The US economy is being kept afloat with lawnmowers, cars and vacations. US consumers have kept buying these things despite high inflation and the contractionary policy of the Federal Reserve, and they deserve thanks not only for the recession that still has not come but for the fast pace of recent economic growth.

And yet, the economy doesn’t feel sustainable. Consumers have to cut back eventually, right? And when they do, does that mean a recession?

Part of the answer can be found in Americans’ bank accounts. A few years ago, they were flush with pandemic checks, but their owners had nowhere to spend their money. Now question of how much savings Americans have is as contested as the race for speaker of the House (and it has lasted much longer). There are conflicting reports about whether the excess savings have run out, even though spending is still strong. No one is sure what is going on.

A more detailed answer to these questions comes from the Fed, which released its tri-annual Survey of Consumer Finances last week. The short version: Things have been worse. While many consumers are wealthier, many others are spending on borrowed time. Some people still have lots of cash, and others are in a precarious spot.

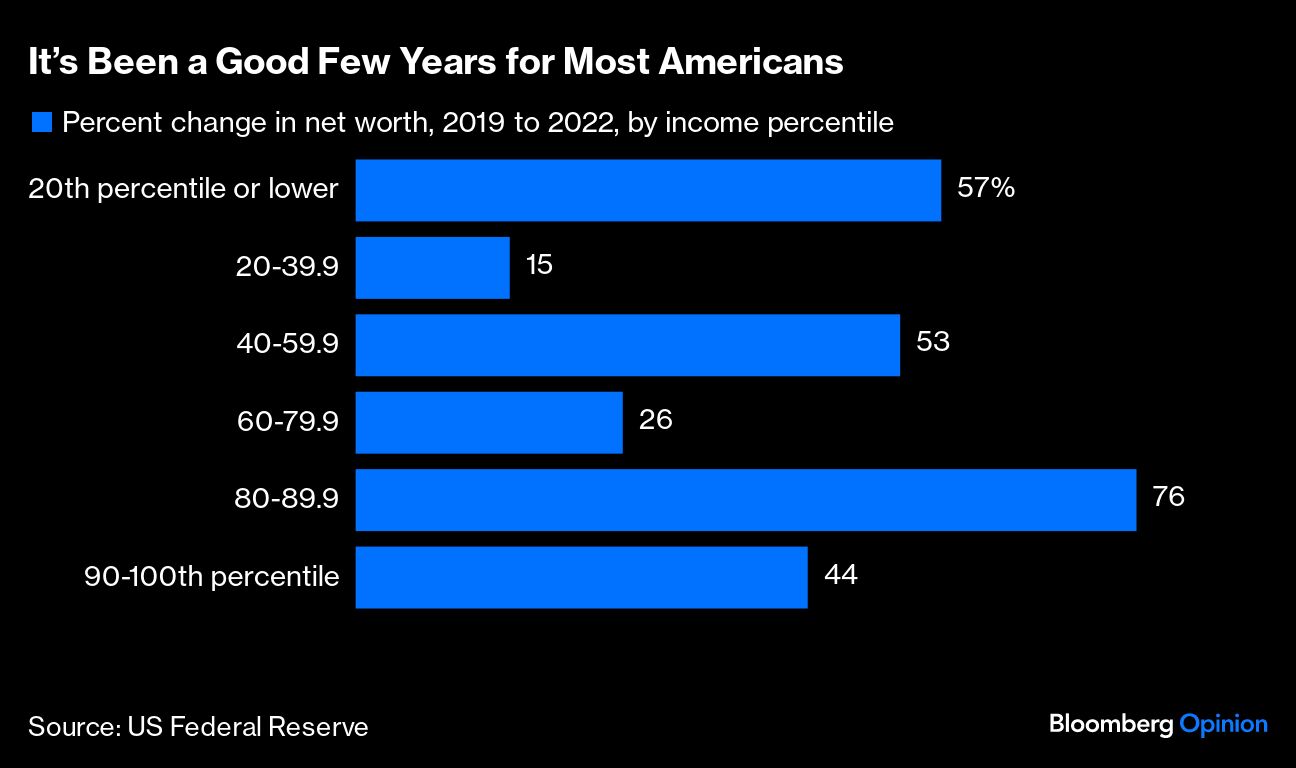

The survey offers the most complete picture so far of what happened to US households from 2019 to 2022. One thing it shows is a sizable uptick in net worth among all income groups.

