Banks are never fans of tougher regulation, but they really don’t like the overhaul of US capital rules proposed at the end of July by the Federal Reserve and other finance authorities. Lenders and their lobbyists have come out fighting.

It’s not just the potential costs or extra capital demands they hate: There is plenty of negotiating room around those. They also claim a lack of analytical justification for the changes, that some rules are incoherent and that regulators are overriding Congress.

The Fed’s vice-chair for supervision, Michael Barr, is going to be sucked into a deeply political battle over the rule changes, especially as they are due to be finalized in the middle of a presidential election year. Worse, at July’s vote two Fed board members sharply opposed the plan and even Chair Jerome Powell, appeared to express reservations, as the finance industry keenly highlights.

The headlines from the overhaul were that the biggest banks could see the amount of equity capital they need in their balance sheets rise by nearly 20%, while midsize banks could need 10% more. But JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon revealed last week that he expects to need 25% more capital, while David Solomon, Goldman Sachs Group Inc. CEO, forecast marginally more than that. Banks will make more detailed protests in letters to regulators due by November 30.

These are extremely unlikely to be the final numbers. Regulators’ demands often start high and settle for less. That would allow Barr to seem reasonable toward business interests while somewhat appeasing Democrats like Elizabeth Warren, a big voice on financial services. But even if banks had to hit those targets, they would have no trouble getting there: Bank of America Corp., which sees a 20% uplift as the worst likely outcome for itself, could add the capital it requires within two quarters without affecting its dividends.

