Why Are Elephants So Smart and Buildings So Short?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe can and do build much taller skyscrapers. But they are impractical money losers because so much floor space is taken up by elevators. A new book explains the interplay between size and scale, and what it means for our economy and investments.

Vaclav Smil, the 80-year-old Czech-Canadian scientist whom Bill Gates cites as his favorite author, rarely disappoints. Smil’s 2022 book, How the World Really Works, is a superb paean to the physical world and its primacy in our lives – warning us that idealistic techies are wrong when they claim that teraflops and petabytes are what matters. As the economist Michael Edesess noted in his book review in Advisor Perspectives last year,

If you’re a modern techy, you might say [that]... the four pillars of modern civilization... [are] something like the microchip, the cloud, the internet, and wi‑fi. Nope, says Smil. The four pillars of modern civilization are cement, steel, plastics, and ammonia.

“He’s right,” concluded Edesess, as do I. The material world matters. Many of us, dazzled by information technology, underestimate the importance of natural resources, materials science, and good old-fashioned heavy industry. (Without synthetic ammonia, used to make fertilizer, half of us would starve. Good to know.)

How the World Really Works also put a dent in the hopes of energy-transition enthusiasts. It will take a lot of time, money, and materials. Previous energy transitions took 40 to 60 years, Smil argues.

This one will too.

Smil’s latest book, Size: How It Explains the World, homes in from the very large – the workings of the whole world – to a more modest, focused topic: the sizes of things and how they affect us. While everything Smil writes is elucidating, I’m reluctant to recommend Size, not because it is a bad book, but because so many books on related topics, including most of Smil’s, are better. The two-and-a-half chapters on scale are quite good – they are the second half of chapter 4 and all of chapters 5 and 6. The connections Smil makes between Galileo, Jonathan Swift, animals, plants, and buildings regarding the effects of scale are Smil at his best.

But reading the whole book – just because Smil wrote it – is a poor time allocation decision when both Geoffrey West’s superb Scale, which I reviewed very favorably, and Sebastian Mallaby’s The Power Law (the latter being about scaling in venture capital, for the investment-minded and reviewed here) are easier and more fun to read. The chapters in Size that are not about scale are filler, mushing together some vaguely size-related concepts such as the golden ratio in art and architecture, the science of ergonomics, and the basics of normal and Pareto (power-law) probability distributions.

In this review, I focus on Smil’s scale chapters. I then discuss size and scale in business, a topic that Smil does not cover.

Why are elephants so smart and buildings so short?

Scale sounds like just as abstract a concept as size, so let’s make it more concrete. As Smil (and West) use the word, it’s the way the size of one thing varies with a change in the size of some other related thing. For example, one might guess that the brain-to-body-mass ratio of an animal would predict its intelligence, but the prediction is wrong until you correct for scale. An elephant’s brain is small relative to its body, but its intellect is impressive; the tiny tree shrew has the largest brain of any animal relative to its body but that does not make it smart.

The overarching principle is that the brain-to-body-mass ratio that maximizes intelligence is smaller in big animals and larger in small animals. The relation among these variables is nonproportional. (To explain why would take a whole book, so I won’t try.)

Nonproportional scaling factors are everywhere. Brian Potter, an engineer who writes about the economics of buildings, explains:

As a building gets taller, more and more elevators are needed to service the upper floors, which intrude on the floors below. The result is that a taller building must devote proportionally more and more of its space to elevators.

For a one-story building, and most two- and three-story buildings, the ratio of elevator space to building space is zero. For the tallest buildings, it can be 40%. That is why, in Potter’s words, “skyscrapers are so short” (when it comes to usable space).

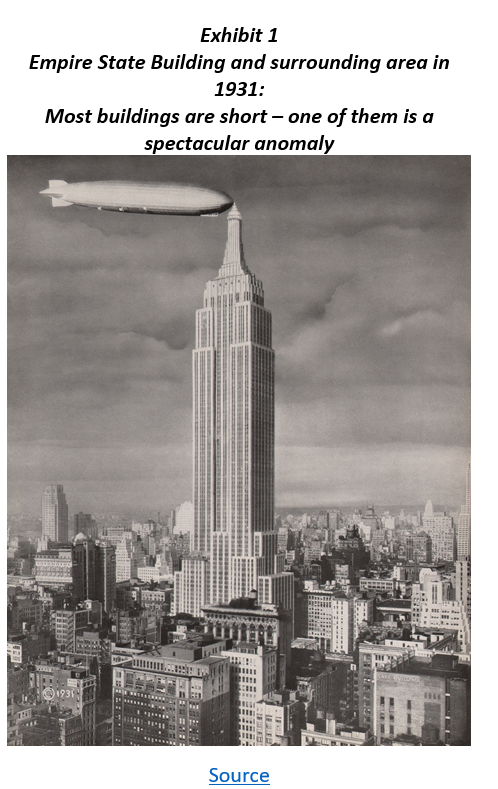

Skyscrapers aren’t short compared to other buildings, but they are short and inefficient relative to what they could be if there were no scaling effects. Moreover, the structures near them are often surprisingly short, suggesting that very tall buildings might be a peacock’s tail, showing the world how wasteful the builder can afford to be. Exhibit 1 is a famous example from 1931, combining the majestic and the comical. (The dirigible adds a nostalgic note – did people really ride in those?)

