The rout in 10-year Treasury notes has pushed yields to the highest since 2007, with the latest bump above 4.89% coming on the heels of a strong US jobs report on Friday. What everyone wants to know now is how much further the selloff will go and how long it will last. I can venture a few educated guesses based on history.

Looking at past periods of monetary policy tightening, my main observation is that the 10-year yield tends to max out at — or slightly above — the Federal Reserve’s peak policy rate. This stands to reason because investors traditionally demand a premium for the inherent uncertainty associated with holding longer-term bonds.

Moreover, longer-term yields — which influence debt like auto loans and residential mortgages — are a key part of the monetary policy transmission puzzle, so the Fed may not see its work as done until they fall into line. Longer-term yields may move higher in anticipation of the Fed’s target rate or they may follow, as is the case this time. But one way or another, history shows that the 10-year yield needs to climb high enough to kiss the Fed’s peak rate before both can start moving in the other direction.

- In 1994-1995, the 10-year peaked at 8.03%; the upper bound of the fed funds target peaked at 6% about two months later.

- In 2000, the 10-year peaked at 6.79%; the fed funds peaked at 6.5% about three months later.

- In 2006-2007, the 10-year had a double peak at around 5.29% over about 12 months that coincided almost perfectly with the peak in fed funds at about 5.25%.

- In 2018, the 10-year peaked at 3.24% before fed funds peaked at 2.5% about a month later.

From this (admittedly limited) sample, we can surmise that the “normal” move is for the 10-year yield to reach or exceed the peak in the fed funds rate, which currently stands at a range of 5.25% to 5.5% and is projected by the median Fed forecast to peak 25 basis points higher later this year. Taken at face value, those two pieces of information suggest that 10-year yields could plausibly go an entire percentage point higher (or more, in the 1995 scenario).

