How Venture Capital Thrives by Betting on Weirdness

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWho would want to be tasked with investing their own and other people’s money in companies run by weirdos and jerks? But that turns out to be one of the most important skill sets shared by successful venture capitalists.

“Reasonable people,” begins Sebastian Mallaby in his excellent history of venture capital investing, “well-adjusted people...without hubris or naïveté, routinely fail in life’s important missions by not even attempting them... Khosla himself was an unreasonable man, creatively maladjusted.”

Vinod Khosla is the venture capitalist who backed the startup company, Impossible Foods, that makes the Impossible Burger. (It’s a plant-based burger that has become wildly successful because, unlike earlier veggie burgers, it tastes good.) Although each venture-capital success story is different, Mallaby – the author of The Man Who Knew, a biography of Alan Greenspan that I reviewed here – finds a common thread: All of them involve unreasonable, maladjusted people who are a pain in the neck. Mallaby describes Khosla as “cocky and obnoxious...one part tyrant, two parts visionary.”

Vinod Khosla is the venture capitalist who backed the startup company, Impossible Foods, that makes the Impossible Burger. (It’s a plant-based burger that has become wildly successful because, unlike earlier veggie burgers, it tastes good.) Although each venture-capital success story is different, Mallaby – the author of The Man Who Knew, a biography of Alan Greenspan that I reviewed here – finds a common thread: All of them involve unreasonable, maladjusted people who are a pain in the neck. Mallaby describes Khosla as “cocky and obnoxious...one part tyrant, two parts visionary.”

But Khosla is not the inventor of the Impossible Burger. That’s Patrick Brown, who is even more unreasonable. A celebrated geneticist, Brown wanted to put the meat industry out of business. Most inventors would be satisfied with their product achieving a decent market share and making them rich. Brown wanted to destroy an industry he regarded as harmful and save the world by. Livestock farming takes up one-third of the world’s agricultural capacity; Brown wanted it to disappear.

His dream was that “nobody would eat ground cow flesh again.”

Impossible!

Mallaby’s new book, The Power Law, elegantly shows how these impossible dreams get funded, and then either win big or (much more frequently) lose everything. That is where the power law comes in.

What is the power law?

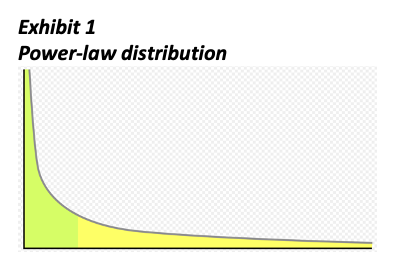

The book’s title, The Power Law, is meaningful to people who work with data but will be a mystery to everyone else. It’s an important concept from statistics, so I’ll start by describing it. Have you ever noticed that the sizes of cities, businesses, and executive paychecks follow a pattern like this?

Cities are the clearest example. You can picture New York, the largest U.S. metropolitan area, at the top of the curve in Exhibit 1. Los Angeles, about two-thirds as large, is farther down. Chicago, about two-thirds as large as Los Angeles, is farther down still – and so on down to the multitude of small cities making up the “long tail” to the right. The word power is thus used in its mathematical sense, that of a “power series” in which each observation equals the previous one multiplied by a constant, called the constant of proportionality. In the cities example, the constant is about two-thirds.

The power law versus the normal distribution

Mallaby compares the power-law distribution to the much more familiar normal distribution. In a normal distribution, outliers don’t matter much. Men’s heights are normally distributed, so if you removed Lebron James from a room of 100 otherwise randomly selected men, their average height would go down by only a fraction of an inch. But wealth follows a power law, so if you take Elon Musk out of a room of 100 randomly selected people, or even rich people, their average wealth plummets.

In a phenomenon that follows a power law, outliers matter tremendously.

The power law and venture capital

What does all this have to do with venture capital? It turns out that the returns on venture capital investments follow a power law. (I am talking about the returns on the companies that are in the VC firms’ portfolios, not the VC funds themselves.) The power, in this case the ratio of the return on the #2 company to that of the #1 (and so on down), is much less than two-thirds. According to Mallaby,

Y Combinator, which backs fledging tech startups, calculated in 2012 that three-quarters of its gains came from just two of the 280 outfits it had bet on. “The biggest secret in venture capital is that the best investment in a successful fund equals or outperforms the entire rest of the fund,” the venture capitalist Peter Thiel has written.

