Private Equity's Bubble Vintage May Fizzle

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsPrivate equity firms that spent hundreds of billions of dollars on acquisitions at the top of the market risk a nasty hangover.

A combination of higher interest rates and lower valuations could lead to disappointing returns for deals struck in the frothy mid-2020 to early 2022 period, after which borrowing costs rose sharply. In industry parlance, it’s shaping up to be a disappointing “vintage.”

While another bull market or interest-rate cuts could spare PE firms’ blushes, the onus is on them to deliver operational improvements rather than relying on rising valuations to generate profit for their investors. They won’t all pass the test.

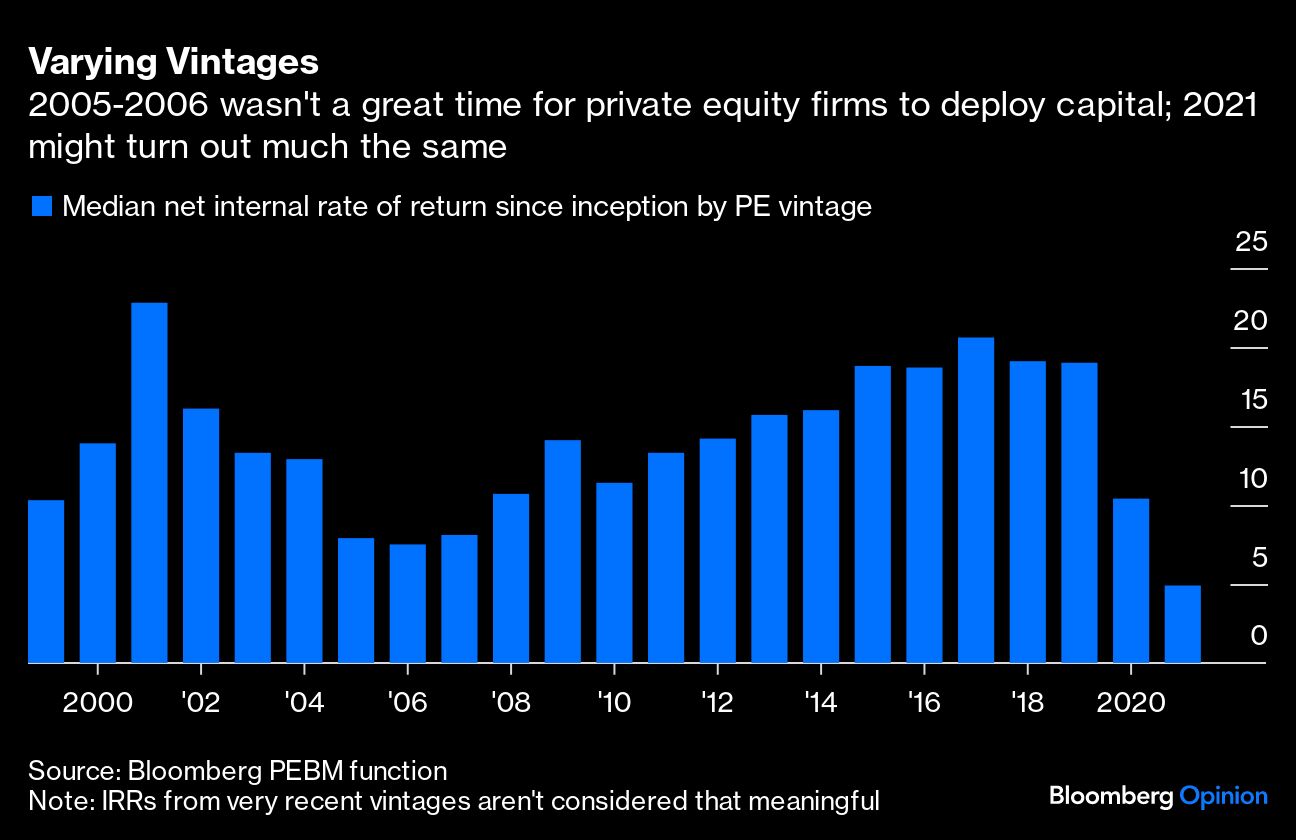

Investors need to pay attention not just to what sponsors buy but when they put money to work. Some of the industry’s best returns came during or following recessions, as starting valuations were lower and there was less competition to acquire assets.

