Bill Bengen: How to Monitor and Adjust Withdrawal Plans

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Bill Bengen has continued his groundbreaking research into retirement strategies. He has developed a framework for retirees to monitor and adjust withdrawals based on inflation and market performance.

Bill Bengen has continued his groundbreaking research into retirement strategies. He has developed a framework for retirees to monitor and adjust withdrawals based on inflation and market performance.

Bengen was a keynote speaker at the Insider’s Forum, the conference run by Bob Veres and Jean Sinclair that took place last week in San Antonio. Veres aptly introduced Bengen as one of the few “genuinely transformative people in the advisory profession.”

Bengen’s research originally sought to answer a simple question, “How much can you withdraw from your retirement portfolio?”1 His seminal research was published in 1994, featuring what became known as the “4% rule.” He was the first person to explore that question systematically and rigorously, and it has been studied by many others over the last 30 years.

In 2021, he determined that the safe withdrawal rate (SWR) was approximately 4.7%, based on a 50/50 portfolio of stocks and bonds and then-current equity valuations and interest rates.

His research since then has focused on a methodology to develop a plan based on a withdrawal rate, monitor it, identify deviations and decide what corrections to take.

Eight factors go into the design of a withdrawal plan, and Bengen reviewed each one and how various assumptions affect outcomes.

1. Choose a withdrawal scheme. Advisors must choose a rule for determining how much to withdraw from the underlying assets on a regular basis. This is a mathematical description of how to take money out of an account. The most common method is to withdraw a fixed percentage after adjusting for inflation. This is the scheme Bengen has used in his research, and he referred to it as a cost-of-living adjustment (COLA). But other methods are possible, including front-loading to allow for more money to be spent up front (e.g., for travel) and to cut back later. Bengen also mentioned the use of fixed annuities, such as single-premium immediate annuities, which don’t offer inflation protection. “Every scheme has a different number,” Bengen said.

2. Select a plan duration. He uses a 30-year retirement in his research, but he said there needs to be a margin of error for the uncertainty of life expectancy (particularly as people live longer).

3. Specify the type of withdrawal account. Bengen’s 4.7% is for a qualified plan, and the corresponding rate would be lower if assets were held in a taxable account.

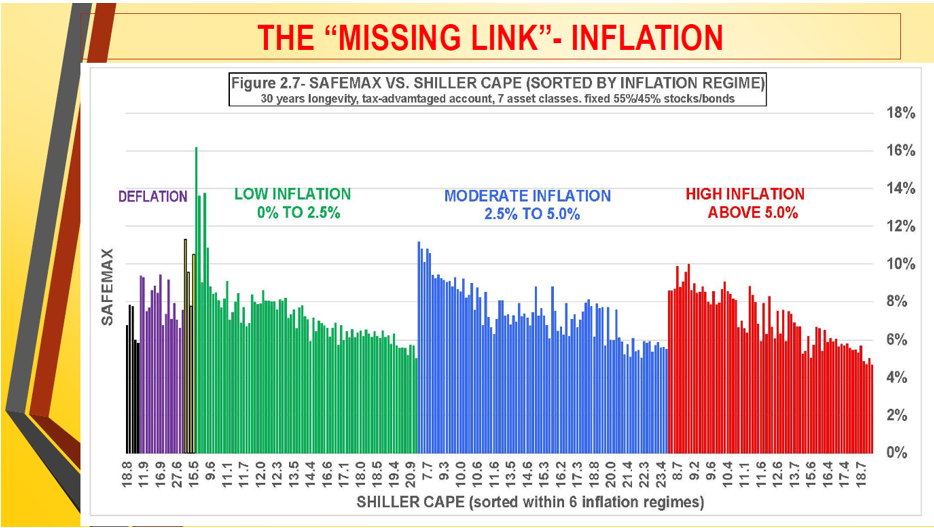

4. Select the initial withdrawal rate. This is the most crucial aspect of plan design and the one Bengen spent the most time discussing. There are two assumptions that must be made: the level of equity valuations, for which Bengen used the Shiller CAPE ratio, and an inflation regime. Given those two assumptions, one can determine the “SAFEMAX,” which is the maximum that could be withdrawn from the portfolio based on historical starting points with the same CAPE and inflation.

The incorporation of valuations (the CAPE ratio) and inflation is an improvement over how this research was done previously. The old way was to select a withdrawal rate, which had an associated probability of success (i.e., of not running out money) based on historical experience. For example, a 7% withdrawal rate might have a success rate of 50%. The problem, according to Bengen, is that it is hard for clients to make decisions using those probabilities. Most clients want a 95% probability of success, he said. But then things go well (e.g., the markets perform strongly) and they regret making that decision.