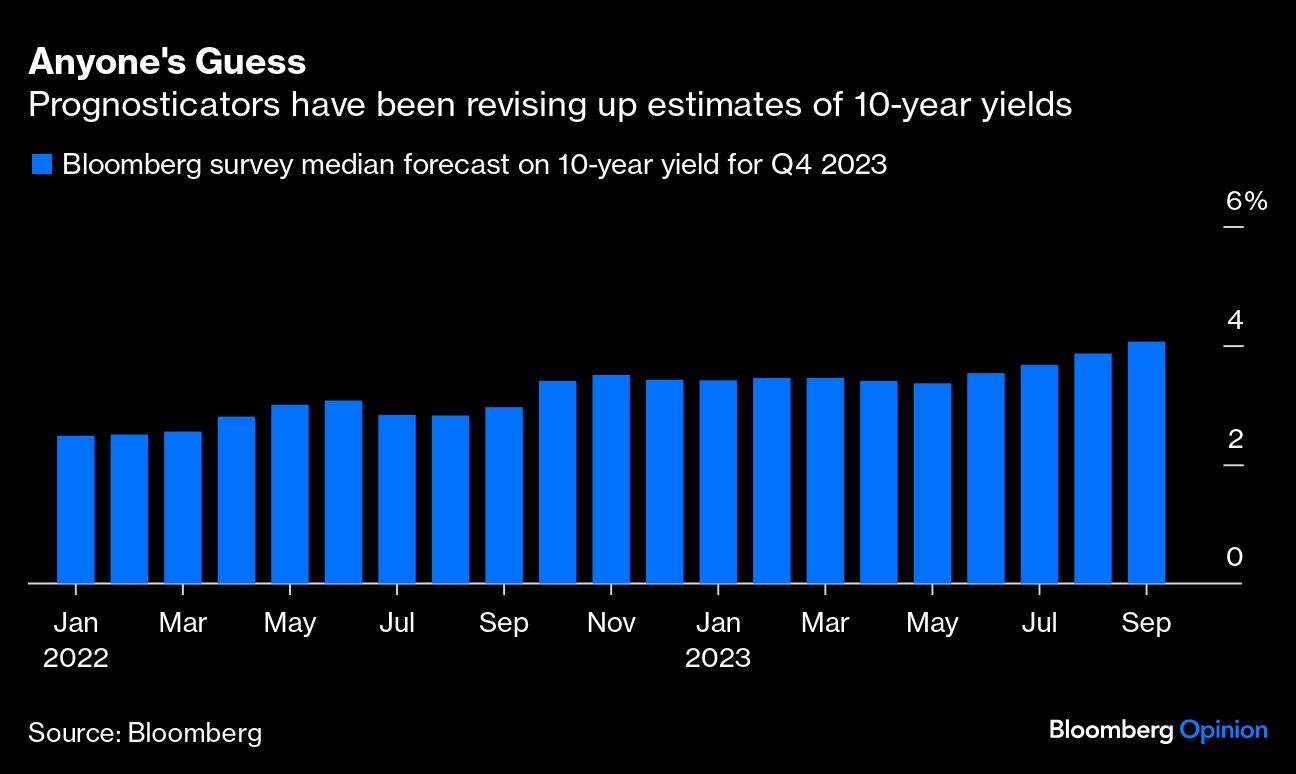

Granted, few investors even seriously considered that possible until very recently, myself included. As of June 2023, the median prognosticator surveyed by Bloomberg thought that the 10-year yield would end 2023 at 3.53%. And even today — in the throes of the rout — the consensus suggests that the yield will fall back to 4.06% by the end of the year. It’s worth considering why everyone was so convinced a few months ago — and many still are today — that “this time is different.”

The obvious explanation, of course, is that the market has been bracing for a sharp change in macroeconomic conditions. Famously, the yield curve inverts in anticipation of a recession because investors expect that the downturn will force central bankers to cut rates in the future. It can also invert because investors think that inflation is transitory and that interest rates will ultimately return to their secular downward trend. In 2022, a majority of market participants seemed to hold one of those two views — so longer-run rates stayed unusually low relative to the monetary policy backdrop.

The past several months have severely dinged the popularity of those outlooks, however. Recession forecasts fell out of vogue as the US consumer kept spending — although they may be making a comeback, curiously, because of longer-run rates themselves. At the same time, the combination of surging deficits, increased Treasury supply and temperamental energy markets has stoked a view of structurally higher inflation and interest rates. As I’ve written before, I still think it’s histrionic to believe we’re heading for a world of permanent 3% inflation and 5.5% interest rates. But I’m coming around to the idea that history may repeat itself and that yields could take a run at 5.5% to 6% before the sovereign-debt bears throw in the towel.

Even if it’s just a detour, there’s no underestimating the significance of such a move. The jump in long-run yields (and mortgage rates, auto loans, corporate borrowing costs, etc.) could ultimately prove to be the downfall for markets and the economy. All else being equal, that risk scenario would mean, theoretically, 30-year mortgage rates nearing 9% and the S&P 500 Index probing the 3,600-3,800 range. For months, economists and policymakers have pondered why Fed policy didn’t seem to be slowing the economy, with some blaming excess pandemic savings and others the mortgage lock-in effect. Those had an impact, no doubt, but so did the shape of the yield curve: Many types of consumer and business loans simply didn’t reflect the restrictiveness implied by the policy rate. Now, increasingly, they do.

Others may view the developments in a positive light. If you believed that the economy was running too hot to tame inflation, then you must also believe that it can take a little extra restraint from higher yields and that perhaps they’re “just what the doctor ordered.” Personally, I’m less optimistic than I was in July (when 10-year yields ended the month at 3.95%), but I’m not ready to join the economic doomsday crowd. For the most part, the latest moves seem like a normal development at this stage in the Fed’s inflation fight. Whether the Fed can win the battle without triggering an economic downturn is still an open question, but the latest developments in the bond market have guaranteed that we’ll find out sooner rather than later.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

More Real Estate Topics >