Later, as land values rose, the city filled in and the Empire State Building doesn’t look as out of place today as it did then. But the world’s tallest building has moved offshore – it’s currently the Burj Khalifa in Dubai – and that one looks as out of place as the Empire State Building did in 1931. Extreme tallness in buildings is a money-losing monument to the ego of the builder.

Brobdingnag and Lilliput

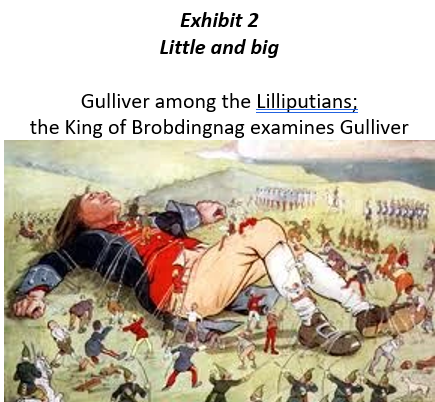

Smil introduces us to these scaling concepts by way of Jonathan Swift’s Gulliver’s Travels. As most schoolchildren know, normal-sized Lemuel Gulliver visits a race of tiny people one-twelfth his height (about six inches tall) and a race of giants 12 times Gulliver’s height (about 72 feet tall). In describing these characters, Swift commits a bonehead error – he “built his masterpiece,” Smil writes, “on the mistaken assumption that such a thing...is perfectly possible” with no change in the way the creatures look and behave.

Smil notes that Swift would not have made that mistake if he had read Galileo’s Dialogue Concerning Two New Sciences, written in 1638, some 84 years before Gulliver. We tend to think of Galileo as an astronomer because of his mammoth contribution to that field, but he was also a general scientist of remarkable ability. His description of the way that scale affects the proportions of animals, summarized by the Brazilian physicist Francisco Rodrigues here, is still our best understanding 400 years later.

Smil dissects the Gulliver problem, explaining that a Brobdingnagian, if he had the relative proportions of a normal human but were 72 feet tall, would weigh 116 tons, more than the largest known dinosaur. His legs would crumble from his weight unless they were several times thicker than an elephant’s, and he would have many other traits that we’d consider deformities. In other words, he would not look human at all, and could not run, jump, or do many other physical things that a human easily does.

The six-inch-tall Lilliputians would also have scale-related problems, albeit different ones – though, as shown in Exhibit 2, they can tie down big Gulliver if, like ants, they band together.

The tale of a whale, a bird, and a tree

But wait...there is an animal that weighs more than 116 tons! You’ve probably already guessed that it’s a blue whale, the largest animal known to have existed. It can survive and thrive because it lives in the water. Weighing almost nothing after accounting for water displacement, the blue whale functions beautifully in its own environment. It is, however, a complete disaster in any other environment. It can’t stand up or walk. The scale of the whale requires that it be aquatic for its entire life.

At the other extreme, a small bird called the bar-tailed godwit has flown 8,435 miles, from Alaska to the Australian island of Tasmania, without stopping. (See Exhibit 3.) It comes close to living in thin air, needing to touch down only to rest and find food. This avian ultramarathoner must carry the many calories needed for this trip in its body; there are no bird restaurants in the sky. A larger creature could not possibly do this – consider how many times a human being trekking that many miles would have to stop and eat.

Thus, Smil concludes, the possible variations in the physique and behavior of a living creature are tightly constrained by their size. In case you’re thinking that this law doesn’t apply to plants, you’d be wrong – it just applies differently. Not needing to move about, a plant can grow larger than any animal. The world’s heaviest tree, the General Sherman sequoia in California, is 276 feet tall and weighs 566 tons, as much as five blue whales; the world’s tallest tree, a skinny California coast redwood called Hyperion, is 380 feet taller but not as heavy. No tree is likely ever to grow much taller or heavier than these behemoths because it would collapse of its own weight.

The laws of scale that apply to animals and plants, but with different parameters, also apply to buildings, cities, microchips, and everything else...

