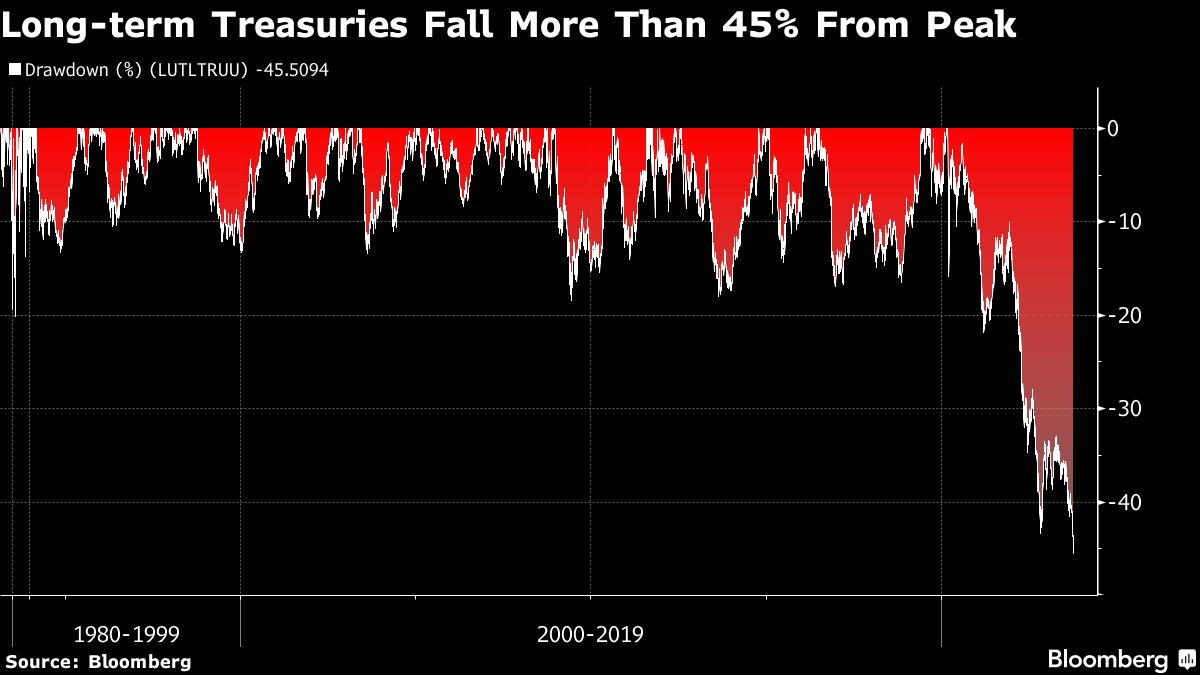

Losses on longer-dated Treasuries are beginning to rival some of the most notorious market meltdowns in US history.

Bonds maturing in 10 years or more have slumped 46% since peaking in March 2020, according to data compiled by Bloomberg. That’s just shy of the 49% plunge in US stocks in the aftermath of the dot-com bust at the turn of the century. The rout in 30-year bonds has been even worse, tumbling 53%, nearing the 57% slump in equities during the depths of the financial crisis.

The extent of the losses is a stark reminder of the risk that comes with piling into longer-dated bonds, where prices are the most sensitive to changes in interest rates. That was part of the appeal of the securities as the Federal Reserve spent the better part of a decade cutting borrowing costs to near zero.

But as the central bank has carried out the most aggressive monetary-policy tightening in decades to rein in runaway inflation, the mix of historically low starting yields, long-maturity debt and rapidly rising rates has proven to be a painful combination.

“It’s quite something,” said Thomas di Galoma, co-head of global rates trading at BTIG and a four-decade market veteran. “To be honest with you, I had never thought I would see 5% 10-year notes ever again. We got caught in an environment post global financial crisis where everybody just thought rates were going to remain low.”