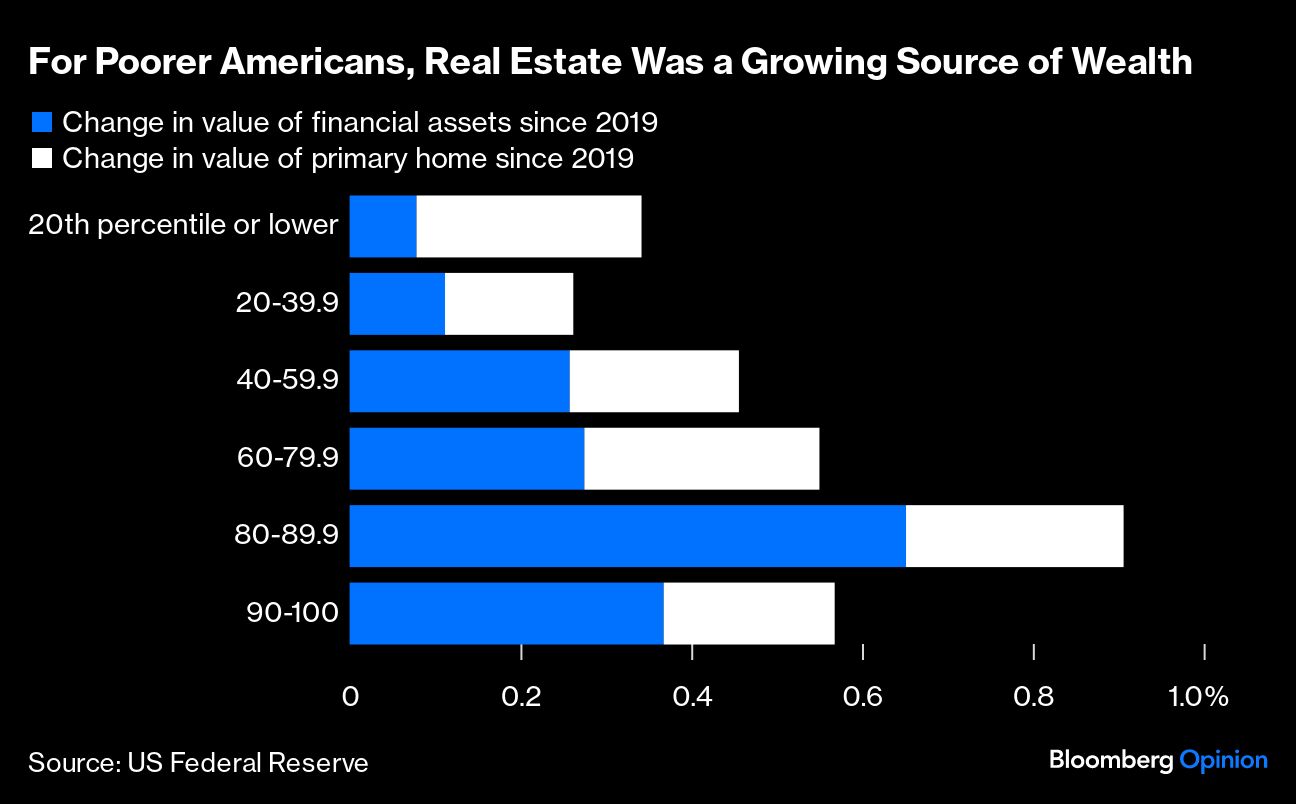

Lots of this new wealth came from increases in the value of a household’s most illiquid asset — its home. Lower-income homeowners especially can thank the appreciation of real estate values for their increased wealth.

The value of consumers’ financial assets did increase, but for the bottom 50%, the increase was not nearly as large. Among the bottom 20%, median financial assets increased from $1,300 to $1,400, not enough to make a big difference in spending. These consumers are also more likely to keep their assets in cash, which was further eroded by inflation in the last year. Median financial assets for the top 10%, meanwhile, increased from $927,000 to $1.27 million.