All businesses great and small

...including businesses. Here’s the bridge between Smil’s intellectual horseplay and the world of investing: The scale of a business is fundamentally important to its organization and behavior. Like our tall building that needs a lot of elevators, a multinational corporation requires many more layers of management than a taco stand. From that perspective, a large business can look very inefficient. But large size also conveys many advantages (economies of scale) to a business, the most obvious of which is bulk purchasing. In a Darwinian fashion, the market weighs the advantages and disadvantages of large size, and a balance is reached for each kind of business, just as it is reached for each species of plant or animal.

For this reason, aircraft manufacturers are large and handicraft shops are small. We already know this, but it’s helpful to understand why. The reasons emerge from the laws of scale.

Size, scale, and stock selection

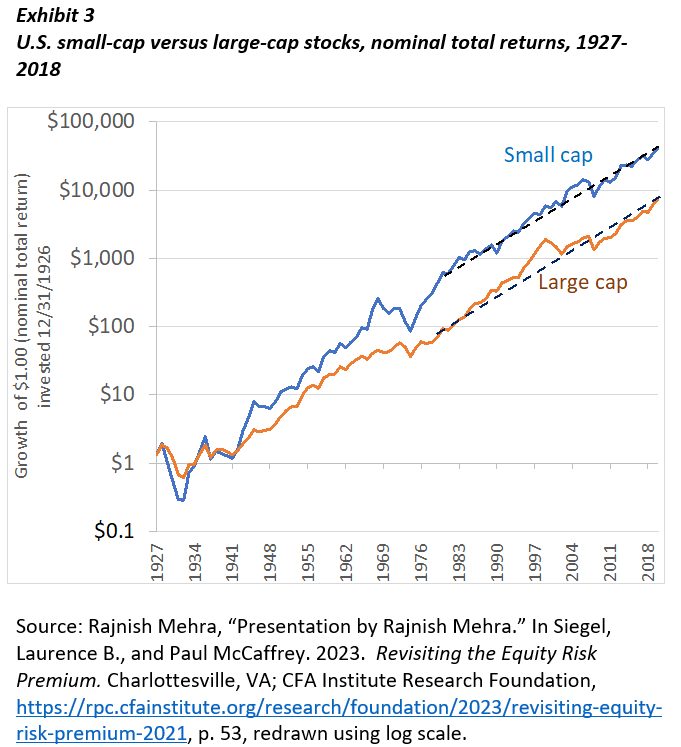

Investors are, of course, intimately familiar with one dimension of size – the market “cap” of stocks. From 1926, when reliable data began, through about 1980, small-capitalization stocks outperformed large ones by a fat margin – enough, on average, to spawn a whole new category of mutual funds and other investment vehicles. After the small-cap effect was discovered around 1980, however, the effect disappeared and the two size categories fought to a tie. (See Exhibit 3.)

This is not to say that small caps had the same return as large caps year after year – they often diverged widely – but there has been no size effect on net from 1980 to 2023, with small caps winning in some periods and large caps in others. Thus, while it looked for a while as though small size conveyed big advantages when investing in publicly traded companies, that turned out to be an advantage that was arbitraged away.

But equity analysts look at other aspects of size: a company’s revenues, profits, number of employees, geographic extent of its market, land area of the physical plant, and so forth. One reason to make such a careful study of size is to determine if the company is well positioned to create a quasi- or earned monopoly in some aspect of its business. If it is, that makes the company worth more. It’s hard for small companies to earn monopoly profits unless the monopoly is very localized or it makes a niche product; to earn monopolistic returns, you want to be as big as possible.

Another reason to be concerned with company size is to forecast how much regulatory attention will be focused on the company; here, large size is a disadvantage. Still another reason is to assess the likelihood of labor unionization – big companies are more susceptible to it.

Moreover, companies are subject to scaling effects, meaning that the impact of size on success can be nonlinear (in either direction). Small companies have the advantage of being nimbler and more experimental – look at the private-equity-funded energy sector today – but some things can only be done efficiently by large ones. Interconnecting the country for electric, telecommunications, water, and natural gas utilities is an example; we have more than a century of evidence that natural monopolies exist in those businesses. The large-cap companies that did this work were good stocks to own while the quasi-monopolies lasted. Radio, which provides a similar service but doesn’t need wires or pipelines (so there is much less capital outlay), has never been a natural monopoly, and small stations often became industry pioneers and big profit-makers.1

Only a Google-sized company could have digitized a large fraction of the world’s books. Sadly, Google must wait for the laws to change so the public can read the books; only a few selected parts, for example the British Library’s vast antiquarian (pre-1877) collection, have been allowed to circulate online. But this stranded asset will someday have tremendous commercial value. Some stocks should be expensive, and the stock of Google’s parent company, Alphabet, certainly is.

In business as well as in biology, architecture, and just about everything else, scale matters.

