The History and Future of Venture Capital Investing

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIs venture capital a good investment? For long periods in the past, the best VC firms had spectacular returns, as their outside investors or “limited partners” – pensions, foundations, endowments, wealthy individuals – participated in the emergence of great companies such as Intel, Microsoft, Apple, and Amazon. But, going forward, can VC investors expect the same returns? Or are we in a new era of lower returns and a more challenging environment?

Innovation and the implementation of new technology, through the support of new businesses, has always been at the heart of economic progress. For centuries, this work was done by wealthy families, monarchs, and governments. But, starting in the mid-twentieth century in the United States, the VC firm, a wholly new type of investment management enterprise, began to seek and use capital from outside investors, as well as by the firm’s owners, to fund and nurture new business ventures.

Learning the history of this transformation helps us discern an answer to the questions I posed at the outset. The Harvard Business School professor, Tom Nicholas, has written a penetrating history of the industry that focuses on the early years and brings the story of VC up to the end of the last century.

By “technology,” of course, I do not just mean computers, rocket ships, or the latest whiz-bang smart-phone app. I mean whatever makes it possible to do more with less: railroads and telecommunications in the 1800s, the fruits of electrification in the early 1900s, the automobile and airplane shortly thereafter, and the thousands of lesser innovations that added up to a highly productive economy instead of a survival-based one. Nicholas fully appreciates this economist’s definition of “technology,” and shows how venture-oriented investors have helped to fund and shape all kinds of technological innovations throughout modern history.

(Don’t) save the whales

If they don’t study the past, leaders of businesses cannot begin to understand the future in which they will be operating. While no one can predict the future with accuracy, students of business history find that there are patterns that repeat, over and over, shedding light on today’s challenges. The Harvard professor Tom Nicholas’ book on venture capital, VC: An American History, reaches far back in time and into activities that are alien to us to find such patterns:

[N]ineteenth century whaling can be compared to modern venture capital... [W]haling was the archetypical skewed-distribution business, sustained by highly lucrative but low-probability payoff events... The long-tailed distribution of profits held the same allure for funders of whaling voyages as it does for a venture capital industry reliant on extreme returns from a very small subset of investments. Although other industries across history, such as gold exploration and oil wildcatting, have been characterized by long-tail outcomes, no industry gets quite as close as whaling does to matching the organization and distribution of returns associated with the VC sector.

That’s a good start (and he has rate-of-return data for whaling!). Too often, business authors who are keen on history look back only a generation or two – or a century at most – to learn lessons of the past that they can apply to the future. I’m more impressed by parallels over very long periods of time, which identify aspects of business that don’t go away. For example, the desire to manage risk is universal. Thales of Miletus, who lived from 624 to 545 BCE, a century and a half before Socrates, invented the options market. He created a technology for hedging the price of olive oil that we still use today.

Nicholas doesn’t reach quite that far back. His tale starts in the early days of the United States, as it should in order to keep the book length manageable and readers engaged. I’ll briefly recount Nicholas’ journey through history, then offer some opinions on what is good and what’s less good about the book. But, as I’ve long maintained, one needs a thorough understanding of “deep history” to capture the elements of human nature and collective action that don’t change much in principle over time, although they change profoundly in implementation. To understand this deep history, I’d refer readers to the works of Peter Bernstein and William Goetzmann, who have chronicled finance, including venture capital, all the way back to ancient times.1

Before accompanying Nicholas on his journey, let’s ask why venture capital has become so important, and why serious study of the industry is revealing.

A venture capital world

We live in a venture capital world. All of the six U.S. “hot stocks” of the current decade – Facebook, Apple, Netflix, Microsoft, Amazon, and Google, which form the acronym FANMAG – were venture-backed.2 Tesla and Uber are also pretty hot stuff, despite struggling to make a profit, and they, too, are funded by venture capitalists.

