Emerging-market currencies erased their Friday gains and were poised for a third week of declines as a stronger-than-expected US jobs report underscored global interest rates could remain higher for longer. Stocks pared the day’s gains while credit risk premiums surged.

A currency selloff in Latin America resumed, with the Mexican and Chilean pesos leading MSCI Inc.’s benchmark lower for the fourth day in five. The losses came after a gauge of returns from carry trades in 18 major developing-nation currencies showed the worst losses since China ended its Covid Zero policy. Investors hoping for a fourth quarter rebound in EM assets have already seen those hopes dwindle this week, with fresh causes for concern arising from North Africa to Latin America.

“Markets have been priced for a Fed that has reached its terminal rate, and today’s data raises the possibility that the Federal Reserve could hike again in November,” said Brendan McKenna, a strategist at Wells Fargo in New York. “With most emerging-market central banks already cutting, especially in Latam, rate differentials swing more notably in favor of the dollar and away from EM currencies.”

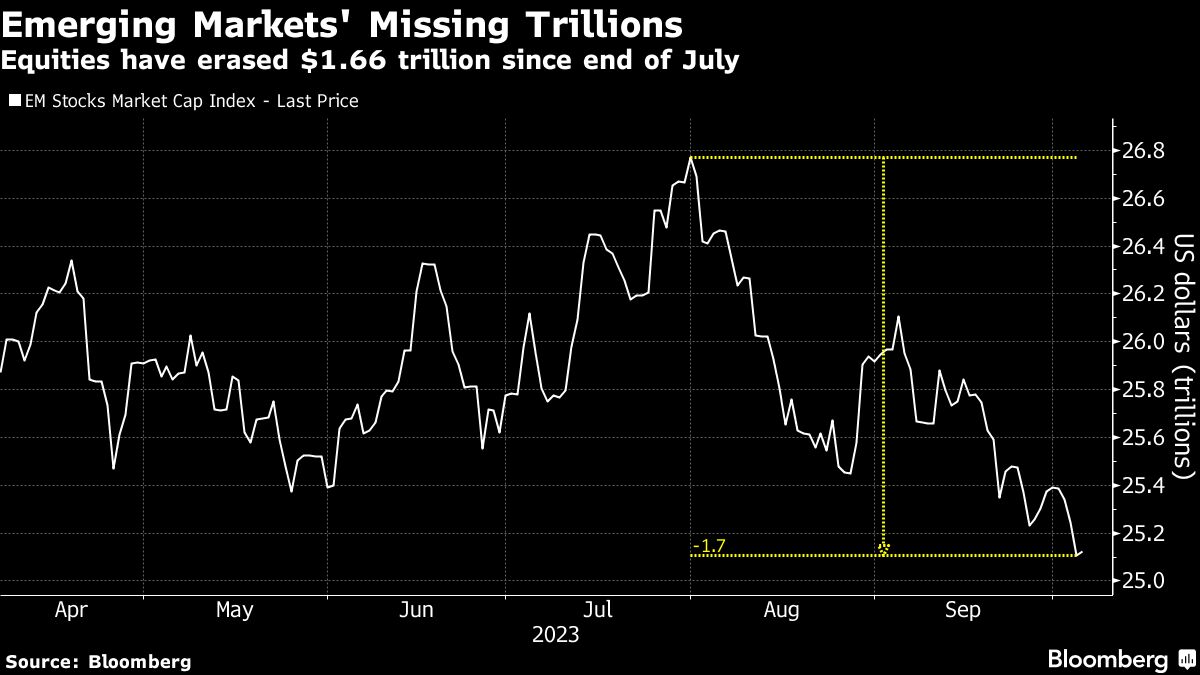

This week’s selloff hasn’t spared stocks and bonds either. About $266 billion of shareholder wealth was erased even though the biggest emerging economy — China — was closed for holidays. The surge in US yields is hitting poorer nations hard — sending the average sovereign borrowing costs soaring to highs seen during the pandemic era.

At this rate, this could be the first time since 2015 that carry traders make losses for three successive quarters. Stocks are within a hair’s breadth of falling to the lowest level since 2001 relative to US stocks. Bond yields would cap a third year of increases, also the longest streak since 2015.

“Given that fundamentally there is no relief for US rates yet, even though technically there are some early signs for a plausible stabilization, we remain cautious in emerging markets,” Citigroup Inc. strategists including Dirk Willer wrote in a note. “We prefer to wait for a clearer sign that rates have indeed peaked before wading back in.”

Meanwhile, fears of deepening debt distress have returned to emerging markets. Egypt was put on notice by the International Monetary Fund’s Managing Director Kristalina Georgieva, who said the nation would bleed foreign-exchange reserves unless it devalued its currency again. Moody’s Investors Service downgraded Egypt to one of the lowest rungs of speculative grade, helping to send its dollar bonds to the worst performance in emerging markets Friday.

Investors began betting that Ethiopia could turn out to be the next country to default on its debt, push its lone dollar bond to the verge of erasing its peace-process gains. Meanwhile, Hungarian yields jumped amid growing evidence of a continued recession.

Latin American currencies have been punished this week in the risk-off shift and policymakers weren’t helping their cause. The Mexican government’s tweaks to its airports tariff policy shocked the stock market, but also spilled over into a peso selloff.

While an earlier spike in oil prices boosted concerns over resurgent inflation and sparked a selloff, this week’s drop in crude futures contributed to losses in currencies such as the Colombian peso.

In the equity markets, meanwhile, the strongest signal of deepening bearishness came from the exchange-trade fund market. BlackRock Inc.’s benchmark fund for the asset class witnessed $757 million of outflows on Thursday alone, the worst in four years. The fund has lost 8% of its assets this week alone.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Srinivasan Sivabalan