When Congress voted in 2018 to give regional banks a break from stiffer post-crisis capital rules, it created a two-tier banking system in the US. One aim of the Federal Reserve’s reforms launched this summer was to undo that and ensure that all banks with more than $100 billion in assets meet the same standards as the biggest lenders.

But the US will still have a two-tier regime if these proposals pass – which is no slam dunk given the heated opposition. This matters because the banks that will remain lightly regulated have become increasingly important lenders. Failures among those with less than $100 billion in assets should be less damaging — but they might not be.

There are 4,136 banks in the US at the last count by the Federal Deposit Insurance Corporation. Under the Fed’s proposals to adopt the so-called Basel III Endgame, only 14 more US lenders will become subject to the stiffest rules, bringing the total in the top tier to just 23. There are five members of the KBW Banks stock index that will still get a light touch, including Comerica Inc. and Zions Bancorp NA.

Those 14 larger regionals and credit-card companies have a total of about $4 trillion assets, using numbers for the end of 2022, equivalent to slightly more than two Wells Fargo & Cos., or almost 20% of total US domestic bank assets, according to Fed data. This would mean roughly two-thirds of all US banking assets will be governed by the stricter rules. All of this top tier will face steeper capital requirements than they do today – with the biggest increases hitting the biggest institutions, like JPMorgan Chase & Co and Goldman Sachs Group Inc.

But the remaining 4,000-plus banks won’t be affected and their role in the economy has grown, especially in real estate lending, since the 2008 financial crisis.