A broader view of Vaclav Smil’s work

I close with an overview of Vaclav Smil’s oeuvre and how Size fits into it. As an energy expert, Smil often finds himself at the center of a whirlwind of passionate opinions on the topic. He is called a pessimist by optimists and vice versa. To this, he replies: “I am neither a pessimist nor an optimist. I am a scientist.”2 He calms the passions by taking moderate positions, emphasizing solutions rather than imminent disaster.

But he does not get everything right.

Must growth come to an end?

In a widely quoted sound bite in his 2019 book, Growth, Smil wrote that “[G]rowth must come to an end. Our economist friends don’t seem to realise that.” This quote has been used by the degrowth movement to support their cause and by techno-optimists to illustrate how wrong a great scientist can be. In fact, the quote is both exactly correct and profoundly wrong.

No physical quantity can grow at a positive rate forever. That is as incontrovertible a fact as any.

What our economist friends know that Smil does not, however, is that what people try to maximize is not a physical quantity. People try to maximize utility – the amount of satisfaction or usefulness they get out of whatever they’re consuming. Theoretically, utility can grow at a positive rate indefinitely. Whatever satisfaction or usefulness you got out of a given pile of goods and services this year, you might be able to get a little more next year. Maybe it’s just a matter of becoming more psychologically well-adjusted, or maybe the quality (not the quantity) of the goods and services will have improved.

While projecting this betterment forever is a stretch, this principle focuses the mind on utility not being constrained by physical limits. Utility exists only in people’s minds, so there are no limits to it.

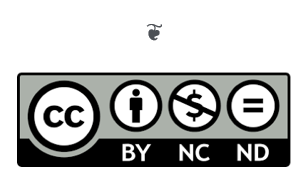

Dematerialization

There’s more good news. We are not only getting more utility out of the pile of goods we produce – we are using fewer resources to make them. This is called “dematerialization” and is another path to sustainable growth. Not only do our economist friends know that – so does Smil, who wrote a book about it, called Making the Modern World: Materials and Dematerialization (2013). It is not entirely optimistic, and he does not think dematerialization will solve all our resource problems, but he is keenly aware of the phenomenon.

Smil recognizes that some further increase in resource use is necessary and good. Some people – several billion of them – need more stuff. “Too many people still live in conditions of degrading and unacceptable material poverty,” he writes, and “all of those people...need to consume more materials per capita in order to enjoy a decent life.”

Smil’s book on dematerialization is worthy, but a much shorter and easier read on the topic is chapter 23 of my book, Fewer, Richer, Greener (2019). The chapter is titled “Dematerialization: Where Did My Record Collection Go?” and is available here as a free download. If you access it, please do not redistribute or repost it. Smil’s work features prominently in my book chapter.

Side trips

Smil has written more than 40 books. Size fits into this body of work awkwardly. Many writers, some successfully and others less so, veer off into topics that are not their core expertise but that they find interesting: Edgar Allan Poe wrote a textbook on mollusks, and Robert Louis Stevenson wrote a nonfiction book celebrating laziness. Size has the same feel, that of an author exploring a side path. Smil has done this before, in Why America Is Not a New Rome and Should We Eat Meat? These are not his core interests – I guess he just felt compelled to say something about them.

Smil has it in him to write an engrossing and informative book on size, scale, proportion, and related concepts. He did not do so. Although it contains some fine chapters, Size does not hang together as a book.

Advice to readers and investors

Investors should treat Size as deep background. Most investors would be well advised to read other books on related topics, such as Geoffrey West’s Scale and Pulak Prasad’s What I Learned About Investing from Darwin, which I reviewed here – to study these ideas. An economy is much like an ecology, and investors should be aware of the recent literature that clarifies and builds on this connection.

Smil’s writing style is heavy, packed with information. Many readers prefer a breezier approach, but Smil is such a knowledgeable writer, thinker, and researcher that one would be remiss to skip him entirely. To learn about size and scaling, read Scale – and to know how the world operates, read Smil’s How the World Really Works.

Laurence B. Siegel is the Gary P. Brinson director of research at the CFA Institute Research Foundation, economist and futurist at Vintage Quants LLC, and an independent consultant, writer, and speaker. His books, Fewer, Richer, Greener and Unknown Knowns, explore ideas in economics, investing, environmentalism, and human progress. His website is http://www.larrysiegel.org. He may be reached at [email protected].

The author thanks Stephen C. Sexauer, CIO of San Diego County Employees Retirement Association, for helpful comments and revisions.

1 Professional economic historians and other sticklers will note that the first radio networks (CBS and so forth) were in fact linked by wires. That phase, however, did not last long and does not appear to have been a critical aspect of that industry’s history.

2 In How the World Really Works.

[the troublesome content-free endnote i is now gone, and the endnotes are correctly numbered.]

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All