But it was not always thus. Most of the great corporations of the past – and many of the present – were financed through organic growth (retained earnings), accretion (mergers and rollups), bank lending, government funding, and stock and bond issuance. Venture capital, as an industry and not a rich men’s hobby, only begins with the founding of American Research and Development Corporation in 1946 by, among others, Georges Doriot, a Harvard Business School professor often considered the father of organized venture capitalism. That is not so long ago in the history of American industry, and mirrors the emergence of other modern business institutions – the captive research institute and the consulting firm – that characterized the postwar period.3

There was life (and money) in venture capital way before Doriot. While Nicholas could be forgiven for skipping ahead to the post-World War II period and the rise of institutional venture capital in the U.S., he’s a historian and doesn’t go for the easy path. Instead, Nicholas skips backward to 1783 and the funding of the Industrial Revolution, specifically the spinning jenny.

On whales and long tails

But first, let’s finish the whale story. It’s so good it deserves more detail, and the comparison of venture capital to whaling is the thread that ties Nicholas’ story together.

The extreme financial risk associated with whaling ventures is not typical of the way that most businesses invest and grow. If a chain of hardware stores decides to open a new branch, it is not guaranteed to succeed, but it is not likely to harpoon (sorry) the whole business if it fails. The same applies to Toyota or Ford launching a new line of cars and trucks: it is a calculated risk that is more likely to succeed than fail.

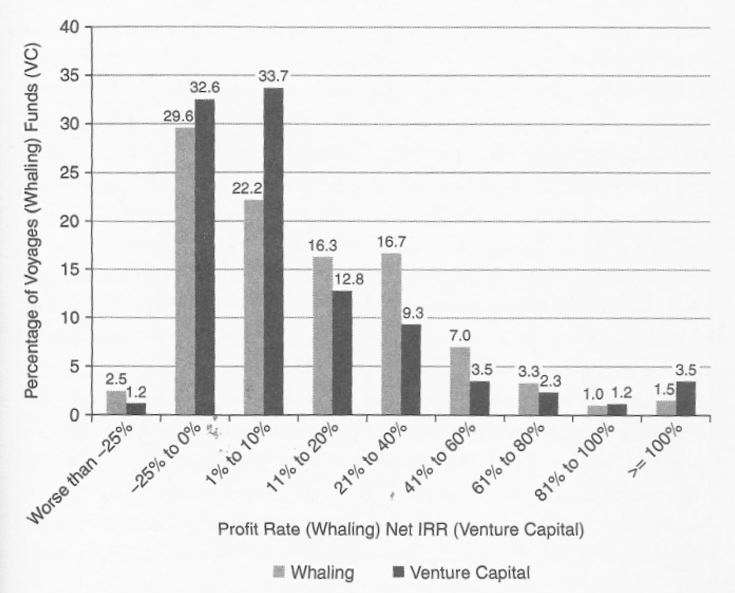

Whaling, gold exploration, and oil wildcatting are the opposite: they are more likely to fail than succeed, but the successes – at least in expectation – are so large that they more than make up for the failures. So far, the parallel is close, at least on paper. Exhibit 1, from Nicholas’ book, compares returns of the top 29 whaling ventures to returns, almost two centuries later, of the top 29 venture capital funds.

Exhibit 1

Returns on top whaling ventures and venture capital funds

Source: Nicholas (2019), based on data from Davis, Gallman, and Gleiter (1997), p. 250, and from Preqin.4

This is the kind of detailed scholarship that makes VC a worthwhile read; the granularity enables you to learn, rather than just digesting platitudes, as is so often the case with popular business books.

But what distinguishes whaling from modern venture capital is the risk taken by the entrepreneur. Failed whaling ventures often resulted in the sailors being drowned or, in the awful case of the whaling ship Essex, which was launched in 1799 and sank in 1820, eaten. (The voyage of the Essex was the inspiration for Herman Melville’s Moby-Dick.) It is said that 50% of sailors (not just whalers) who went to sea in the pre-modern era died on the job. That’s why elevated outdoor walkways on old East Coast houses are called widow’s walks.

