Avocado toast, hard seltzers, and Instagrammable vacations are not the reasons millennials and our Gen Z compatriots have failed to scrimp, save and budget our way into home ownership.

I've long been an ardent defender of renting and I stand behind the sentiment that it doesn’t equate to throwing your money away. Still, the chaotic rental market of recent years has made buying seem like the practical move, even in cities with a high cost of living, at least from a logistics and emotional turmoil perspective. The problem is that prospective homebuyers across the country are facing a housing shortage, are frequently boxed out in bidding wars, and have watched their purchasing power erode as mortgage rates surge.

Millennials have little choice but to compromise — either by giving up on homeownership or facing the reality of being able to afford less than what’s desirable.

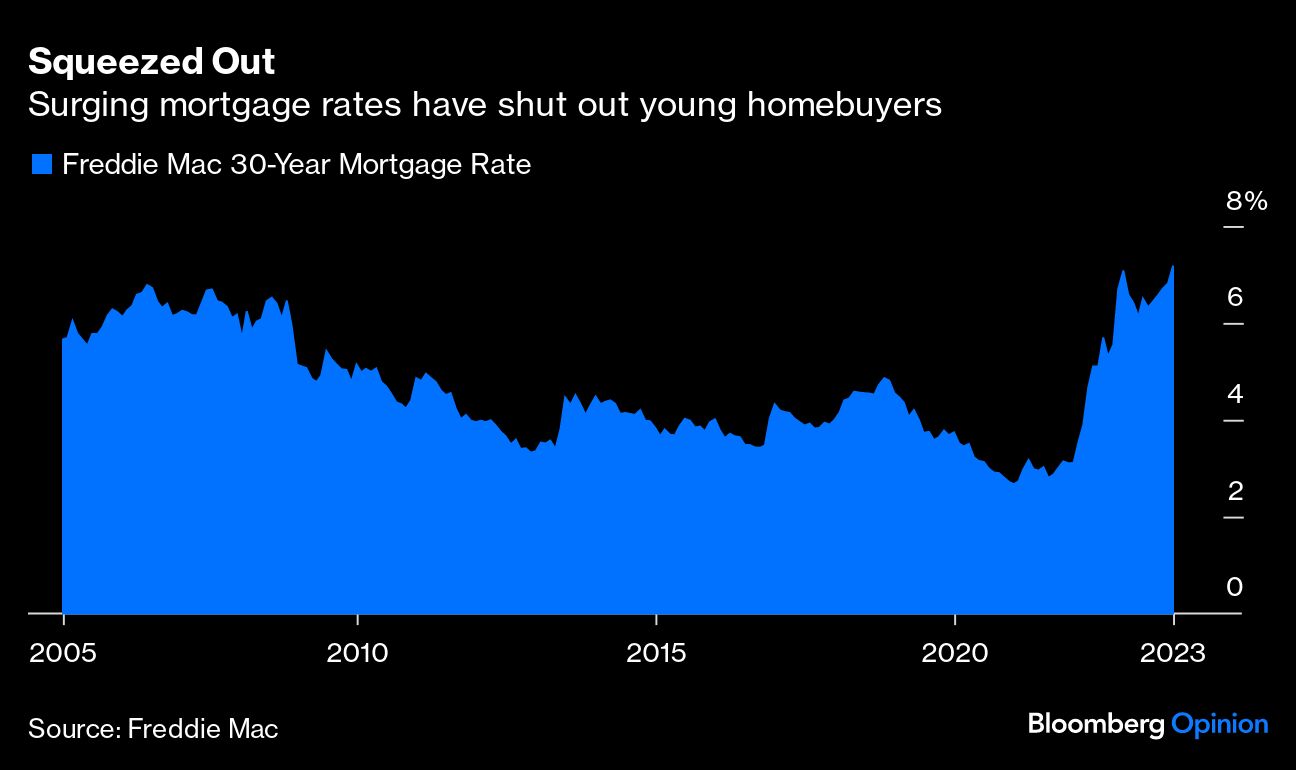

Millennials have only known low mortgage rates, anchoring our expectations about what’s reasonable to an unrealistically low number compared to previous generations. In 2009, when the oldest millennials started thinking about homeownership, the mortgage rate was around 5.4%. It stayed under 5% for the next decade before the pandemic drop to under 3%. Now, we’re creeping toward double-digit rates for the first time since the early nineties.

Those who missed the opportunity to buy have lost tens of thousands of dollars in purchasing power since late 2022. Their frustration is compounded by the fact that homes prices continue to increase because housing inventory has dropped dramatically since the pandemic.

The median sales price of a new single-family home in June was $415,400. In August 2022, a potential buyer could afford a $416,500 home with a $2,500 monthly payment on a mortgage at 5.5%, according to real estate brokerage Redfin Corp. Today, that same buyer can afford an approximately $368,750 house with a mortgage rate of 7% (and climbing).

Yes, we know, double-digit mortgage rates were the norm for many boomers who bought in their thirties, but affordability is not remotely the same, even after adjusting for inflation.

The median sales price of a house in the final quarter of 1985 was $86,800, amounting today to approximately $245,000, which is roughly what the median home cost back in 2012. Today’s homebuyers must shell out roughly 70% more than in 1985 adjusted for inflation. Wages haven’t kept pace either. The most recent census data puts median household income in the US at $70,784 in 2021. It was $23,618 at the start of 1985, which equates to about $68,434 today. Taken together, the cost of a home has gone from about 3.5 times income to nearly six times.

In this situation, how much of your salary should go toward housing? Financial planners would advise keeping costs below 28% of gross monthly income, meaning you’d need to earn six figures to purchase a home worth $416,500 with 20% down and a mortgage payment of roughly $2,500.

With a gross annual income of $90,000, you could afford a $2,100 monthly payment (or a little more since it makes sense to stretch that 28% a bit if your mortgage lender allows). But 20% down on a $416,500 house means almost a full year of income. You layer in student loans, an auto loan, and just generally living life and it’s no wonder people struggle to be competitive in this housing market.

Inventory blues and purchasing power woes aside, millennials need to be willing to make compromises if we’re going to join the ranks of homeowners.

One option is waiting. Bloomberg Opinion columnist Conor Sen wrote recently that the economy may slow enough in the first half of next year to push mortgage rates lower. However, waiting can seem risky since it could take years for a more optimal environment to emerge for buyers.

The most frustrating option, particularly for those who delayed buying their first home until their mid-thirties, is that you may not be skipping the smaller starter home that you’ll soon outgrow. Perhaps you envisioned four bedrooms, three baths, and ample room for children (or dogs) to run around and a 10-minute drive to work.

Instead, if homeownership is an important cornerstone to your financial (and mental) health, and a good investment in your area, it might be time to adjust the Zillow filters to what’s within your budget, even if that means a townhouse or fewer bedrooms and bathrooms, instead of your midnight fantasy scrolling. Alternatively, you can be creative and buy a multi-generational home with a family member or a duplex that you partly rent out.

Home ownership may be positioned as a stepping stone to being a full-fledged grownup but doing what’s in your financial interest must supersede societal and familial pressure. You can keep scrolling Zillow for that dream home that’s magically within your budget and won’t be scooped out from under you. Or you can take a beat, squeeze in another Instagrammable vacation, eat that avocado toast guilt-free, and fact-check your boomer uncle the next time he brings up double-digit mortgage rates.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.