The source of this winner-take-almost-all effect is the fact that, in the venture world, or at least the technology part of it, success leads to more success in an explosive pattern.1 It’s not like the ordinary investment management business where styles such as growth and value run in cycles with the result that, as Charles Gave said, you are “one day a rooster, the next day a feather duster.”2 Mallaby argues that the explosion upward is due to a network effect that you find in the tech sector but only rarely in the rest of the economy:

After the invention of the semiconductor, or after the invention of the Ethernet cables that hooked personal computers together, usage picked up gradually and then exploded upward in an exponential curve; this was the innovation power law that underlay the financial one observed in venture-capital portfolios.

A little later, the internet did something similar, but at an even faster rate, almost vertical.

The mothership

An earlier story reflecting this same phenomenon, which Mallaby recounted with a historian’s attention to detail, is that of Fairchild Semiconductor, the mothership of venture capital, in the late 1950s. It housed a Who’s Who of future tech-company billionaires: Gordon Moore (of Moore’s Law), Robert Noyce, Andy Grove, and Eugene Kleiner who would later establish the iconic VC firm Kleiner Perkins. Arthur Rock, a New York-based broker who would later become one of the world’s great venture capitalists, backed it.

Unsurprisingly, they were all engineers (except Rock, who financed the venture from outside it). Our modern world was built not by statesmen, scientists, or financiers, but by engineers.3

Left to right: Gordon Moore, C. Sheldon Roberts, Eugene Kleiner, Robert Noyce, Victor Grinich, Julius Blank, Jean Hoerni, and Jay Last.

Source

What became of this little group? In 1968, Moore and Noyce founded Intel, for a long time the world’s largest semiconductor manufacturer. “Intel Inside®.” (Manufacturers of parts and ingredients struggle for name recognition even if they are blindingly rich.) Grove became president of Intel in 1979. Eugene Kleiner joined with Tom Perkins, Frank Caufield, and Brook Byers to form what would become the most recognizable name in venture capital investing; Kleiner Perkins dominated Silicon Valley for four decades before its influence started to fade about a decade ago. It funded or co-funded, among hundreds of other companies, Amazon, Genentech, Google, Netscape, Sun Microsystems, and Twitter.4 The impact of the Fairchild “alumni association” on modern life is incalculable.

Flower children versus the Mayflower

Most of the successful startups in the last 40 years have been in the western United States, mostly in northern California. Yet VC as a business concept originated in the Northeast with Laurance Rockefeller, Jock Whitney, Georges Doriot, and others profiled in the early chapters of Tom Nichols’ book VC: An American History, which I reviewed here.5

Why the move to the West? “We owe it all to the hippies,” said the musician-businessman Bono (Paul Hewson). Under the influence of Stewart Brand, author of the Whole Earth Catalog, the freewheeling and nonconformist culture of Bay Area hippies collided with that of inquisitive computer scientists at Stanford and Berkeley in the late 1960s and early 1970s, and a new culture of hackers, tech dreamers, and startup founders emerged.6 I had a job interview with the late Apple executive Jef Raskin in 1977 (I was not selected) and the atmosphere resembled that of a hippie commune.

The east-west schism had taken shape earlier, as the Fairchild crew negotiated with their East Coast bankers. Mallaby recalls:

[Robert] Noyce wanted instinctively to run Fairchild without any divisions between bosses and workers.... [T]here would be a level playing field, a ferocious work ethic, and a belief that every last employee had a stake in the firm.

In [Tom] Wolfe’s telling of this story,7 ...Fairchild Semiconductor’s East Coast overlords...could never fathom this...ethic. [They] had a feudal approach: ...there were kings and lords, and there were vassals and soldiers.

Sequoia Capital’s Don Valentine described the Eastern money men as “people with hyphenated names or Roman numerals after their last name, direct descendants of immigrants who arrived on the Mayflower.” Imagine a group of casually dressed, computer-toting hippies asking them for large sums of money.

It was not a foregone conclusion that the unstructured West would beat the button-down Northeast. But, by the late 1970s, with the founding of Apple in Silicon Valley and Microsoft in Seattle, it did, and Western dominance of venture capital in the United States has only grown stronger since then.