In 2008, Michael Kitces introduced the use of CAPE valuations in estimating SWRs. He determined the ex-post SWR based on CAPE ratios (e.g., the SWR was 16% after the Great Depression, when someone could start retirement at historically low equity valuations). Kitces’ work showed there was approximately a 75% correlation between CAPE ratios and SWR. But Bengen said that is not good enough to reliably predict SWRs. “It is not strong enough to do the job,” he said, because retirees could not tolerate situations where, for example, their SWR could be anywhere between 4% and 10%.

Bengen found the improvement that was needed, which was to incorporate inflation. About two years ago, he did that by segmenting inflation into six regimes (low, moderate and high inflation and deflation). He looked at the beginning CAPE and the resulting SWR within each regime and found there was a near-monotonic declining SWR as CAPE increased with a 90% correlation. The only period it did not work very well was the late 1980s, when stocks were cheap but got very expensive later, allowing for higher SWRs. The results are shown in the graph below:

5. Choose an asset allocation. Bengen has been using 55/45 stocks/bonds.

6. How much of a legacy is desired? The greater the legacy, the lower the SWR.

7. Rebalancing interval. How frequently is the asset mix rebalanced to its target? Bengen did not say whether more frequent rebalancing leads to higher or lower SWRs, and it is unlikely there is a reliable relationship.

8. Are above-index returns targeted? Bengen used index-fund returns for his analysis but acknowledged that some clients may employ active management with the hope of increasing the SWR.

Two case studies

Bengen next used two case studies to illustrate his methodology. In each, he took a hypothetical combination of a CAPE ratio and an inflation rate and matched those to a historical period. Once a match was made, it yielded what he called a current withdrawal rate (CWR). He then determined whether the CWR would have succeeded (i.e., not depleted the assets) over the ensuing 30 years.

The first case study used COLA-based withdrawals over a 30-year period with moderate inflation and a CAPE of 14.8. That was the case in 2009 and matched the conditions in mid-1986. Bengen’s model predicted a CWR of 7%. But in 1986, the retiree would have faced adverse market performance in the subsequent five years. Bengen showed that, in retrospect, the best option was to do nothing, and to not adjust withdrawals or asset allocation. The lesson, according to Bengen, is not to panic, because bear markets are usually followed by strong recoveries.

The second case study started with a CAPE of 22.3 and moderate inflation. This matched the conditions in 1966, and the retiree would have faced four bear markets and significant inflation over the ensuing 30 years. Indeed, inflation would have hit in the third year, putting the retiree short of their withdrawal goal. If withdrawals were not reduced, the retiree would have faced “tremendous concerns” 10 years into retirement, he said. The lesson, Bengen said, “is that you cannot ignore inflation.” Reducing withdrawals by 10% in year five would not have been enough to avoid depleting one’s assets. A 30% cut was needed to get back on plan.

“Inflation is the greatest enemy of retirees,” Bengen said. “It is much better to make a big cut sooner rather than a bigger cut later,” under those conditions.

Bengen plans to turn his research into a comprehensive management scheme for retirement withdrawals and to integrate it with financial planning software. He also hopes to have a new book next year.

Practical implications

Bengen is correct that inflation is at least as great a risk to retirees as a bear market. But by not including Treasury inflation-protected securities (TIPS) in his asset allocation, he misses the opportunity to create a risk-free hedge against that outcome. A year ago, Advisor Perspectives published an article by Allan Roth that showed that a TIPS ladder could be constructed to guarantee a 4.36% SWR. Real rates have risen since then and are approximately 2.5% across the yield curve. One can now build a TIPS ladder that yields a SWR of approximately 4.76%.

A risk-free SWR of 4.76% should be the first consideration in any retirement plan. If a TIPS ladder yields sufficient cash flow for a 30-year period, there is little reason to consider anything else. There will be many who need more cash flow, and that decision should be grounded in a consideration of the risks of allocating to riskier assets versus the TIPS ladder.

I asked Bengen what his model would say for those retiring today, with the CAPE ratio at approximately 31 and inflation at 3.7% (based on the headline CPI). He said it is “off the map.” There is no historical precedent that yields any guidance.

Bengen’s research revealed valuable insights into the relationship between equity valuations (CAPE ratios), inflation and SWRs. It should be combined with other methodologies, such as Monte Carlo analysis, to illustrate the risks and distribution of outcomes that retirees face.

Robert Huebscher is the founder of Advisor Perspectives and a vice chairman of VettaFi.

1 More precisely, how much can you withdraw on an inflation-adjusted basis over a 30-year timeframe?

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All