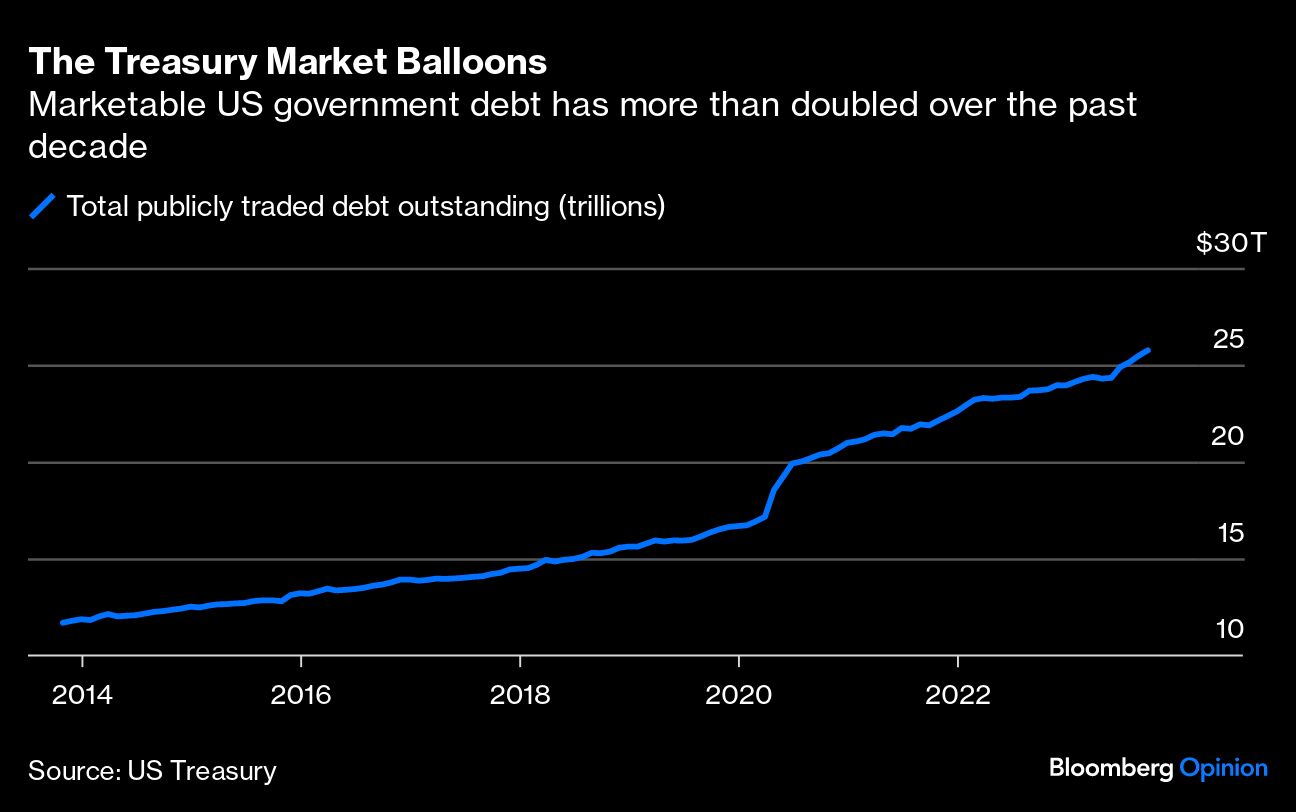

The $25.8 trillion market for US Treasury debt is like the circulatory system for the world’s financial markets — everything else relies on it. In recent years blockages have occasionally formed, and central banks have had to step in to restore the money flow. Now, as Treasury prices adjust to a surge in federal borrowing and a changing outlook for long-term interest rates, it’s essential that policymakers keep the market healthy.

The diagnosis is relatively simple. For decades the market has depended on a group of so-called primary dealers (today there are 24) to maintain order during times of stress. But the size of the market has exploded in the past decade, at the same time as new rules have set limits on banks’ leverage, curbing their capacity to take on assets. Meanwhile, as primary dealers’ holdings have shrunk, principal trading firms, hedge funds and other nonbanks have stepped in to play a bigger role.

Unlike the primary dealers, these firms and funds have no obligation to help make markets and their activities are less visible to regulators. That leaves policymakers scrambling for emergency solutions — as when a shock from the Covid-19 pandemic drove investors, including highly leveraged hedge funds, to sell Treasuries in a “dash for cash” in 2020. Regulators are considering ways to discourage such risks from building, including pressing banks to gather data and curb lending to hedge funds.

Sustainable cures are overdue. Policymakers should act on four fronts to help keep the market functioning smoothly.

As a start, the Securities and Exchange Commission should focus on central clearing for Treasuries. By acting as a trusted middleman, clearinghouses mitigate the risk of counterparties failing to make good on trades. Yet less than a quarter of Treasury trades are centrally cleared, compared with nearly all trades in markets such as exchange-traded derivatives and equities.

A proposal that would require more of those trades to be cleared makes sense. Before moving ahead, the SEC should ensure that the Fixed Income Clearing Corp. — currently the only company registered to clear US Treasuries — is prepared to handle trading and collateral from all eligible participants. It also needs to be alert to systemic risks that the industry may pose.

Next, regulators should open the market to more participants. Currently, most trades take place among dealers or between dealers and their customers. Enhancing the ability of customers to trade directly with each other, known as “all-to-all” trading, should make it easier to find counterparties during times of stress. Previous efforts to encourage such trading have faltered, but more central clearing might make it easier to build the trust necessary to widen the pool.

For their part, central banks should make it possible for nonbanks to post Treasuries in return for short-term loans. The Bank of England is already studying making loans available to a wider variety of market participants in exchange for gilts during periods of exceptional market disruption. The Fed could do the same with its standing repo facility.

Finally, the Financial Stability Oversight Council, created after the 2008 financial crisis, should consider designating some key institutions as systemically important, putting them under enhanced supervision. That will give regulators more insight about where leverage is building in the system, and more power to impose guardrails.

The Treasuries market is too important to be allowed to clot or seize up. Regulators have studied the market and its vulnerabilities long enough. Now they should do what’s needed to keep it boring.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by The Editors