Peter Thiel, Founders Fund, and the power law

Fast forward a couple of decades (Mallaby’s book is long) – past the founding and funding of Microsoft, Apple, Google, and Amazon. It’s 2004 and the venture capital industry is booming, thanks largely to big institutions – university endowment funds, pension funds, charitable foundations – perceiving that private capital, of which VC is a part, offered a better return than the stock or bond markets. Having started a half-century earlier as a rich man’s hobby and then a niche activity in the Boston and San Francisco suburbs, VC has gone mainstream. It’s an industry.

Peter Thiel is an odd duck even by the standards of the VC duck pond. A gay conservative libertarian Republican German American, Thiel annoyed much of the VC community with his kooky projects (life extension and seasteading), lawsuits, and constant political proselytizing.8 He is also brilliant and mega-rich, having co-founded PayPal, set up a hedge fund called Clarium Capital, and founded the security company Palantir. He was the angel investor behind Facebook. He is closely associated with Elon Musk, with whom he is said to have (surprise!) a love-hate relationship.

Having nothing to do (!) and recently emerged from fights with other Silicon Valley bigwigs such as Sequoia Capital’s Michael Moritz, Thiel set up his own venture capital firm, Founders Fund. Mallaby writes,

Having nothing to do (!) and recently emerged from fights with other Silicon Valley bigwigs such as Sequoia Capital’s Michael Moritz, Thiel set up his own venture capital firm, Founders Fund. Mallaby writes,

The name signaled the ethos: founders who had created companies like PayPal were out to back the next entrepreneurial cohort, and they promised to treat this new generation with the respect that they themselves had wished for.

It sounded very groovy, very Californian. It would also become one of the most successful VC firms of the new century.

At the beginning of this article, I quoted Thiel saying that the best investment in a successful fund was often the only one that made any money. Thus, writes Mallaby,

Thiel was the first VC to speak explicitly about the power law. Past venture investors, going back to Arthur Rock, had understood full well that a handful of winners would dominate their performance. But Thiel went further in recognizing this as part of a broader phenomenon.

Because Mallaby’s expansion on this point is the central theme of the book, I quote him at length:

Thiel went further in recognizing this as part of a broader phenomenon.... the “Pareto principle” or 80-20 rule [says] that radically unequal outcomes [are] common in the natural and social world.

Mallaby describes the economist Vilfredo Pareto’s observation, around the turn of the last century, that 80% of the land in Italy was owned by 20% of the people, and that this inequality could be observed in many different contexts. “It was therefore not just a curiosity that a single venture-capital bet could dominate a whole portfolio. It was a sort of natural law,” writes Mallaby. He continues:

Thiel was methodical in thinking through the implications of this insight... He argued, iconoclastically, that venture capitalists should stop mentoring founders... The power law dictated that the companies that mattered would have to be exceptional outliers; ...[t]he founders of these outstanding startups were necessarily so gifted that a bit of VC coaching would barely change their performance.

The most successful companies in the Founders Fund portfolio, a colleague of Thiel’s observed, were often those with which VCs had the least involvement. In Mallaby’s words,

[T]he art of venture capital was to find rough diamonds, not to spend time polishing them... [If] the power law dictated that only a handful of truly original and contrarian startups were destined to succeed, it made no sense to suppress idiosyncrasies...the wackier the better. Entrepreneurs who weren’t oddballs would create businesses that were simply too normal...[and] would have occurred to others.

And that is how the power law – not just the theory of it, but the practice – became the central principle of venture capital investing.

Y Combinator

Y Combinator has the coolest company name in the Valley. It sounds like they are breeding new companies in a biochemistry lab.

The brainchild of Paul Graham, Y Combinator provides the exact same deal to every venture: $500,000 to “accelerate” the growth of the business, regardless of its size and financial condition. (It is not the only accelerator firm.) Over 20,000 companies apply each year, and the acceptance rate is 1.5% to 2%. In a beautiful demonstration of the power law, the rewards to Y Combinator are few and big: “We now have more than 110 companies valued over $100M and more than 25 companies valued over $1B,” according to the company web site. Most of the $500,000 investments are a total loss.

The brainchild of Paul Graham, Y Combinator provides the exact same deal to every venture: $500,000 to “accelerate” the growth of the business, regardless of its size and financial condition. (It is not the only accelerator firm.) Over 20,000 companies apply each year, and the acceptance rate is 1.5% to 2%. In a beautiful demonstration of the power law, the rewards to Y Combinator are few and big: “We now have more than 110 companies valued over $100M and more than 25 companies valued over $1B,” according to the company web site. Most of the $500,000 investments are a total loss.

