Investment bankers were finally starting to believe in the green shoots of capital-markets activity this month, but the Federal Reserve might now have crushed them under hawkish boots.

After a dire 18 months or so for deals and financing activity, September has brought a promising burst, particularly for new stock market listings and leveraged loan sales, both of which require decent appetite among investors to buy into riskier assets.

Trouble is, investor attitudes could be knocked by the message delivered by the Fed along with its decision to hold interest rates steady at Wednesday’s meeting. Chairman Jerome Powell wants to convince the market that more rises could still come, while a majority of board members favor another hike before the year-end. This could stoke uncertainty in the minds of investors and company executives, which will make them more likely to hit pause on new deals or big strategic decisions.

US stocks wobbled after the Fed meeting, with the S&P 500 ending down on the day. But worse, the big initial public offerings that hit the market in the past 10 days are dropping back to earth despite big opening day rallies. UK chipmaker Arm Holdings Plc jumped 25% in its debut last week but fell below its listing price on Thursday. Instacart (listed as Maplebear Inc.) rose more than 12% in its debut Tuesday, but has given up most of those gains. A third new listing, marketing technology Klaviyo Inc., was up more than 9% on its debut Wednesday but also slipped on Thursday. Further weakness in these stocks could discourage companies preparing listings, such as German sandal maker Birkenstock.

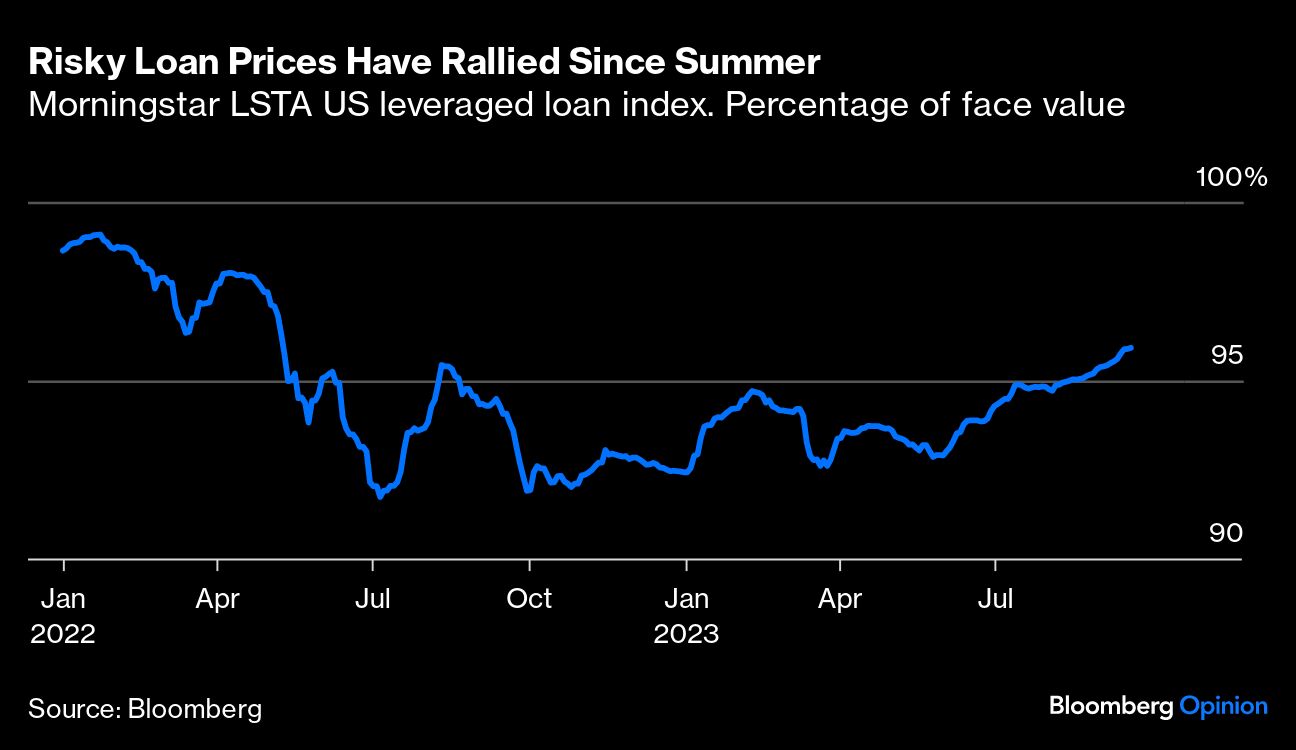

Another key market to watch is leveraged loans, the junk-rated debt typically used to fund private equity deals. It has been boosted by a big pick-up in investor demand and a strong rally in the secondary market since summer after a long moribund spell. Little more than a year ago, banks were taking hefty losses on loans they couldn’t sell. But a wave of successful transactions will encourage dealmakers to press ahead with merger and acquisition plans.

On Wednesday, Goldman Sachs Group Inc. and JPMorgan Chase & Co. led the sale of nearly $10 billion in loans and bonds for Worldpay Inc., which is being spun off by Fidelity National Information Services Inc. What’s more, the dollar portion of the loans was increased to $5.2 billion from $3 billion and its interest rate was reduced during the marketing process, which allowed GTCR, the fund manager buying a majority stake in Worldpay, to cut back the equity it’s investing in the deal.

Last week, Restaurant Brands International Inc. sold the biggest loan in more than 18 months after increasing its deal size and scrapping a planned bond issue. Syneos Health Inc. is another to have closed an enlarged loan sale.

Bankers say that loan and share sales could pick up even with rates remaining high, so long as investors believe that central banks have finished hiking. A reasonable amount of certainty on interest rates allows executives, private equity firms and investors to be confident in their costs of debt and the longer term returns.

What could really boost activity, though, is an idea that rates will fall. Stock market listings, especially, could get a big boost from an expectation of rate cuts ahead, according to equity strategists at Morgan Stanley. Since 2009, capital markets activity has taken off when rates have peaked or seen the first cut, according to a study published this week by Edward Stanley and Matias Ovrum, strategists at the bank. That is directly opposite to the pattern that held between 1998 and 2008, when activity picked up as rates started to rise. The early signs are that the characteristics seen since 2009 are holding, for now anyway, they wrote.

Powell and the Fed are worried that cutting rates again too early could repeat the mistakes of the 1970s: Reigniting inflation even as growth slows. Higher-for-longer was the message, but most of the market hasn’t changed its view that rates will start to decline early next year. If that’s the case, bankers can look forward to a much busier 2024 even if deal-making and fundraising stutter a bit over the next few months.

However, one of their own keeps putting a damper on this view. JPMorgan Chief Executive Officer Jamie Dimon has said in a string of recent appearances that high government spending, mountainous public debt and dangerous geopolitics make a tighter monetary policy and nasty surprises more likely than most people currently think. In six months’ time, inflation might still be at 4% and not dropping, leading to further unexpected rate hikes, he said at an event in Detroit Wednesday.

Dimon admits this is a minority view. Personally, I suspect he’s right.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul Davies