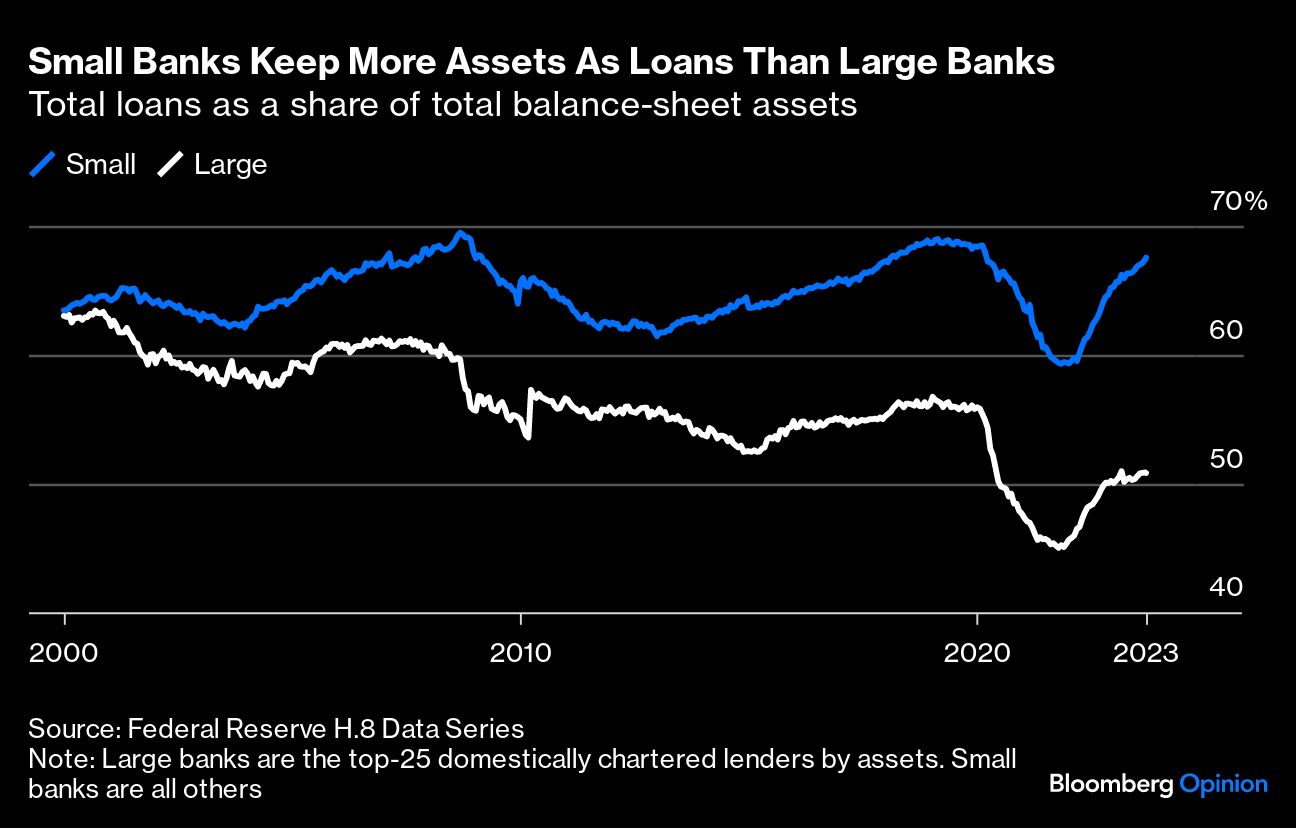

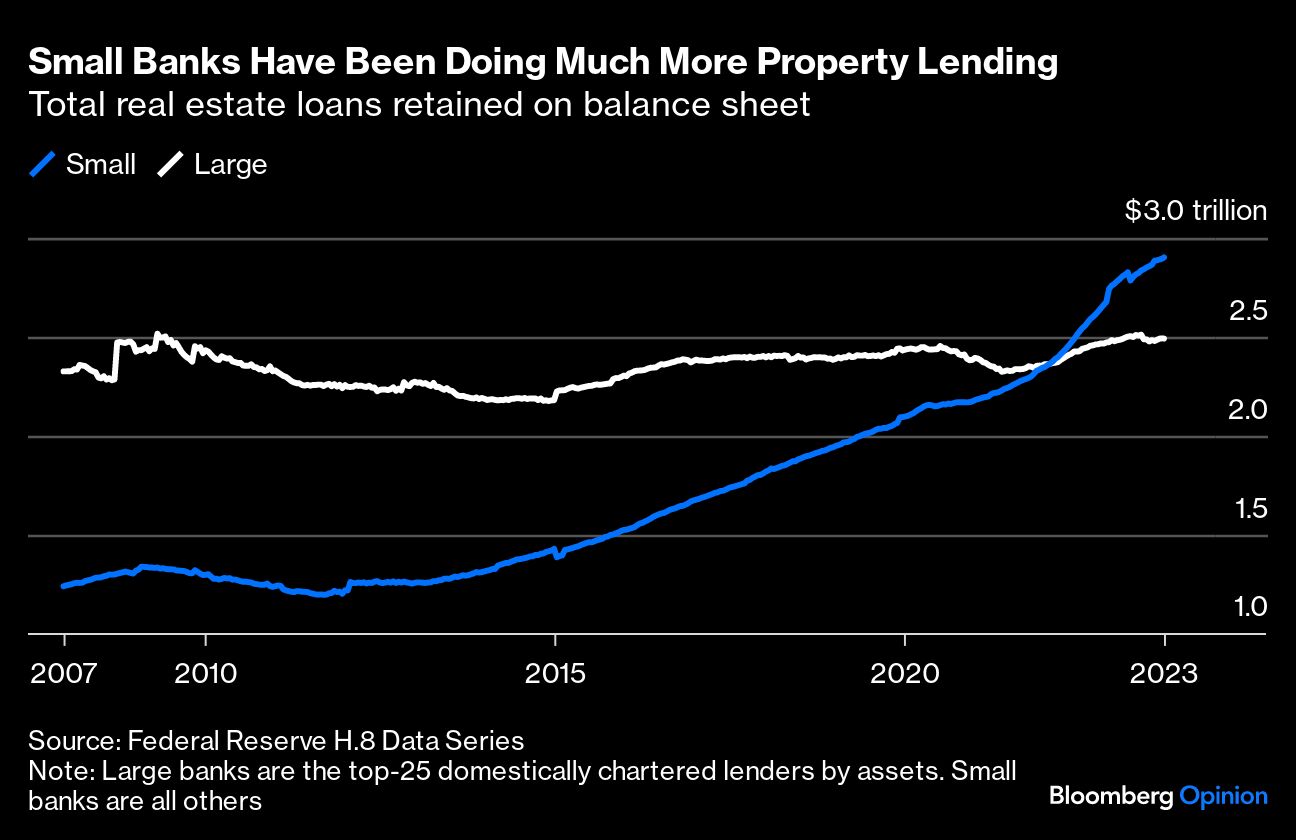

This is partly by design. The globally agreed post-crisis rules pushed big lenders to hold more liquid assets like cash and government bonds. Lots of credit risk found its way into markets instead, but in the US the smaller banks also enjoyed rapid growth.

