Hedge funds are in regulators’ sights again. Their risk-taking with borrowed money must be better monitored and will sometimes have to be limited, the head of a global group of supervisors told the Financial Times last week.

But it isn’t just hedge funds. The Financial Stability Board is reviewing the growth of leverage in markets so it can combat the risks posed by all non-bank money managers, according to the comments from Klaas Knot, the Dutch central bank chief who also chairs the FSB. Regulators want more disclosure of how much borrowing and leverage from derivatives exists and even to cap what some players can do.

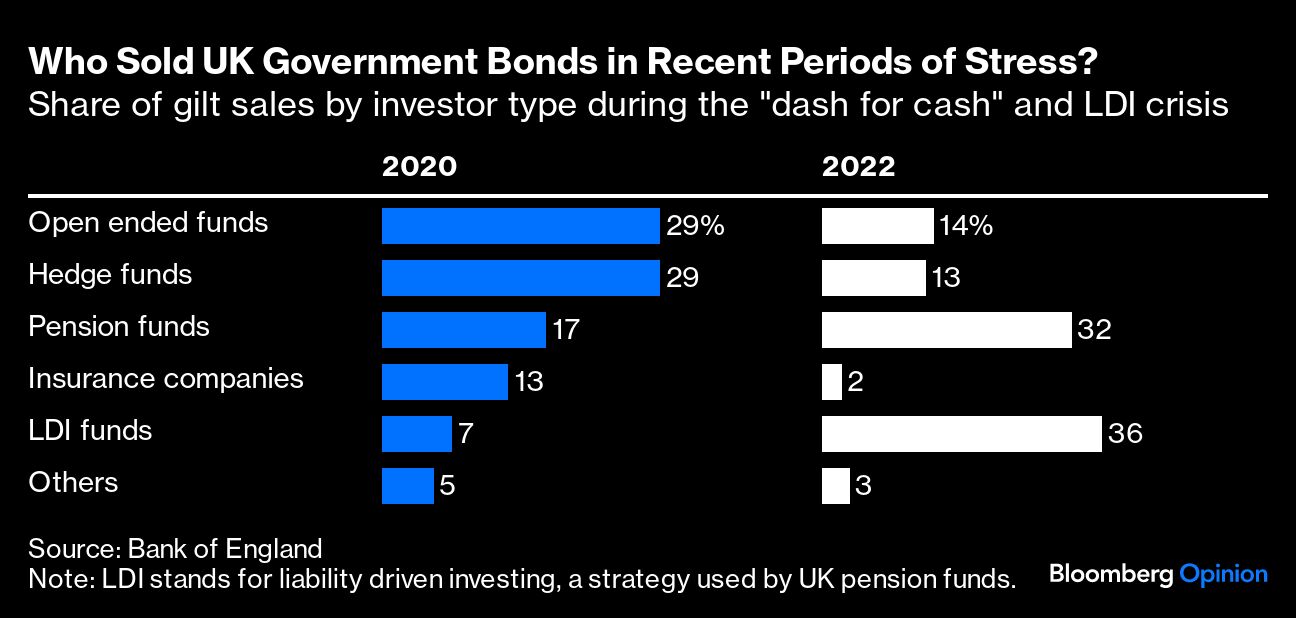

This seems a natural reaction to a string of crises, from the 2021 collapse of the hedge fund Archegos, which cost banks billions of dollars, to Britain’s pension-fund-driven government bond market blowup in 2022 and to the chaotic “dash for cash” at the start of the Covid-19 pandemic.

What’s going on here is bigger than a few episodes of market mayhem, however. This FSB review is part of a fundamental shift in central bankers’ view of financial markets. To see why, read the speech given last week by Andrew Hauser, the Bank of England’s executive director for markets, about “filling gaps in the … liquidity toolkit.”

