Sergio Ermotti promised ruthlessness in reshaping Credit Suisse Group AG, and the chief executive officer of UBS Group AG has been true to his word.

His team cut costs and offloaded assets from its one-time rival faster than planned, as revealed in UBS’s in third-quarter results on Tuesday. Investors took this as a sign that UBS could restart stock buybacks sooner. The shares rose as much as 5% in early trade.

UBS acquired the failing Credit Suisse this summer in a shotgun marriage arranged by Swiss regulators. The earnings report showed signs of a surer footing for the combined wealth and banking businesses, but there was also evidence of decimation in Credit Suisse’s investment bank.

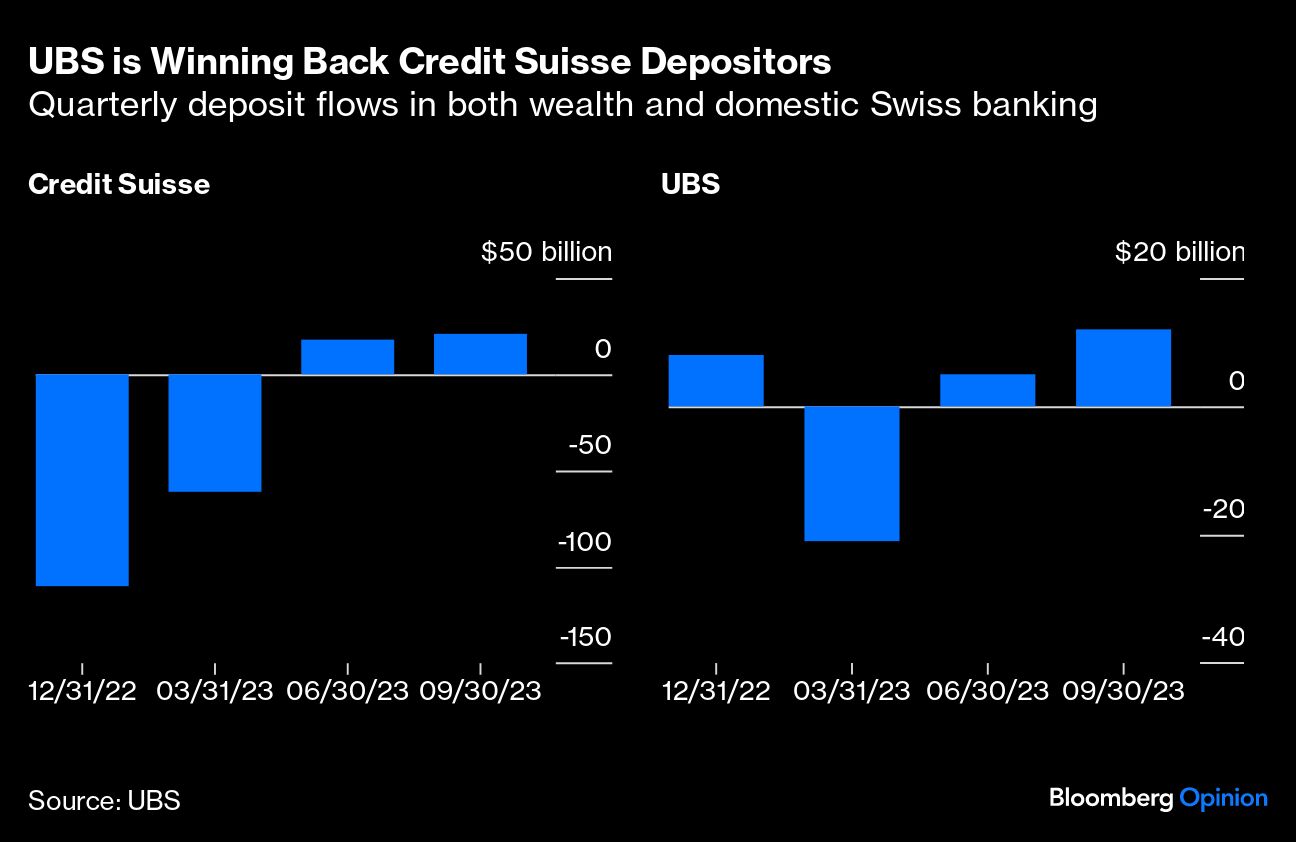

The big positive was that UBS has managed to sweet talk Credit Suisse customers into returning billions of deposits, especially in wealth management. In wealth and the domestic Swiss bank, it took in $33 billion, two-thirds of which was from Credit Suisse clients. That followed inflows of $23 billion in the second quarter, most of which was also from Credit Suisse clients. While healthy, that’s a long way from replacing the $171 billion in outflows that Credit Suisse suffered in the previous two quarters.