By contrast, returns from deals immediately preceding the 2008 economic crisis were relatively poor because purchase prices were stretched and holding periods increased. (This variation is why private equity investors are well advised to diversify across vintages.)

PE funds often generate low or negative returns early in their roughly 10-year lifespan, so one shouldn’t read too much into the 2021 vintage’s current lackluster performance — the internal rate of return is just 4.9%, according to data compiled by Bloomberg.

Nevertheless, Bloomberg Intelligence analysts Paul Gulberg and Ethan Kaye predict PE returns will diverge by vintage with those that deployed capital just prior to 2022 potentially most challenged.

“This environment is a trickier one for some of the embedded equity that got put in the ground, particularly in private equity from call it 2019 to 2022, where prices were much higher, rates were much lower, and expectations for growth were there,” Kipp deVeer, Ares Capital Corp. chief executive officer, told analysts last month. “A lot of those things have changed, right?”

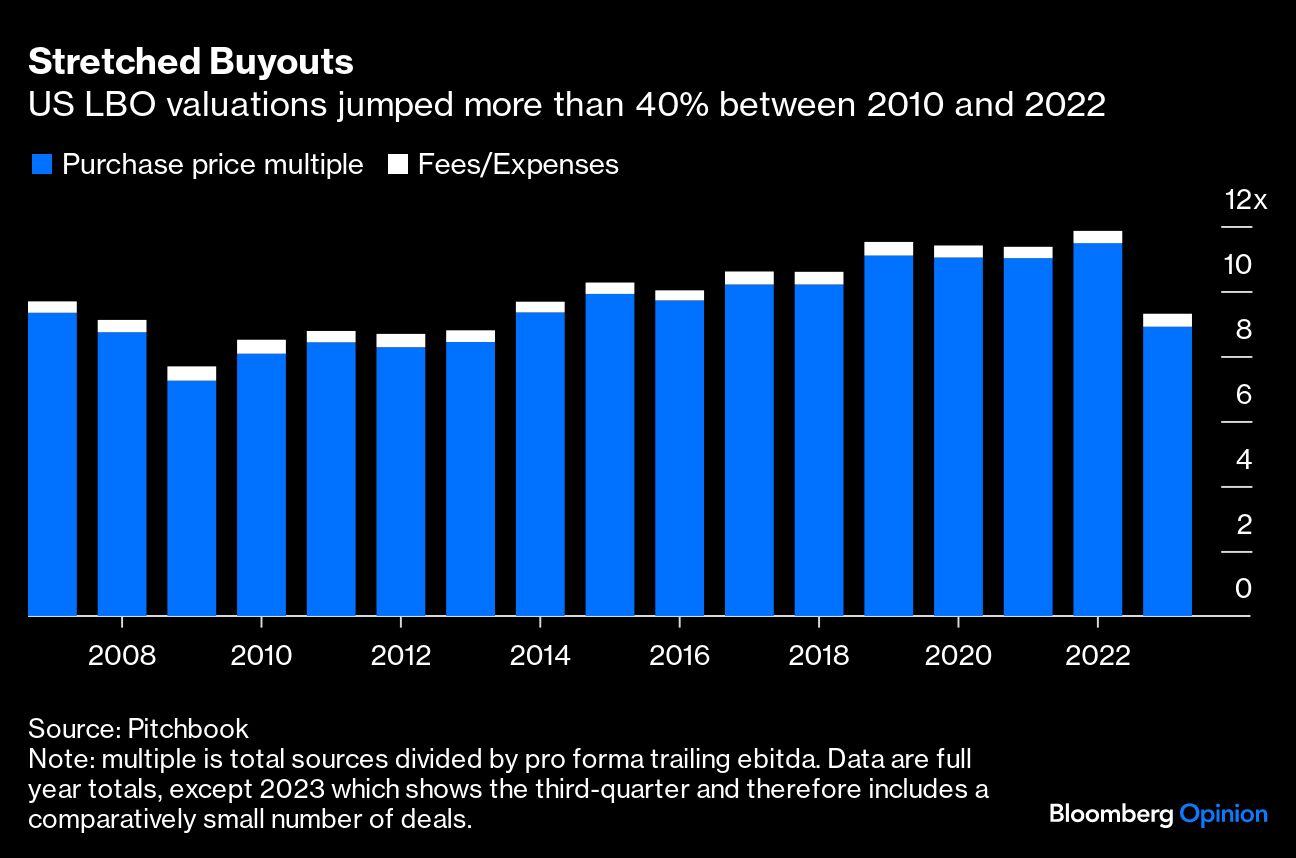

Right. Consider valuations: Average purchase prices — expressed as a multiple of earnings before interest, tax, depreciation and amortization — were about 40% higher in 2022 compared with 2010.

This was great for older PE vintages that exited investments at high prices but bodes ill for for new funds that were required to write larger equity checks. Around half of the value creation by PE firms since 2010 has come from higher earnings multiples, according to consultancy Bain & Co., so the recent contraction in valuations isn’t a good start.1

