Now that inflation is finally decelerating, regulators are increasingly turning their focus to financial stability. They’re pushing for greater oversight of the financial system — not just banks, but also how they facilitate the ballooning shadow-banking system, led by hedge funds. With a tsunami of government debt to finance in upcoming years and the era of nearly cost-free and unlimited leverage ending, anything that restricts the market’s room for maneuver may have unintended consequences.

A worrying succession of mini quakes — including the March 2020 dash-for-cash that saw the Federal Reserve intervene and last year’s UK pension fund crisis that required emergency Bank of England gilt purchases — has made market overseers nervous about systemic risks. New rules coming into force in the coming years will change how financial markets operate. The hedge fund community is a keystone of the debt markets; disrupting its ability to absorb government debt will have knock-on effects for borrowing costs.

From July 2025, Basel III "end-game" rules take effect for larger US banks, catching up to what is already falling into place across Europe. Significantly, the change restricts the use of standardized models on the volume and complexity of risk-weighted assets. The Bank of England and European Central Bank have already put in place stricter controls; the BOE has even included selected hedge funds in its system-wide stress testing.

In short, a crackdown’s happening — so banks will find it more expensive to provide liquidity to customers. Each leg of any Treasury bond trade, which banks currently allow their clients to leverage for free, will incur additional costs after the rules change. This may alter behavior profoundly as marginal trades, especially in large quantity, become uneconomic. From early 2025, the Securities and Exchange Commission is proposing mandatory clearing of US Treasuries and repurchase agreements through the Depository Trust & Clearing Corporation. The clearinghouses only see the cumulative net exposure of each clearing member, not the exposure of individual customers. That’s a system flaw that various authorities are investigating.

And from the end of May 2024, the US and Canadian financial markets will settle equity and bond trades on a T+1 cycle, rather than taking two days to reconcile delivery of a security versus payment. This shortens the time available to resolve the small amount of "fails" that still add up to many billions of dollars of unreconciled transactions, which in turn may heighten concern over concentration of trades.

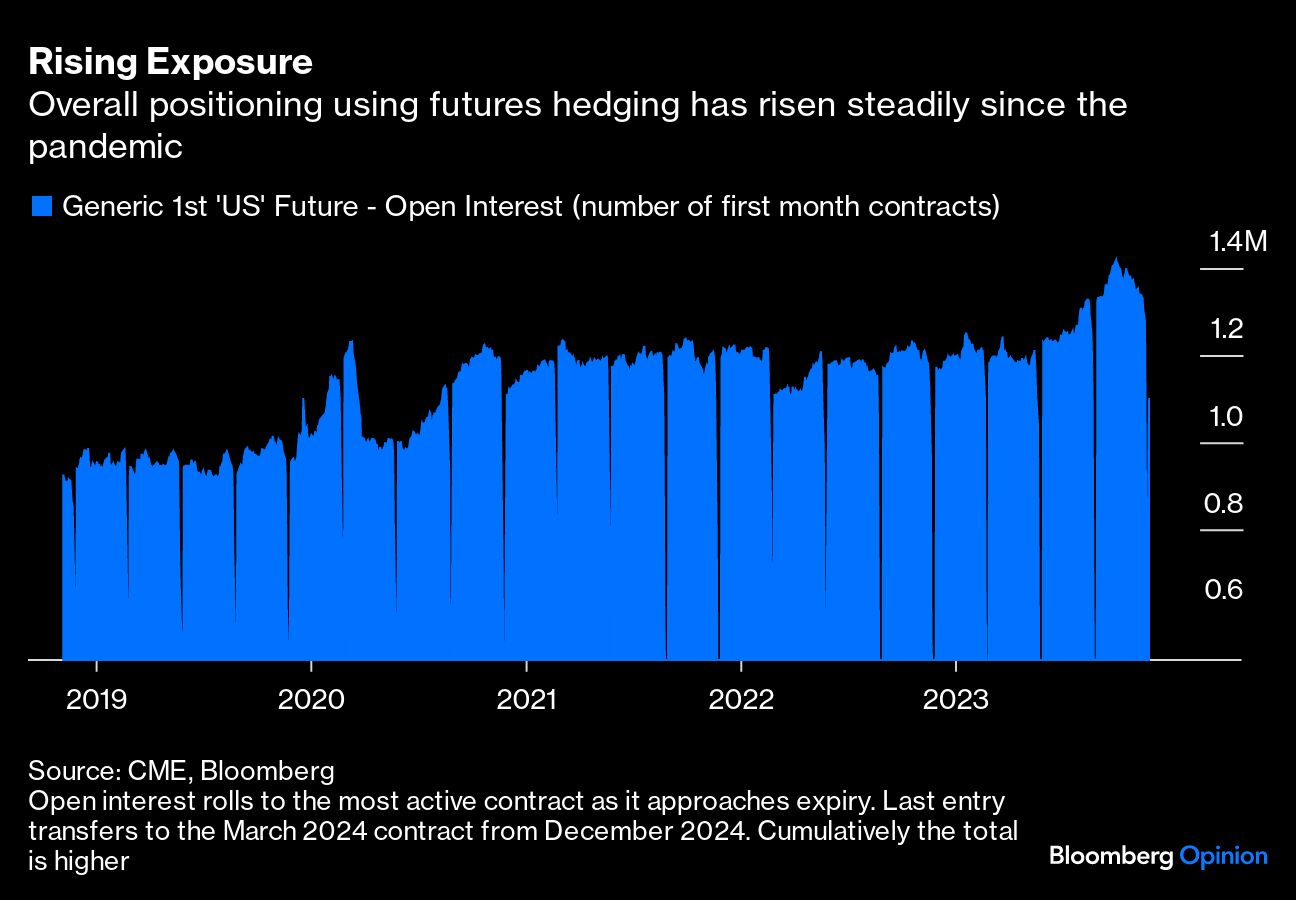

The so-called US Treasury basis trade has grabbed the most attention, as it's by far the biggest of many similar arbitrage plays. It’s where an eligible government bond is matched against an equivalent short position in the relevant futures contract, with the long and short netting off when the futures expire. But the secret sauce is in the financing, or implied repo rate, of the bond. Banks are happy to let hedge funds leverage the trade many times over at zero cost; the new rules will end this free ride.