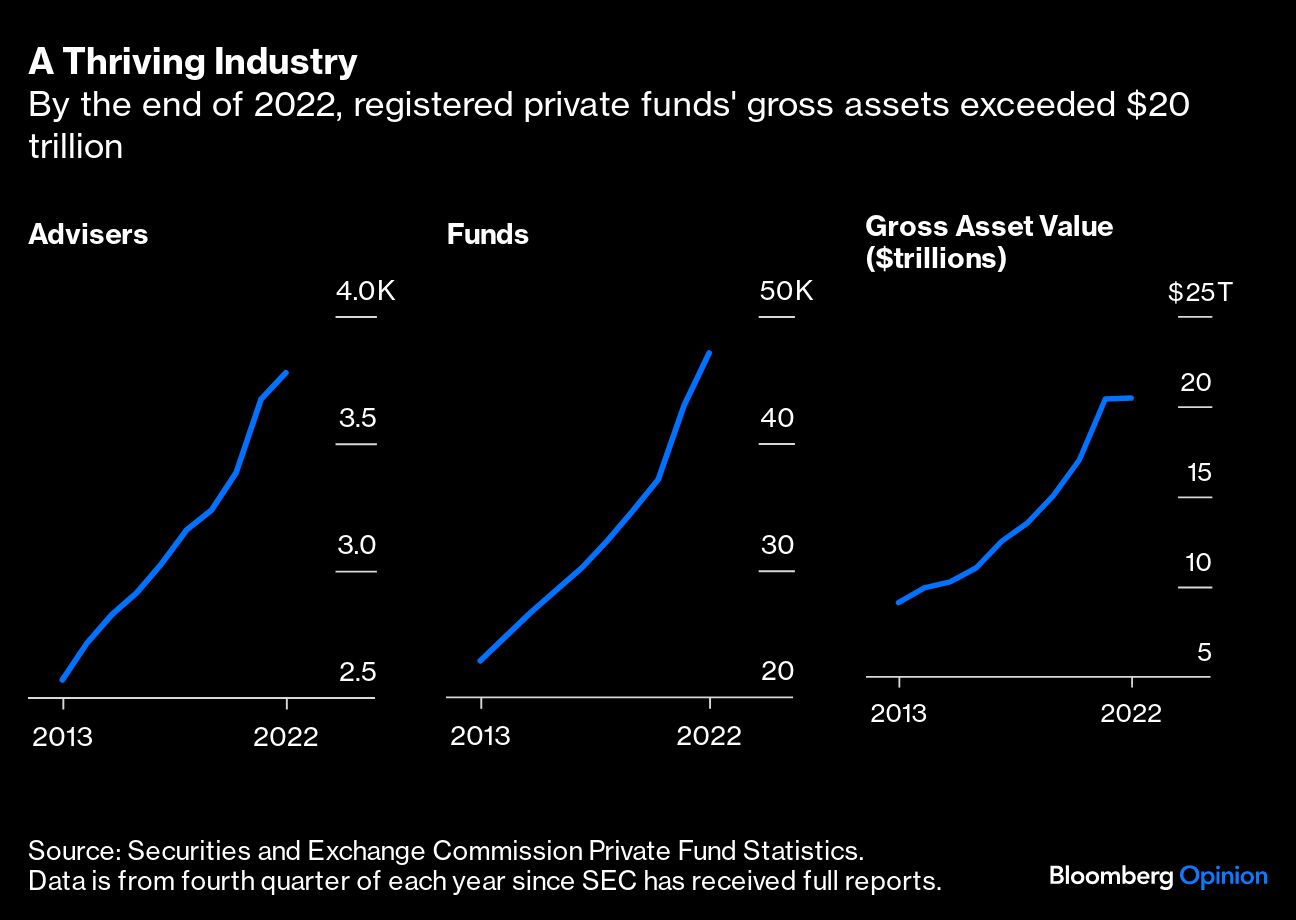

If a teacher, electrician or autoworker buys a stock or a share in a mutual fund, the Securities and Exchange Commission aims to ensure they’re investing on a level playing field. But if their pension funds put money in a private equity or hedge fund, regulators have largely stayed out of it. After all, the thinking went, sophisticated investors should be able to look out for themselves.

So it was a historic shift when the SEC voted last month to step into such negotiations. The commission mandated that private funds give investors standardized quarterly reports on fees and performance, along with annual audits. It also prohibited funds from giving some investors information or redemption rights that would put others at an economic disadvantage unless the terms are disclosed and offered to all investors. In effect, such changes would be upending a business model that has persisted for decades.

Six trade groups for the fund industry have sued, challenging the SEC’s right to take such action and alleging the new rule will cause unnecessary harm to investors. They argue that the SEC is breaking new ground in interpreting its mandate, a step that Congress likely did not intend and that would amount to a significant expansion of the commission’s power. They also say that the rules will undermine their business by effectively prohibiting customized arrangements with investors and imposing mountains of needless paperwork.

Although some added transparency for investors may be helpful, on balance the industry’s objections are reasonable. The SEC itself concedes that the new rules will require at least 3.7 million compliance hours and $5.4 billion in added expenses each year. That will be a boon to the largest funds, as added red tape imposes a bigger burden on smaller competitors. It will also mean higher fees and lower returns for investors — all those teachers, electricians and autoworkers — as the costs are simply passed along.