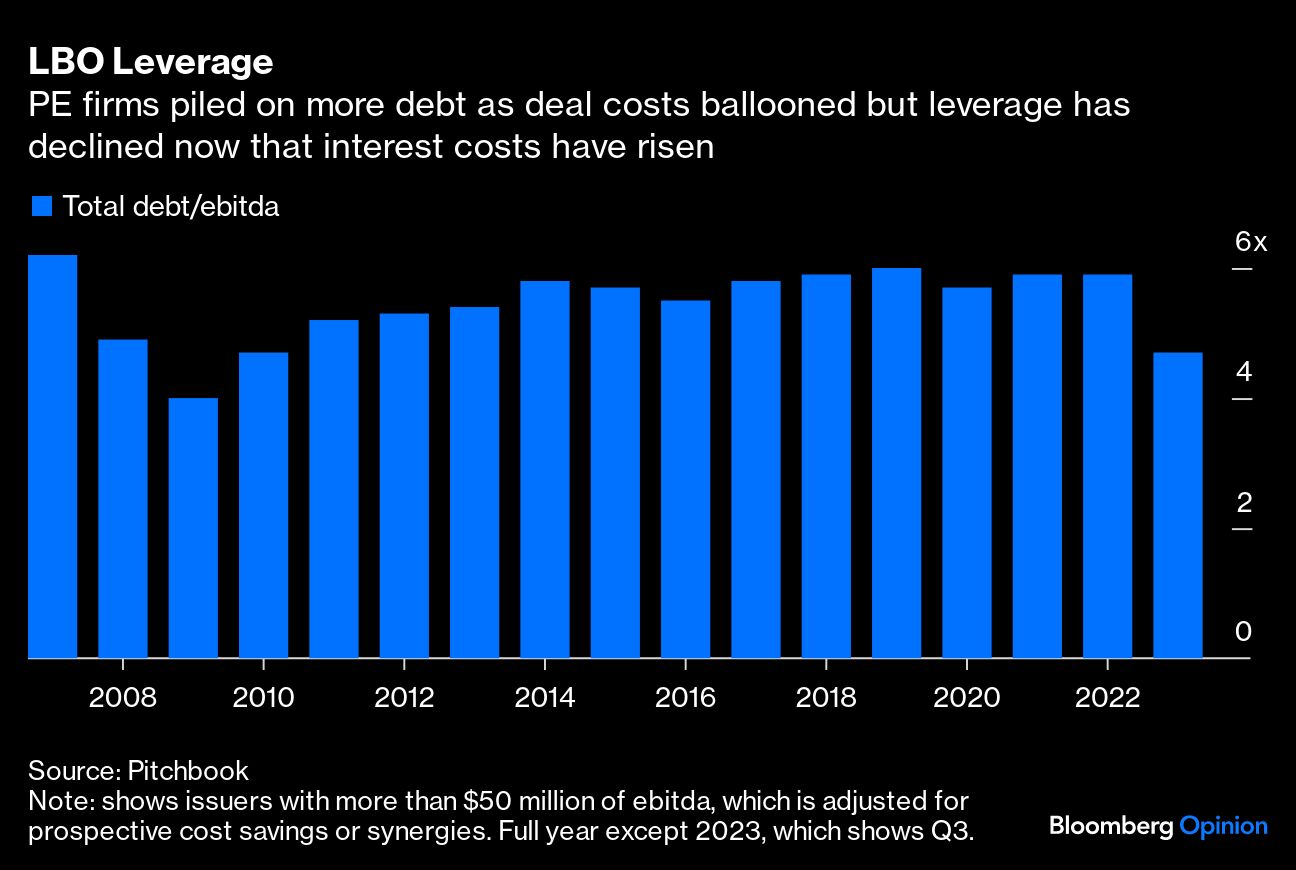

Plunging borrowing costs in 2021 triggered a surge in deal making, with sponsors increasingly turning to private credit to fund large transactions and using projections of recurring revenue rather than earnings (because targets had little or none of the latter). The cost of servicing floating-rate borrowing has since more than doubled, and most sponsors didn’t hedge this exposure.

It’s not the only way PE firms may have overestimated the ability of portfolio companies to support high debts: Flattering adjustments to earnings — so-called add-backs — also became much more prevalent in this period.2

Private credit loans originated in 2021 will likely perform worst, rating company Moody’s Corp. warned in June, noting these were underwritten “when there was rising optimism around operating performance and higher tolerance for weaker creditor protections, including covenants.”

Borrowings from this PE vintage generally don’t require refinancing yet, providing some breathing space. But if interest rates remain higher for longer and valuations stay compressed, PE owners may have to inject more equity, lowering their returns.

Typically, private equity funds spread their investments over four or five years, reducing the risk of buying only when prices are high. But some of that conservatism was jettisoned in 2021; for example, when software-focused PE firm Thoma Bravo LLC spent almost all the $23 billion it had raised from investors in just 14 months. The firm declined to comment, but its co-founder, Orlando Bravo, said at a Financial Times conference last month that “the time to buy the right company that fits your strategy is when you can.”

“When things are very frothy, when the markets are ripping, people tend to be pro cyclical and over-invest capital at the top of the market,” Joseph Bae, co-chief executive officer of KKR & Co., told investors last year, adding his firm was more measured in its approach.