Failed tech entrepreneurs, in contrast, merely have to start another business or, in extremis, get a job.

Financing the Industrial Revolution

High-tech cotton

A generation before the age of the great whaling ships, a remarkable invention – the spinning jenny – “allowed spinners to multiply their labor, deepening the use of capital in the economy,” Nicholas writes. Using a traditional spinning wheel, a spinner could produce only one spool of yarn at a time, but the jenny quickly made it possible to spin 12 at a time, and “incremental advances would further multiply the output of a single operator to...as many as 120.”

That is a huge increase in productivity in a short time, bolstering Nicholas’ claim that the cotton industry was not the low-tech activity we now tend to think it is, but the leading edge of late-18th century technology, and part of what launched the British and American economies into the self-sustaining growth they would enjoy in the next two centuries. This technological change also, of course, destroyed many jobs as it created others; and, just as importantly, made cotton goods much cheaper so that it took less labor to afford them. This parallels the wrenching – yet, on net, beneficial – changes we are experiencing through the Internet, artificial intelligence and other technological advances.

Developing a new technology is not free, and Nicholas chronicles the proto-venture-capital deals that supported the development of the spinning jenny. The backers unsurprisingly included whaling families, because they were rich but also because they were accustomed to the idea of taking risk. In a series of appendices, Nicholas reprints the terms of the deals between backers and entrepreneurs, dated in the 1780s, that resemble, at least in their gross structure, similar deals that are concluded today. (The use of lawyers was much more sparing back then, so the agreements are quite short and readable.)

Development of the railroads and modern industry

The laying of the railroads, which began a half-century later, was one of the most massive infrastructure projects in the history of the world and required government financing as well as venture capital backing. Still later, the building of America’s great industrial corporations required a comparable blizzard of capital-raising, in which Andrew Mellon and J. P. Morgan were among the key figures on the capital provision side. Nicholas compares Mellon’s approach to modern VC practices:

Richard Florida and Mark Samber argue that Mellon’s activities “mirror those of contemporary venture capitalists in many respects, by providing both financial resources and management assistance.” ...First, while Mellon engaged in debt financing...he soon adapted his style to also include equity involvement and thereby long-tail returns. He engaged in equity participation across a portfolio of early stage ventures, often in new high-tech industries...[such as an efficient method of aluminum refining, which had eluded metallurgists for two millennia].5

The annus mirabilis of 1946, and beyond

Corporations and informal networks of wealthy industrialists provided the bulk of venture-capital financing through the rest of the Second Industrial Revolution (roughly 1870-1940). But things were about to change as World War II came to an end. The bridge to the modern VC era was built by a half-dozen men who came to prominence right after the war. Here, I’ll focus on one of the best known, John Hay Whitney, known as Jock Whitney.

Jock Whitney, the Renaissance man of venture capital6

A wealthy jack-of-all-trades and scion of a highly accomplished family, Whitney was, with Benno Schmidt,7 the founder of J. H. Whitney & Co., which is widely considered the first venture capital firm (as opposed to private investor). In fact, the duo may have coined the phrase “venture capital.” The reporter Gabe Kleinman writes that the firm “initially position[ed] itself as ‘a lender of “private adventure capital” ’— and legend has it, Schmidt abbreviated this to ‘venture capital’ so it would roll off the tongue more easily.”8 Nicholas dissents, saying the term was already in use.

Kleinman adds that “[m]odern philanthropy and private equity have the same parents: the Wallenbergs, Vanderbilts, Whitneys, Rockefellers, and Warburgs.” Of this august crowd, Whitney was distinguished by his making a proper business out of it. He built an infrastructure that enabled J. H. Whitney & Co. to help its portfolio companies grow, improve their management practices, and achieve a successful exit. “By 1958,” Nicholas writes, “Whitney had thirteen partners whose experience spanned business, law, finance, and academia, and twenty additional support staff to help with investment due diligence.” It was the prototype of the modern venture capital firm, except for the raising of capital from institutional investors, which we’ll get to in a moment. J. H. Whitney & Co.’s first investment was Spencer Chemical, which “represented an archetypal VC investment because a single portfolio company returned the entire value of the fund,” writes Nicholas.