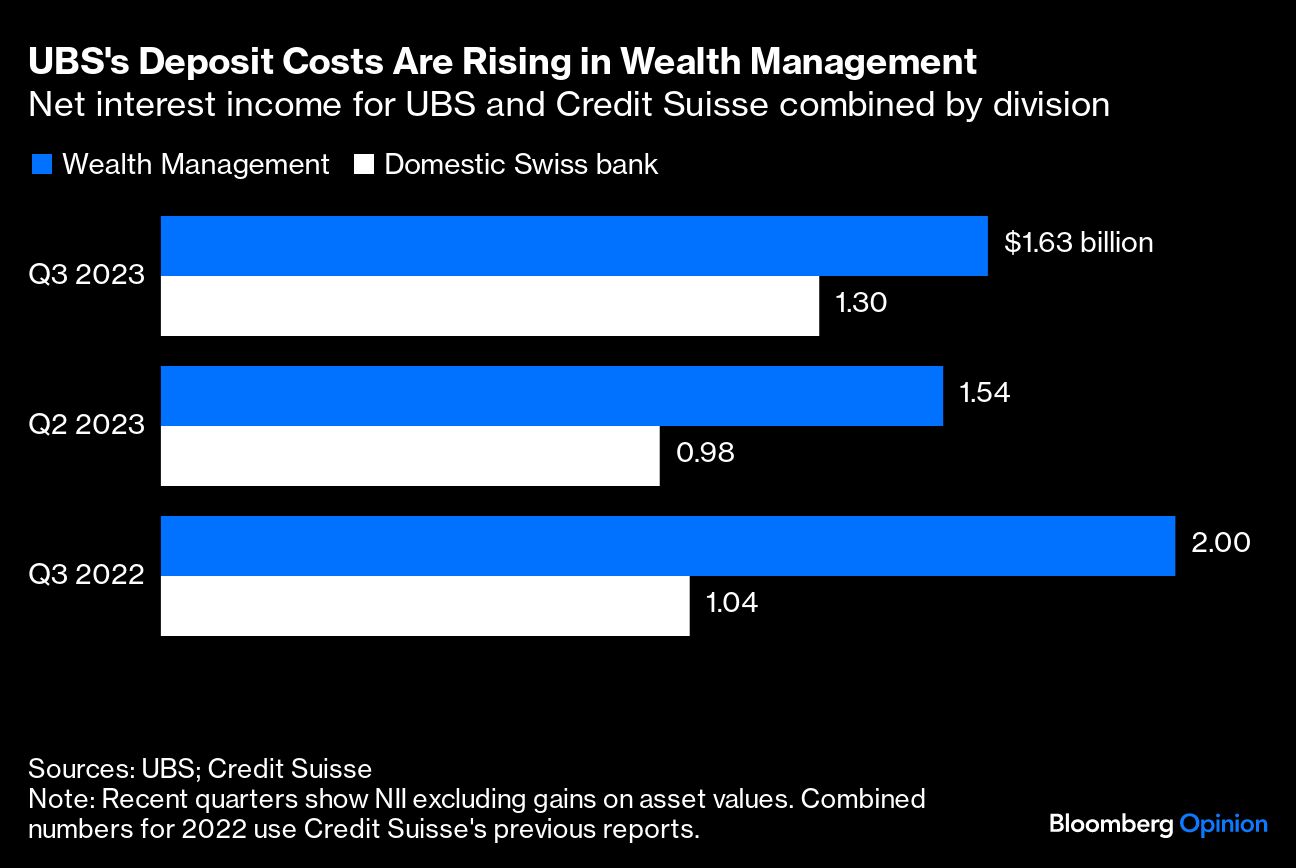

To some degree, UBS is paying up to attract money back, although the best rates are likely being offered to clients with lucrative trading, investing and borrowing accounts. Still, deposit costs are higher as many customers are moving cash to higher-yielding savings accounts, which has squeezed net interest income. The wealth unit’s NII was down 18% versus what both banks earned separately in the third quarter last year. Offsetting this, however, NII was up 24% in the domestic Swiss bank, which relies more on cheaper corporate deposits for funding.

