Every year, millions of Americans send their hard-earned money to life insurance companies, in return for a promise that it will grow and provide them with regular income in old age. These fixed annuities make up a large part of the nation’s retirement savings — at last count, more than $3 trillion.

They could also become a nexus of the next financial crisis, if regulators don’t act to mitigate mounting risks.

The annuity business should be simple and boring. Invest in high-quality assets that will mature when the time comes to pay policy holders; take a small cut of the returns for your efforts. Thanks to penalties for early withdrawal, insurers shouldn’t have to worry about customers suddenly demanding their money back, as sometimes happens to banks. As long as the company’s owners provide enough equity to cover the occasional bad investment, everyone should be fine.

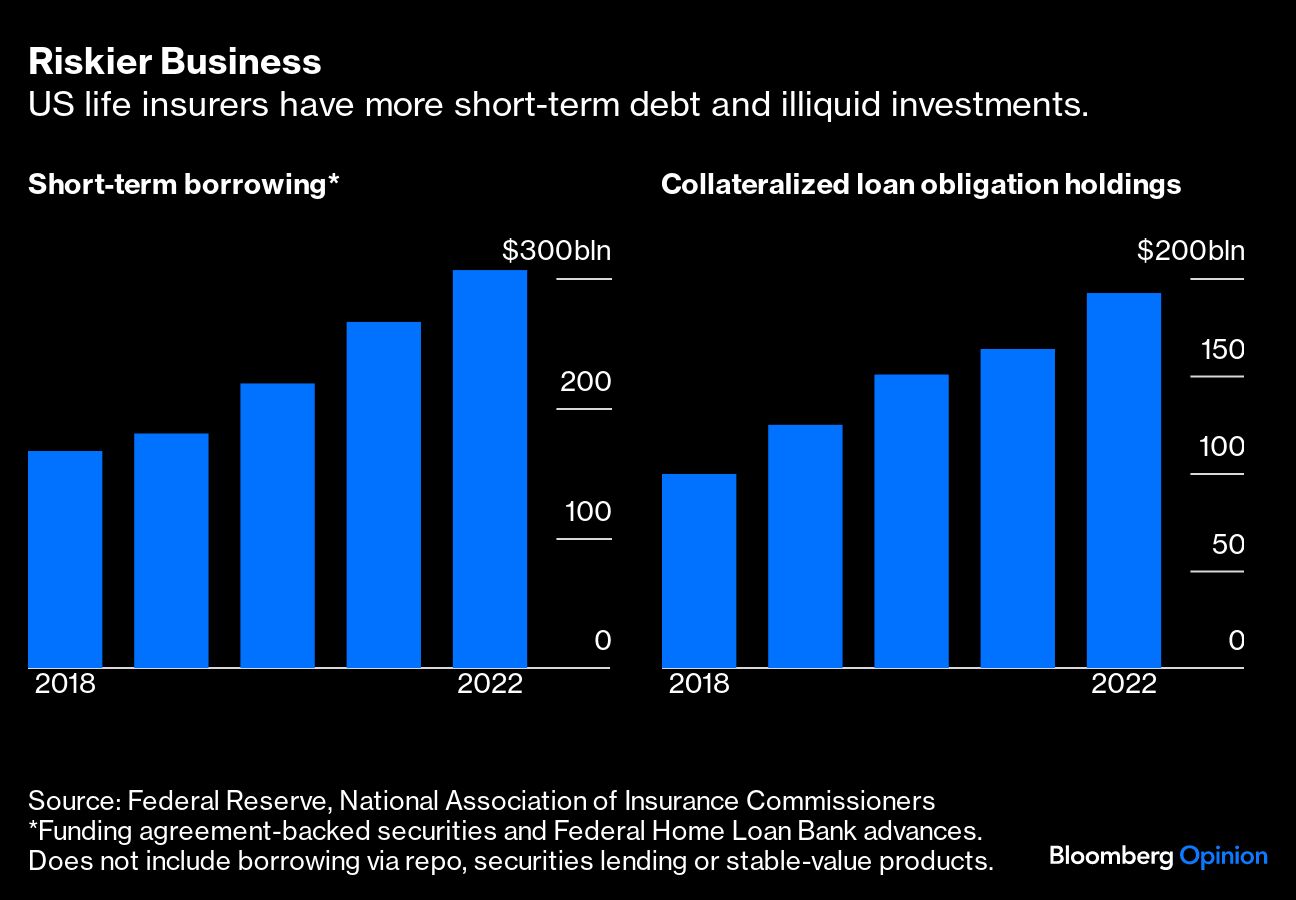

In recent years, though, insurers have made things more complicated. In pursuit of cheaper funding, they’ve turned to shorter-term borrowing — via wholesale credit markets and Federal Home Loan Banks. They’ve juiced returns in part by investing in collateralized loan obligations, which contain loans to highly indebted businesses. And they’ve channeled billions of dollars through affiliated reinsurers in Bermuda, where tax and other rules are less burdensome.

The transformation has coincided with a big shift in the industry’s ownership. Private investment firms have taken stakes in companies accounting for more than a tenth of all US life and annuity assets. In some cases they might be adding value, by identifying higher-yielding yet hard-to-sell assets — such as corporate vehicle fleets — that serve annuity holders’ interests. But research suggests they’re boosting returns primarily by increasing risks, and by circumventing taxes and capital requirements. Much of the industry — comprising about $2 trillion in annuity liabilities, including transferred corporate pension plans — has adopted similar strategies.