Kleinman adds that “[m]odern philanthropy and private equity have the same parents: the Wallenbergs, Vanderbilts, Whitneys, Rockefellers, and Warburgs.” Of this august crowd, Whitney was distinguished by his making a proper business out of it. He built an infrastructure that enabled J. H. Whitney & Co. to help its portfolio companies grow, improve their management practices, and achieve a successful exit. “By 1958,” Nicholas writes, “Whitney had thirteen partners whose experience spanned business, law, finance, and academia, and twenty additional support staff to help with investment due diligence.” It was the prototype of the modern venture capital firm, except for the raising of capital from institutional investors, which we’ll get to in a moment. J. H. Whitney & Co.’s first investment was Spencer Chemical, which “represented an archetypal VC investment because a single portfolio company returned the entire value of the fund,” writes Nicholas.

Between horsemanship, boating, serving as president of the Museum of Modern Art, amassing one of the world’s great personal art collections, representing the United States at the Court of St. James’s, co-authoring a song with Fred Astaire,9 and romancing movie stars and marrying Betsey Cushing, the former daughter-in-law of Franklin D. Roosevelt, it’s hard to see how Whitney had time to run a company at all. But that is often what successful people are like. They have more energy than they know what to do with.

Georges Doriot and American Research and Development

The other key figures in the postwar VC boom were Laurance Rockefeller and Georges Doriot, the latter having helped to establish American Research and Development (ARD) in 1946. That year was the annus mirabilis (“wonderful year”) of venture capital, when all three of the best-known early firms – Whitney, ARD, and the Rockefeller Brothers Fund – were founded. Nicholas presents a table listing the seven VC firms established in 1946 and four more between 1947 and 1951.

Doriot differed from the others in coming from academia rather than inherited wealth. He was a Harvard Business School professor. His great innovation was to take the existing venture tradition, created by wealthy families, and make an institutional investment product out of it. ARD raised funds from foundations, university endowments, and eventually pension funds as their legal authority and practical ability to invest in alternative assets grew over time. Eventually – in 1966 – the general public could invest, when ARD converted itself to a publicly traded closed-end fund.

ARD’s big win was its 1957 investment in Digital Equipment Corporation, launching the marriage between the VC community and the computer industry. Nicholas quotes Doriot as saying that “we gave the man [who founded Digital] $70,000...and today we value that investment at $52 million.”

Nicholas gives a lot of airtime to ARD and Doriot, because of the firm’s importance to the history of VC, without admiring him personally. He was not a nice man: he mistreated his employees, was overcautious in an enterprise where risk-taking is of the essence, and did not like women in business. And, although Doriot is usually given credit for founding ARD, the engineer and banker Ralph Flanders was the real founder. Flanders was appointed Senator from Vermont shortly afterward and handed the controls to Doriot.

Private enterprise versus government

Nicholas uses the story of ARD to launch an account of the rivalry, starting with the 1953 act by Congress that made Small Business Investment Companies (SBICs) possible, between business and government in capturing the opportunity from emerging businesses. “It was not clear that venture capital could be supplied by market mechanisms alone,” Nicholas writes. He shows, however, that the government-backed SBICs were often undercapitalized, had trouble attracting management talent, and consequently provided poor returns to investors. But the cloud had a very large silver lining:

...SBICs created an entry point for talented startup investors who would later engage in the [VC] industry. One example is Sutter Hill Ventures, a Palo Alto VC firm created by William Draper III and Paul Wythes in 1964 out of two SBICs.... Sutter Hill...sent on to generate annualized returns of 37% from 1970 to 2000.

That is a cumulative return of 12,636 times your money, assuming the 37% is a compound annual rate of return and not an arithmetic mean. With Sutter Hill, the Silicon Valley gold rush (an appropriate metaphor given the firm’s name) had begun in earnest. Off to the races!