Behind this unpromising subtitle is a radical plan: The BOE will become the permanent lender of last resort to investment funds in the way it has been to banks for hundreds of years. Initially, this support will be available only to insurers and pension funds, but it is exploring how it might bring in hedge funds and other asset managers in the future. There are many details to be ironed out but a necessary quid pro quo is stricter monitoring and regulation.

The UK plan goes further than the Federal Reserve’s Standing Repo facility, which allows it to lend to the shadow banking system, but through dealers. I think other central banks will follow the BOE. Why? Behind all the dry technical talk of systemic risks and liquidity shocks lies a very simple recognition. A run on financial markets causes the same lethal problem as a run on banks: It drastically restricts or cuts lending to the economy.

Hedge funds, dealers, mutual funds and so on collectively supply massive amounts of credit to industry and society. This role has only grown in size, importance and complexity since bank regulation was tightened after the 2008 crisis. The non-bank financial system has doubled in size and now accounts for half of all financial assets globally, according to the FSB. Hauser’s speech delivered a startling statistic: Almost all of the £400 billion ($488 billion) increase in net borrowing by UK businesses since the global financial crisis came from market sources rather than banks.

Central banks had to prop up financial markets alongside banks during 2008. Since then, every crisis has forced them to create new ways to lend temporarily to specific types of managers or assets: from money market funds to junk-rated leveraged loans. Central bankers have gotten very good at cooking up new programs quickly, but they don’t always work as hoped, and in 2020, it took multiple kinds of lending to halt the spiraling chaos gripping markets.

It might sound blindingly obvious that markets need support a bit like banks, but there has long been strong opposition to the idea of central banks expanding their operations like this — from finance and politicians. The arguments against it take the view that investment funds are different from banks. Investors know their money is at risk and if they lose some it shouldn’t matter in the same way that it does if deposits flee a failing bank. Such losses shouldn’t be as disruptive to anyone’s ability to pay bills, or rent or employee wages.

This view is too simplistic: It was before 2008 and it definitely is today. The money you invest in a hedge fund, or pension, or even a money-market fund might not be so immediately important to the payments system, but it is to the funding of consumers, companies and the government. When shadow banks, or non-bank financial intermediaries, create credit for businesses, they use leverage and derivatives and collateral, which tie the fortunes of these markets and money managers together.

Shadow banking is a lot like traditional banking in a disaggregated form – no individual asset manager is like a bank, but collectively they are. The market system transforms short-term, easily withdrawn money into long-term lending like a bank does, but in markets it happens across a chain of related transactions rather than within the four walls of a single bank. And while a bank creates money based on trust, shadow banks do it based primarily on government bonds as security. As Hauser put it in his speech: “To support this activity, NBFIs [non-bank financial intermediaries] have become increasingly important players in the core markets that lie at the heart of the economic and financial system.”

You don’t need a complicated economic theory to understand this; you just need to witness how central banks have been forced to bail out markets when crisis strikes. The supply of credit also isn’t purely a financial question: When it collapses, it leads to job losses, business closures and poverty and that is a political problem.

Throughout the past few hundred years at least, banking existed as part of a political bargain. How much lending is supplied to whom, what profits banks get to make, what support they get from the state in times of crisis and what rules and guardrails they in turn must obey arise from an ongoing political negotiation.1 Whether profits and bonuses are kept when taxpayers are saddled with bailout bills is part of this bargain too.

Hedge funds, money-market funds, pensions and insurers are being drawn into a similar “Grand Bargain” as Hauser called it. They might have leverage limits imposed in some areas, as Knot suggests. They might be forced to hold more cash to try and ensure they only need to borrow from a central bank in the most extreme of circumstances – just as banks have had to meet tougher liquidity rules.

Many asset managers will protest. They might not even want the kind of protection central banks are increasingly going to offer. But economies need them to have it, and such support doesn’t come for free.

1 I read an excellent book over the summer on this topic called Fragile By Design: The political origins of banking crises and scarce credit by Charles Calomiris and Stephen Haber.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul Davies