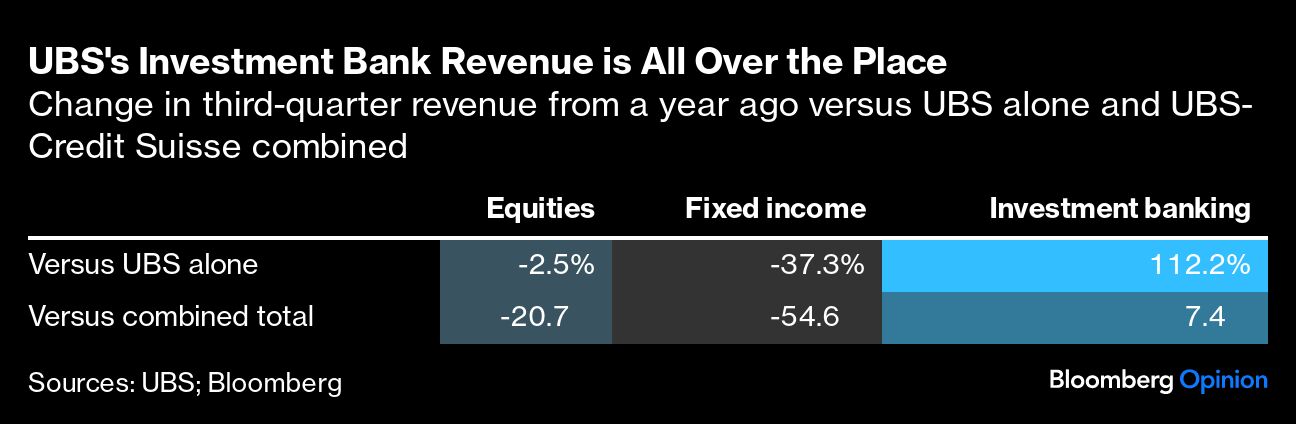

While these businesses look steadier, it is clear that Credit Suisse’s investment bank and markets arm has been put through the shredder. Chief Financial Officer Todd Tuckner compared the combined units’ results with UBS’s standalone investment bank from prior periods because so much of Credit Suisse is being discarded.

The dealmaking and capital-raising business performed very well on this basis with revenue more than double the same period last year. That was down to UBS winning some big deals in leveraged finance and had little to do with Credit Suisse bankers, but UBS expects the teams who haven’t been jettisoned to contribute more in future.

In markets, UBS underperformed. In equities and fixed-income trading, the combined banks produced lower revenue than UBS alone did in the third quarter last year. And when compared to what UBS and Credit Suisse produced separately a year ago, revenue was down 21% in equities and 55% in fixed income.

UBS allowed its investment-banking leaders to cherry pick the people and businesses they wanted from Credit Suisse and then send the rest into a bad bank to be wound down over time. They have been sharp and clear about it, and plenty of Credit Suisse people jumped before they were pushed, which is why the restructuring is going quicker than expected so far. The investment bank will be in the shape UBS wants by the end of the year, but how its likely revenue base will look in future is a big unanswered question.

The rest of the cost cuts to come from wealth management and the domestic bank will be slower to achieve because these are more traditional mergers – and within Switzerland fraught with political sensitivities over jobs.

UBS has a bit of a tightrope walk to perform in getting this right, according to Filippo Alloatti, head of financials credit at Federated Hermes Ltd., but it does have a good track record in cost cutting. The more difficult challenge for UBS will be in telling a good and credible story on revenue growth when UBS sets out a three-year strategic plan at its full-year results next February, Alloatti said.

The bottom line is that UBS has made a strong start on a long and difficult job, but there are still a lot of details to be nailed down. Investors might be getting a bit ahead of themselves in their stock buyback hopes, but so far, so good.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul Davies