Tom Perkins and the golden valley

The southwestern corner of the San Francisco Bay basin is called the Santa Clara Valley. Few Californians today know that: they call it Silicon Valley, even though no silicon is mined or processed there and very little is used in manufacturing computers or other devices, which are built elsewhere; the Valley’s main product is software and data. But it’s still called Silicon Valley because, between about 1970 and 2000, the period when Sutter Hill made a great fortune, it was the world capital of the computer industry.

A wealthy kingdom must have a king, and Silicon Valley is probably the wealthiest kingdom in the world. For a generation its king was not Steve Jobs or any other entrepreneur but Tom Perkins, the best-known partner and public face of the VC firm of Kleiner, Perkins, Caufield & Byers. Just as merchants once petitioned the king for contracts and loans, entrepreneurs preferentially sought out Kleiner Perkins funding, because the venture firm provided not only a rich lode but, arguably, better management assistance than anyone else. And funding by Kleiner Perkins was perceived as a “Good Housekeeping Seal of Approval” that encouraged investment by other VCs and the trust of potential customers.

A wealthy kingdom must have a king, and Silicon Valley is probably the wealthiest kingdom in the world. For a generation its king was not Steve Jobs or any other entrepreneur but Tom Perkins, the best-known partner and public face of the VC firm of Kleiner, Perkins, Caufield & Byers. Just as merchants once petitioned the king for contracts and loans, entrepreneurs preferentially sought out Kleiner Perkins funding, because the venture firm provided not only a rich lode but, arguably, better management assistance than anyone else. And funding by Kleiner Perkins was perceived as a “Good Housekeeping Seal of Approval” that encouraged investment by other VCs and the trust of potential customers.

The firm funded, among many other companies, AirBnB, Amazon, America Online, Compaq, Coursera, Genentech, Google, Intuit, Lotus Development, Netscape, Spotify, Sun Microsystems, and Uber. Of course, following the modern VC model, most or all of these companies were funded by multiple VC firms, not just one as in the prewar days.

The kingship has since passed to John Doerr, current president of Kleiner Perkins (and the dominance of that firm has waned somewhat) but, in a business history book, the story of a founding partner is usually more compelling than that of a successor.

Like Jock Whitney and many other VC leaders, Tom Perkins was known as a “character.” The reporter John Wilson, in The New Venturers, had him starting out in the 1940s as “a science-struck kid always tinkering with Tesla coils and ham radio equipment” only to be transformed, forty years later, into a “charismatic corporate gamesman...[who] with his actor’s looks and unruly mop of hair barely flecked with gray...[has] more the air of a yachtsman than a financier.”10 He was respected but not exactly loved, with Nicholas describing him as having a “dominant” persona that could drift into “moments of complete derangement,” but those are traits often associated with mega-successful executives. And Perkins admitted that he founded a company – University Laboratories – just to run a company he did not like, his former employer Optics Technology, into the ground.

Perhaps it takes a colorful personality to bet other people’s money, along with a very good chunk of one’s own, on speculations that are as risky as early 19th-century whaling ventures. But beneath the bravado and panache of the leaders, the staff typically performs assiduous feats of due diligence to minimize that risk and concentrate their bets on potential winners. They do not put their finger in the air and invest. Despite all that effort, modern VC firms, like those in olden days, still lose much more often than they win, and often rely on very successful single investments to produce a positive return on the overall fund.

Participatory management: A new VC investment style

Perkins changed the VC industry by devising a new investment “style.” Nicholas characterizes the styles existing at the time as follows:

There were essentially three types of venture investors at the time – east coast firms such as ARD (in its twilight years), Greylock, and [the Rockefellers’] Venrock, which were steeped in old money; west coast entities like Davis & Rock and Sutter Hill; and individuals who acted like modern-day angel investors.

What Perkins did differently was to “provid[e] a more systematic approach to seed capital deployment and governance in high-technology industries.” This was described as “a new style of participatory, value-added investment.”