Buyout volume in this period was dominated by a couple of sectors — technology and health care — whose revenue and pricing power were expected to remain “sticky” even if the economy slowed. (Companies are reluctant to switch software providers due to the costs and inconvenience, for instance).

However, cracks have started to emerge. US health care has been hit by a combination of wage inflation and insurer reimbursement difficulties, and several PE-owned companies have filed for bankruptcy this year, including KKR’s Envision Healthcare Corp. PE-backed software firms may be vulnerable if revenue doesn’t grow or they don’t control costs sufficiently. Fintech Finastra Group Holdings Ltd.’s $5.3 billion debt refinancing this summer was complicated by its stalling sales, forcing owner Vista Equity Partners LLC to inject an extra $1 billion.

Of course, it’s too soon to give up on PE’s bubble vintage. The stock market’s recent blistering rally and high valuations awarded to profitable tech companies are encouraging. In June, Thoma Bravo agreed to sell a financial software investment, Adenza Group Inc., to Nasdaq Inc. for $10.5 billion, roughly doubling its money in fewer than three years. (Nasdaq’s shares fell after the deal was announced due to concerns that the exchange overpaid.)

Plus, as Dan Aylott, head of European private investments at Cambridge Associates, told me, funds that still have dry powder “should be able to spend it now in a more favorable valuation environment.”

The current drought in PE exit sales shows sponsors aren’t yet ready to lower their price expectations or accept that rates will remain higher for longer. However, following a decade of stellar PE returns, investors should be prepared for a poor vintage.

1 Though in tech, earnings growth has been a bigger driver of value creation, notes Bain.

2 For mergers and leveraged buyouts in 2021 these adjustments – which include expected cost savings - accounted for nearly one third of projected ebitda, compared to almost one quarter in 2015, according to S&P Global Ratings.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All