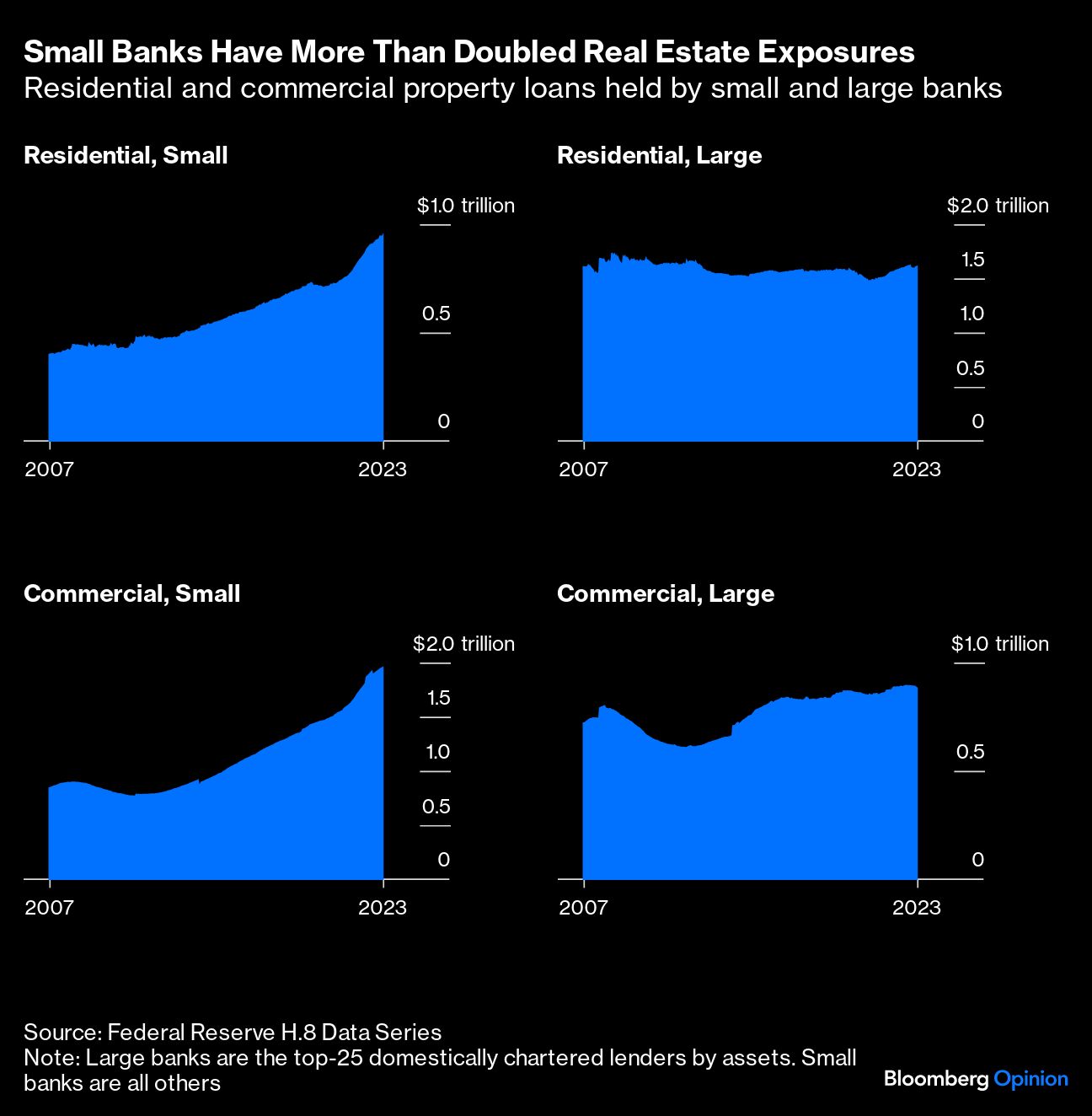

Small domestic banks have overtaken large banks in real estate lending in dollar terms, mostly driven by a huge increase in commercial property lending, according to the Fed’s H.8 data series. The top-251 domestic banks have $2.5 trillion of real estate debt on their books while all the rest have $2.9 trillion. Since 2007, total property lending and residential lending has remained essentially flat for the large banks, but small banks have grown both by more than 130%.

The new round of rule tightening would make writing mortgages far more costly in capital terms for the top banks. The Bank Policy Institute, a lobby group, has warned that borrowers with small down payments will be worst affected, making their mortgages potentially much more expensive. That could disproportionately affect lower-income families, first-time buyers and minorities, especially Black or African-American borrowers.

Larger banks want this changed and they have a decent chance that it will be. The Fed’s own economists have said it doesn’t want to restrict low- and moderate-income homebuyers from getting onto the housing ladder.

But aggressively geared lending isn’t necessarily healthy for borrower or lender. Alexa Philo of Americans for Financial Reform told the House Financial Services Committee last month that the 2008 crisis had devastating impacts on the wealth of people and communities of color. Foreclosures on subprime loans and falling home prices wiped out many Black and Latinx owners' home equity, which was a large part of their net worth, she said.

None of what is being debated will limit the ability of small banks or non-banks, which have also taken a growing market share, to lend aggressively. In my view, housing or income inequality would be better addressed elsewhere than through encouraging people to take on risky debt, but that’s another matter.

The broader point is that credit risk has been migrating to small banks, not just to markets, and that will continue under the Fed’s reforms. Maybe that’s the plan. Smaller banks might be restricted in how much they can grow: They are by nature less diversified and limited to local markets, and they sell fewer mortgages to government-sponsored agencies like Fannie Mae and Freddie Mac. Still, they have managed to collectively grow mortgage lending faster than the market has a whole, and they account for about one-fifth of the growth of all one-to-four family residential mortgages since 2007, based on Fed data.

Lack of diversification makes small banks more vulnerable, but that is meant to be OK: Small banks should be able to crash without hurting the wider economy or causing a crisis. The question is whether the $100 billion asset threshold is small enough: Regulators and Congress thought $250 billion was small enough until Silicon Valley Bank. Lots of small banks in the same area might all be making similar loans and could collectively become a major problem – that is one lesson to take from the Texas banking crisis of the 1980s, for example.

Big banks think the Fed’s new capital rules have gone too far — and they have some fair points. But the shift of risk into thousands of smaller banks should also have us asking whether the rules go far enough.

1The H.8 series is based on domestically chartered banks, which covers bank subsidiaries of big US groups and foreign groups. The top-25 overlaps considerably with the Federal Reserve list of 24 banks in the top regulatory categories, but isn't exactly the same.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recentwhite papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.