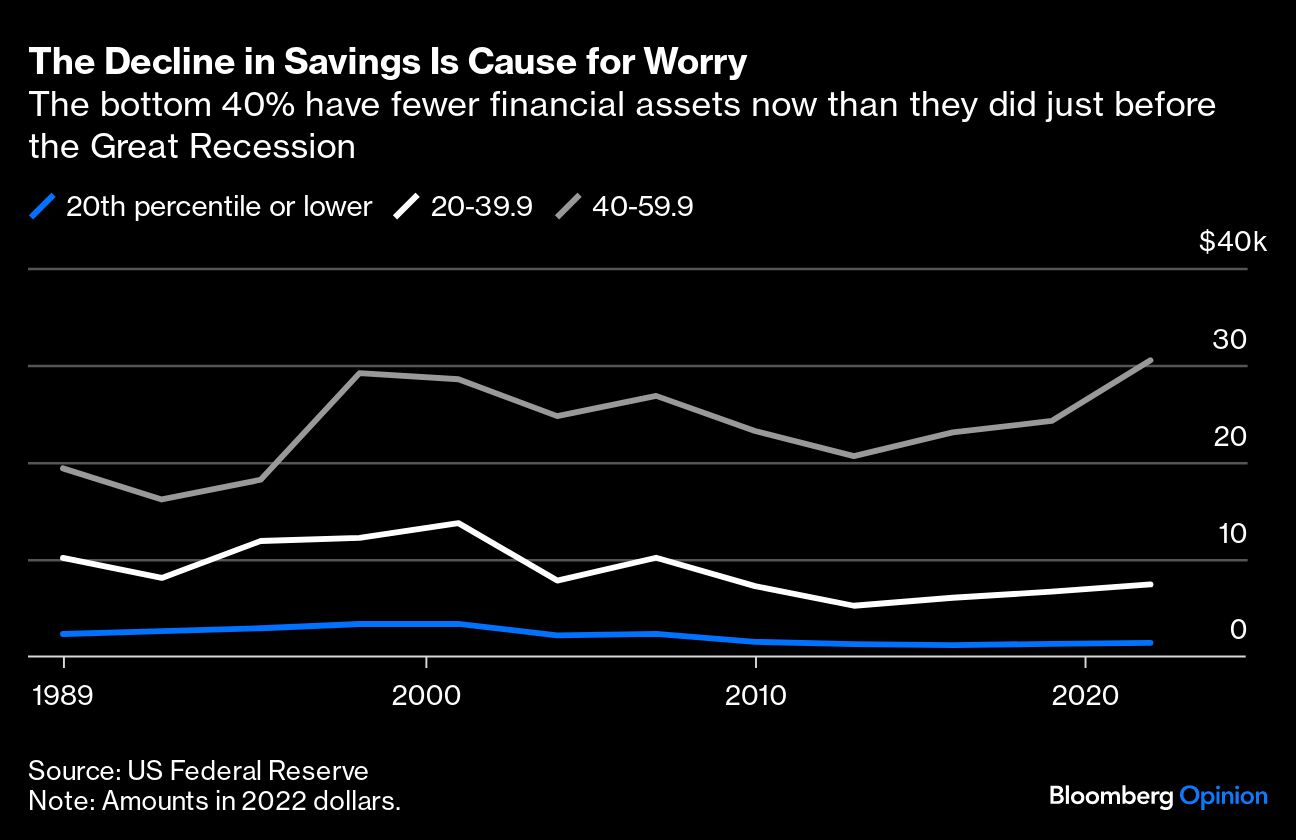

It is also worth noting while financial asset values have risen for every income group since 2019, at least when it comes to savings, those in the bottom 40% are much worse off now than they were on the eve of the financial crisis. Financial assets are 40% lower than they were in 2007 for the bottom 20% (though they do have slightly less debt).

One potential bright spot: Low mortgage rates helped increase homeownership for lower-income consumers. Homeownership rates went from 26.5% to 31% between 2019 and 2022 among the bottom 20% of earners under age 65. And unlike in 2007, many of them have fixed-rate mortgages.

The data show that the top 50% benefited from soaring house and asset prices in the last four years, and are in good financial shape. The bottom 50% did a bit better at first, but still don’t have much liquidity and inflation has eroded their savings. This may explain why credit card debt has been rising along with higher spending.

This points to a serious and growing vulnerability in the US economy. Even if there is a recession, the top half of Americans will probably be fine. Their spending will decline, but it is unlikely to plummet unless there is a huge drop in asset values. People in the bottom half of the economy, by contrast, do not have much in savings, and they could be in trouble if the job market cools off and inflation continues to be high.

All this said, odds are that things will not get as bad as they were in 2008 when many people had mortgages they could not afford, and overleveraged consumers caused a housing bust that decimated household wealth. Now many homeowners have cheap, fixed-rate mortgages — which have only gotten cheaper with inflation. They are less likely to sell, at least not all at once, and crash the housing market.

A recession could still happen, of course. An environment of rising interest rates, after decades of low rates, creates a lot of vulnerabilities in the economy, and a weakening consumer sector will make it worse. American consumers may not be able to prevent a recession, but they won’t cause one, either.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.