Indonesia? Why would you buy anything else?”

Bright Spots

The bulls, however, say there’s money to be made in emerging markets — as long as they play it right.

Neuberger Berman’s Urquieta said he favors high-yielding bonds where markets are overly pessimistic on the risk of default and restructuring. He’s long on Argentine debt, and touted value in BB-rated sovereign notes.

The high-yield segment is also enticing Claudia Calich, the head of emerging-market debt at M&G Investments in London. The opportunity is worth taking on risks associated with exposure in El Salvador, Sri Lanka, Pakistan and Ukraine, she said.

“You start putting together a lot of those names, and suddenly, it gives you an opportunity set,” Calich said. “High-yield names are much more subject to idiosyncratic events, which can provide upside surprises — like Turkey post-election, Ecuador and Argentina elections and the recent removal of sanctions on Venezuela secondary market trading.”

Calich holds notes from Venezuela and its state-owned oil company PDVSA, Ukraine and Ecuador. She also has a small overweight in Argentine notes.

Morgan Stanley strategists favor dollar-denominated high-yield government bonds next year from eight countries ranging from Colombia to Egypt, as well as corporate debt from Mexican oil company Petroleos Mexicanos. Goldman Sachs pointed to BB-rated credits, and said Pakistan and Ecuador offer value among riskier sovereign borrowers.

In addition to remaining bullish on local-currency debt, Pimco is eyeing nearshoring trends, which it says support assets from Hungary, Czech Republic, Poland and Mexico.

“The nearshoring trends are very supportive for emerging markets,” Pimco’s Dhawan said. “We continue to be bullish. In fact, even more bullish now that where we’re at an inflection point” where rates are coming down and continue to support risk assets, he said.

What to Watch

- In Brazil, third-quarter GDP data may show a slight decline. In Argentina, markets will continue to monitor any new announcements by President-elect Javier Milei in the lead up to his Dec. 10 inauguration.

- The Reserve Bank of India is set to deliver a dovish hold at December’s meeting, keeping the repo rate at 6.50% for a fifth straight review, according to Bloomberg Economics.

- In other parts of Asia, CPI reports will come from South Korea, the Philippines and Thailand.

- Data out of Turkey showed inflation accelerating to 62% through November, the highest level this year. The central bank says price growth could peak at 75% in May before falling to 36% by end-2024.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Carolina Wilson