You could be forgiven for thinking this sounds more like a MacArthur Foundation “genius grant” than an investment. (Y Combinator also gives away money to nonprofits.) Graham would fit in at a foundation or university – he is something of a philosopher whose blog posts are legendary for their intellectual quality.9 But Y Combinator is not a foundation. Graham and his partners care very much about money; they just earn it in a very unconventional way, breaking all the rules of traditional VC investing. They pursue extreme diversification, invest small amounts, take an unusually small stake in the company (7% plus some optionality), and bring the entrepreneurs together in a bootcamp-like atmosphere.

Their try-everything approach gets results. Among Y Combinator’s successful investments were Airbnb, Dropbox, Doordash, and Reddit.

Put enough smart and ambitious people (many of whom are visibly crazy) together in a few hundred square miles of north-central California real estate and you get some unexpected outcomes. Although I’m just guessing, Y Combinator is probably Stewart Brand’s favorite VC.

Uber: Ideas having sex

Uber is one of my favorite companies to write about, because it did almost everything wrong and still succeeded at disrupting one of the most entrenched industries in existence – the taxicab cartel. The company was run by a jerk, broke laws intentionally, and changed the rules on drivers so often as to infuriate half of them. (The other half, who treated the situation as a game to be mastered, did very well.)

Maybe they’re black hats, but without Uber breaking the cartel and creating a free market in rides, we would still be chugging around in taxis that, as George Will wrote in 2003, “were last inspected at Studebaker dealerships and are driven...by strangers driven by strange demons.”10 (I’ve saved that quote for 19 years, waiting to use it.)

Uber’s great innovation wasn’t dynamic pricing (which responds in real time to changes in supply and demand); the airlines had been doing it for decades. It wasn’t the use of mapping and geolocation software to enable drivers and passengers to locate each other. It wasn’t the hiring practices, where drivers could work as many or as few hours as they wanted and have other jobs. The innovation was doing all these at the same time.

Matt Ridley, that brilliant and controversial chronicler of human progress, asserts that new ideas come from old ones having sex.11 It’s a vivid image. Computer + telephone = internet. Horse and carriage + engine = car (with an unemployed horse left over). Uber is a particularly salient example of ideas having sex, with at least three different threads of invention combining to produce the resulting leap in utility.

Why are so many founders and CEOs “not nice”?

While Mallaby does not tell the full story of Uber, he draws a valuable lesson from what he describes as the company “going off the rails.” “Founders Fund made an expensive error,” he continues,

by refusing to invest in...Uber; its bratty founder, Travis Kalanick, had alienated [the fund’s managers]. “We should be more tolerant of founders who seem strange or extreme,” [Peter] Thiel wrote, when Uber had emerged as a grand slam. “Maybe we need to give assholes a second and third chance,” [Founders Fund principal Luke Nosek] conceded contritely.

It’s a lesson I would have preferred not to learn. Founders and CEOs are often not nice. Kalanick fits the mold, which was perfected a long time ago by James H. Patterson, the S.O.B. founder of National Cash Register.12 Mallaby refers to many tech-company leaders as “tyrants”; in addition, Steve Jobs and Bill Gates, heroes to many, have been described similarly. All of us are rooting for businesses to be led by good human beings, but there is something about successful entrepreneurship that is correlated with an aggressive and even bullying personality.

It is probably for the best that Kalanick was replaced by a more responsible and law-abiding CEO. But, without Kalanick’s hardball tactics, Uber would not have gotten a foothold (nor would have Lyft, which hitched a ride on Uber’s earlier aggressiveness). Our travel about town would still be guided by strange demons, and we would still be paying monopoly prices for a service that belongs in the competitive economy.

There’s a broader lesson here: Venture capital and the companies it backs play a vital role in the economy and in the rapid rate of technological progress that we’ve become used to, even when they are not well behaved. Disruption is not pretty.

Conclusion and advice for investors

The Power Law is a story book, a history of the U.S. venture capital industry as told by its people, practices, and products. It is plausible bedtime reading. Despite the mathematical title, the book has no math beyond what I’ve presented and does not rely on data or academic studies. Only a natural storyteller like Mallaby can capture the essential weirdness of many entrepreneurs and venture capitalists. They make hedge fund managers, profiled in Mallaby’s earlier book, More Money than God, look like boring conformists.13

Nor does The Power Law give investment advice, but I will: These stunts are performed by trained professionals – don’t try them at home.