In effect, life insurers have become more like banks, but without their backstops and safeguards. Their funding has become less secure: Annuity holders can more easily afford withdrawal penalties when other investments are paying higher returns than before. And their assets are vulnerable to rising corporate bankruptcies. Although CLOs have historically performed well, certain tranches carry a greater risk of total loss than a diversified portfolio of corporate bonds. All this increases the chances that an economic downturn or distress at one insurer could trigger a rush to the exits.

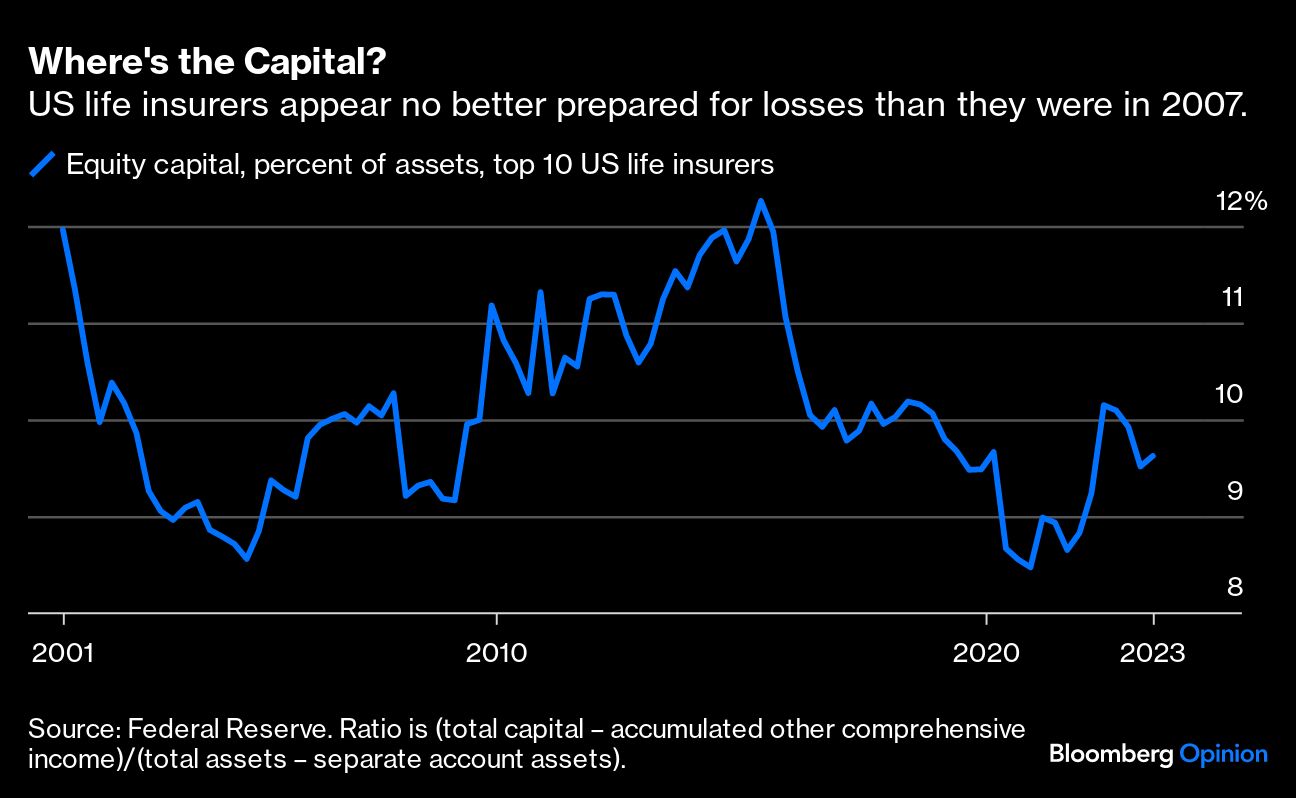

This worst-case scenario isn’t theoretical. Early annuity surrenders recently contributed to the failure of Italian insurer Eurovita. In 2008, wholesale creditors pulled funding from insurers such as AIG and The Hartford. Annuity providers with bank-like activities pay higher yields on short-term debt, suggesting markets view them as riskier. Overall, life insurers were holding about $115 billion in non-AAA-rated CLO tranches at the end of 2022. That’s significant, set against their loss-absorbing capital of less than $500 billion — which represents a smaller share of assets than just before the 2008 financial crisis.

Authorities are aware. The National Association of Insurance Commissioners has developed stress tests of US insurers’ liquidity and CLO holdings, and is working on stricter capital standards. But it’s only a coordinating body for the patchwork of state regulators actually responsible for supervision, which in turn have little insight into insurers’ wider operations. The US is lagging behind international efforts to develop more comprehensive and comparable measures of capital adequacy.

The Financial Stability Oversight Council needs to reassert the power granted under the Dodd-Frank Act to subject systemically important insurance groups to Federal Reserve oversight. The Fed should apply prudent capital and liquidity requirements to reduce the risk of runs. And regulators should insist that all covered insurers disclose the data required to assess their financial condition.

Some of the innovations in the annuity business might benefit consumers, making saving for retirement cheaper and more accessible — but this mustn’t come with an unacceptable risk of disaster, or of yet another taxpayer bailout. “Shadow banking” was deeply implicated in the last big financial crisis. Regulators need to heed that lesson.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by The Editors