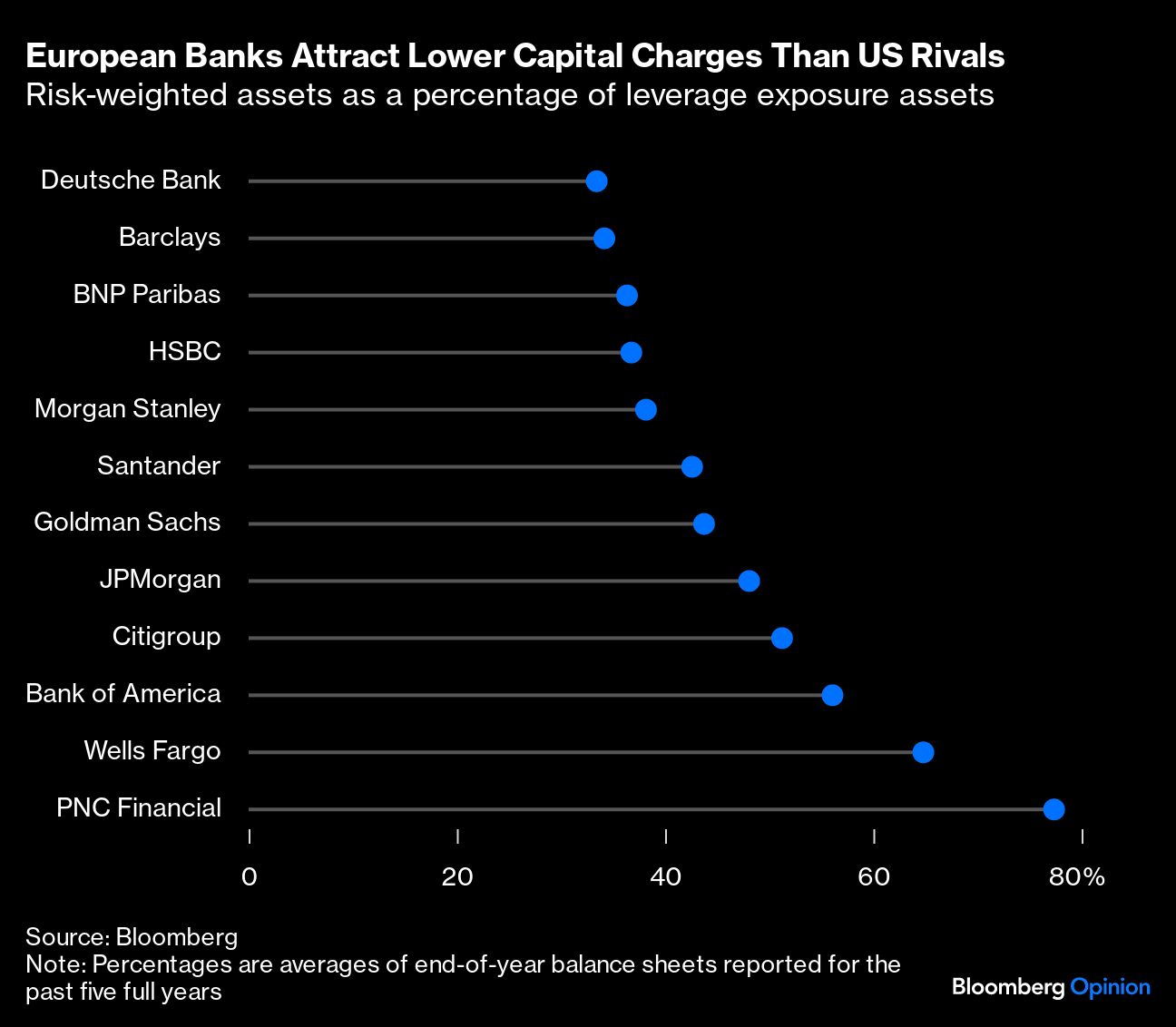

European bank investors will struggle to feel much sympathy. While many lenders there struggle to beat their cost of capital, most big American banks produce good returns and hand out billions of dollars’ of share buybacks and dividends every year. And they too face rising capital demands: Barclays Plc, BNP Paribas SA and Deutsche Bank AG expect their requirements to grow by 5%-10% under UK and European versions of the rules.

In the US, banks are concerned about future profits: A 20% increase in capital means a 20% cut in returns on that capital, all else being equal. JPMorgan, for example, could see long-term returns on tangible equity cut from about 17% to about 14%.

But all else is never equal: Banks constantly adjust pricing and activity to reflect changes in demand or funding costs, for instance, as well as capital rules. The US has the deepest and most active financial markets in the world and its banks have real pricing power, which is why American banks consistently perform better than Europeans. Two examples: Fees for initial public offerings in the US are about double the rate as in Europe; US credit-card issuers still get to charge healthy transaction fees that have been all but eradicated by regulators in Europe.

One big argument from opponents to US rule changes is that they will mean higher borrowing costs or less lending, or a bit of both, particularly for higher-risk mortgages and finance for smaller businesses. This was Powell’s reservation, while Dimon in typically punchy comments last week said the message from regulators was that almost all lending is bad. One of the biggest complaints from industry is that rulemakers have published no cost-benefit analysis of how higher capital would affect lending and the economy. Barr’s arguments would be stronger if it had.

The industry does have good arguments against some of the changes. For example, risks linked to trading in markets and to operational failings, such as IT malfunctions or fraud, appear to be double counted in capital and stress tests as the proposal stands. That seems unnecessary.

On mortgages, the changes aim to level the playing field between big banks and the rest by significantly increasing capital requirements for the former, rather than reducing them for the latter, which would have left US banks closer to European standards.

Worries about international competitiveness are overblown in my view. They mostly matter in capital markets where American banks dominate and have done for years. European banks also expect their regulators to match US capital rules for trading desks. American banks might already have more capital than Europeans, but that is likely due to differences in the kinds of loans they keep on their balance sheets as much as to the standards.

However, the biggest political fight is going to be over regional banks. These got a lighter touch regime from a bipartisan act of Congress in 2018: The Economic Growth, Regulatory Relief, and Consumer Protection Act. This created the two-tier system that let lenders like Silicon Valley Bank operate with fewer guardrails. The Fed’s proposal would force smaller banks to meet the same standards as the biggest. Lobbyists and many politicians, especially Republicans, see this as rulemakers overstepping their authority and in effect repealing an act of Congress.

Barr is going to struggle to get this proposal through as it is — especially without his own board’s backing. The overhaul is happening not because of SVB, but because the Fed needs to bring its rules into line with the final version of global standards that the US agreed with regulators from around the world in 2017. With a few tweaks, a deal with the big banks seems achievable. But true to America’s long history of a fragmented banking system, getting a deal done for regional bank reform will likely prove much, much harder.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul Davies