Individual investors and their advisors should avoid venture capital investing entirely. (I might make an exception for those with true inside information about ventures started by people they know personally, as long as the information is legal. Even then, do it in small doses.) The “good” VC funds, the ones like Accel Partners and Founders Fund that see the most attractive startups, are closed to all but a few institutions and families who commit to investing in the funds in good times and bad.14 The not-so-good funds lose money; sadly, those are the ones that investors can gain access to. (Unlike in the public equity market where manager results are more random, there are “good” and “bad” VC funds because the most successful entrepreneurs keep going back to the same firms for more funding, causing yet another explosive process.)

The power law surely contributes to the plight of the average VC fund. Given the pervasiveness of failed startups, it is essential that VC funds get to invest with the few that offer outsized returns. But the structure of the VC industry dictates that those investments are divvied up among the elite firms at the top of the pyramid.

Even though they shouldn’t invest in VC, individual investors will be holding many of these companies in their portfolios once they go public. They will consequently be buying the stocks that entrepreneurs and venture capitalists are selling. Companies founded by entrepreneurs and backed by venture capitalists are the seed corn of our economy. We only get to enjoy the meal once the seeds have been nurtured (or, more often, allowed to die) by the venture capital community, but investors need to understand where new companies come from, and why.

Laurence B. Siegel is the Gary P. Brinson Director of Research at the CFA Institute Research Foundation, the author of Fewer, Richer, Greener: Prospects for Humanity in an Age of Abundance, and an independent consultant. His latest book, Unknown Knowns: On Economics, Investing, Progress, and Folly, contains many articles previously published in Advisor Perspectives. He may be reached at [email protected]. His website is http://www.larrysiegel.org.

1The explosive effect may not be as powerful, or may not exist at all, in other types of venture-funded businesses such as manufacturers and retail stores.

2Personal communication. Charles Gave is a founder of Gavekal Group, an investment research firm. Before that, he ran the investment management firm Cursitor-Eaton.

3William Shockley, the Nobel Prize-winning physicist for whom nearly all of these men worked before launching their venture, was a scientist as well as an engineer (professor of electrical engineering at Stanford). Note that he did not jump aboard the Fairchild Semiconductor train and was almost certainly not asked to; the group just described, known as the Traitorous Eight, seem to have gotten their nickname by joining together in rebellion against Shockley (yet another “tyrant” by Mallaby’s reckoning).

4Genentech, the first major biotech company, doesn’t seem to fit in. But venture investing is about more than what we usually call “technology.” Medicine is technology too, and Genentech (now part of Roche) is where synthetic human insulin comes from – perhaps more important, if you are a diabetic, than any of the other companies.

5Note the old-money pedigree in the Northeast: Rockefeller and Whitney.

6A history of this period is in Markoff, Robert. 2022. Whole Earth: The Many Lives of Stewart Brand. New York: Penguin Random House.

7Wolfe, Tom. 1983. “The Tinkerings of Robert Noyce.” Esquire (December), https://web.stanford.edu/class/e145/2007_fall/materials/noyce.html

8According to seasteading.org, “seasteading means building floating societies with significant political autonomy.” The organization reports having seven active projects, one of which is underwater (intentionally). For Thiel’s writings, see https://thememeticist.com/other/2020/07/28/thiel-online-writing-list.html.

10Will, George F. 2003. With A Happy Eye, But... New York: Free Press, p. 163.

11In The Rational Optimist (2011), which I reviewed here. It was my first review for Advisor Perspectives.

12See Gary Hoover’s description of Patterson, which is so damning it borders on the hilarious, in his Bedtime Business Stories (American Business History Center, 2020). The chapter on Patterson is here. Yet Hoover argues that many of the sales techniques we use all the time were originated by Patterson and were a big improvement over the haphazard methods that came before.

13More Money Than God was reviewed by Michael Edesess here. Edesess did not like the book, asserting that Mallaby had been “captured” by the hedge fund industry.

14Actually in successive funds issued by the same venture capital manager – e.g., Technology Venture Partners Fund I, Fund II, and so forth – but that is a minor detail.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All