While this sounds like a subtle difference, it’s not. Today’s VC industry is dominated by the Perkins model, in which the venture capitalist is an active management partner, not a silent partner whose role is mostly restricted to providing funding.

The success of the Perkins model is part of what led to the gradual drift of VC’s center of gravity from Boston to the West Coast. Active participation in the management of companies in the VC investor’s portfolio simply turned out to be a better strategy. In addition, the more freewheeling general approach to business found on the West Coast was a better match for the pace of the technological explosion that was taking place.

Bubble, bubble, toil and trouble

This trend would persist into the twenty-first century, with the flourishing of Google and many other companies in its orbit. Nicholas’ long chapter, “The Big Bubble,” covers the familiar period in the late 1990s when venture-backed companies helped drive the stock market to record valuations and then crashed even more quickly than they had risen.

But, as the author Peter Bernstein reminded us at the time, bubbles followed by crashes leave a legacy of new technology that does not go away when the stock prices go down. Bubbles can thus be a marker of progress, not failure. “Hurrah for bubbles,” Bernstein wrote.11

What Nicholas does not do is to bring the story up to date. The recent (twenty-first century) history of VC is in large part a continuation of the model that made the 1990s productive and exciting, albeit with different kinds of companies and products such as social networking and artificial intelligence. Perhaps Nicholas will cover this period in a forthcoming book.

Recommendations for readers

VC: An American History could have been written as popular history or popular science, which in my mind are terms of respect: the highest calling of the non-fiction writer is to educate the public. But it’s not popular history. It is, instead, a serious work of scholarship. It’s also a heavy book, both physically (almost 400 pages) and in the density of the writing, thinking, and data presentation. That will be a positive for some readers and a negative for others. Very much on the plus side, VC is not a compendium of case studies, unlike many books written by Harvard Business School professors. Thank goodness! That hand has been overplayed.

The twenty-first century, in which venture capital plays such an important part, is mostly left out of Nicholas’s story. He may believe that the recent history already well known and that the older stories are not. That is an understandable position to take, but on net it’s a weakness of the book. If Nicholas eventually writes a book about this most recent period, I’d most certainly like to read it.

Venture capital has become a central feature of our economy, and of those outside the United States, particularly in China, which last year represented an astonishing 30% of global VC market capitalization. We would do well to understand this business, which operates beyond the view of most citizens and even some skilled investors. Tom Nicholas’ book provides the needed historical background. It is not for everyone, but if you’re one of the intellectually curious who are drawn to business history, I enthusiastically recommend it.

Looking to the future

Venture capital is now a mature industry flooded with talented and ambitious people. It is no longer the frontier, but part of the mainstream. VC won’t get another king like Whitney or Perkins, but it doesn’t need one. It is a craft, and does not require geniuses to perform the work. In contrast, the entrepreneurs funded by VC firms still have to be pretty exceptional.

We in the investment management business flatter ourselves if we think that alpha can only be produced, in Cliff Asness’ sardonic description, by a “crazed genius” who generously shares his natural gift with a few lucky investors. Alpha production, whether in public markets, hedge funds (which is what Asness was talking about), or venture capital, mostly results from a combination of hard work, good timing, and luck.

Tom Nicholas does not attempt a forecast of future returns from VC, but the lessons of history learned by reading his book show that the conditions for spectacular returns from VC do not now exist. Consider the following:

- There is plenty of money – a flood, some would say – chasing the available deals.

- We are in a technological pause, where improvements are marginal rather than revolutionary. This concern is less serious in biotech and artificial intelligence (AI) than it is in computing and telephony. However, while biotech and AI are advancing quickly, their commercial payoffs tend to be both far in the future and uncertain.

- The past success of VC has drawn in a lot of high-priced talent from other fields, including the tech firms themselves, other types of private equity firms, consulting firms, academia, and firms that manage publicly traded assets. This imposes a high cost structure on VC firms and makes it hard to retain key people, who now work in an environment that favors the talented employee, not the limited partner (investor) or even the general partner.

Thus, current conditions do not resemble the environment chronicled by Nicholas, when lean organizations led by charismatic adventurers could make outsized returns. Be cautious about future capital commitments to VC, especially if you cannot access the very best firms.

When it comes to venture capital, those who fail to learn its history are more likely to earn poor returns.

Larry Siegel is the Gary P. Brinson Director of Research for the CFA Research Foundation and an independent consultant. Prior to that, he was director of research in the investment division of the Ford Foundation. His book, Fewer, Richer, Greener will be published by Wiley in 2019. He may be reached at [email protected] and his web site.

1 Bernstein, Peter L. 1996. Against the Gods: The Remarkable Story of Risk. Hoboken, NJ: John Wiley & Sons. Goetzmann, William N. 2016. Money Changes Everything: How Finance Made Civilization Possible. Princeton, NJ: Princeton University Press.

2 FANMAG is my own creation, and it’s better than FANG or FAANG. Microsoft should be considered venture backed even though it only had funding from one venture capitalist (Technology Venture Investors).

3 The first captive research institute was probably Bell Laboratories, founded quite a bit earlier (1925), but we always find antecedents when we look for them; the big corporate push into research and development was postwar. General Electric’s NELA Park in East Cleveland, Ohio was research-oriented but started as a competitor to GE and was acquired in 1911, so it does not exactly fit the mold of a captive corporate research facility.

4 Davis, Lance E., Robert E. Gallman, and Karin Gleiter. 1997. “Whales and Whaling.” In Davis, Gallman, and Gleiter, eds., In Pursuit of Leviathan: Technology, Institutions, Productivity, and Profits in American Whaling, 1816-1906, pp. 20-56. Chicago: University of Chicago Press.

5 The ancient Romans knew how to extract aluminum from bauxite but it was impossibly difficult and expensive. The problem was not solved until Carl Josef Bayer invented the modern process, still in us, in 1887. We take much technological knowledge for granted.

6 In one of those six-degrees-of-separation stories that I couldn’t make up, through an odd combination of circumstances I’m at two degrees of remove from Jock Whitney, two from Franklin D. Roosevelt, and five from Abraham Lincoln.

My old boss, Franklin Thomas, who was president of the Ford Foundation from 1979 to 1996, asked me to do some investment consulting for his life partner, Kate Whitney, and her sister Sara Whitney, who control the Greentree Foundation in Long Island, New York. The Whitney sisters are Jock Whitney’s adoptive daughters and are also Franklin D. Roosevelt’s granddaughters. (FDR’s son James Roosevelt and his wife Betsey Cushing were Kate’s and Sara’s biological parents. After the younger Roosevelts divorced, Cushing married Jock Whitney, who adopted Kate and Sara.)

Jock (John Hay) Whitney’s grandfather was John Hay, Abraham Lincoln’s personal assistant, who also served in cabinet or ambassadorial positions under four subsequent presidents.

7 Not the former president of Yale, but his father.

8 Kleinman, Gabe. 2017. “Why Aren’t Foundations Actually Helping Their Grantees Like VCs?” Medium (Nov 14), https://medium.com/newco/why-arent-foundations-actually-helping-their-grantees-like-vcs-77d4437648

9 “Tappin’ the Time.” The lyrics are credited to the prolific Gladys Shelley and dated 1936, but according to Kathleen Riley, a biographer of Astaire and his wife, they were authored by Whitney and Jimmy Altemus much earlier, and, Riley writes, “the number was used in the 1927 London revue Shake Your Feet.” Riley, Kathleen. 2012. The Astaires: Fred & Adele. Oxford, UK: Oxford University Press.

10 Wilson, John W. 1985. The New Venturers: Inside the High-Stakes World of Venture Capital. Reading, MA: Addison-Wesley.

11 This comment is from an issue of Bernstein’s privately circulated market commentary, Economics and Portfolio Strategy (Peter L. Bernstein, Inc., New York).

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits