A seemingly insatiable demand for cash is rippling through markets.

Everyone — from moms and pops to corporate treasurers and the mega asset managers — is piling in, won over by a unique opportunity: To lock in a 5% yield, and protect themselves from uncertainty over the US economy.

With rates on cash and cash-like instruments at the highest in more than two decades and offering more income than benchmark US debt or stocks, assets in money-market funds have swelled to a record. But nowhere is that appetite for liquid, high-yielding instruments more apparent than in the market for T-bills where investors have snapped up more than $1 trillion of new notes in just the last three months.

“These are attractive yields so it never made much sense for bills to be stuffed with the dealers for long,” said Thomas Simons, senior economist at Jefferies LLC. “It has taken a long time for retail investors to pay attention to bills, and the same motivation is there for institutional investors too.”

Demand has been so robust, the amount of bills sitting on balance sheets of primary dealers, the first port of call for Treasury debt sales, plummeted to about $45 billion last month after touching an all-time high of $116 billion in July. It has also made the paper more expensive, driving the difference between bill yields and so-called overnight index swaps — which investors use to measure the Fed’s path — back toward zero after climbing into positive territory for the first time since 2020.

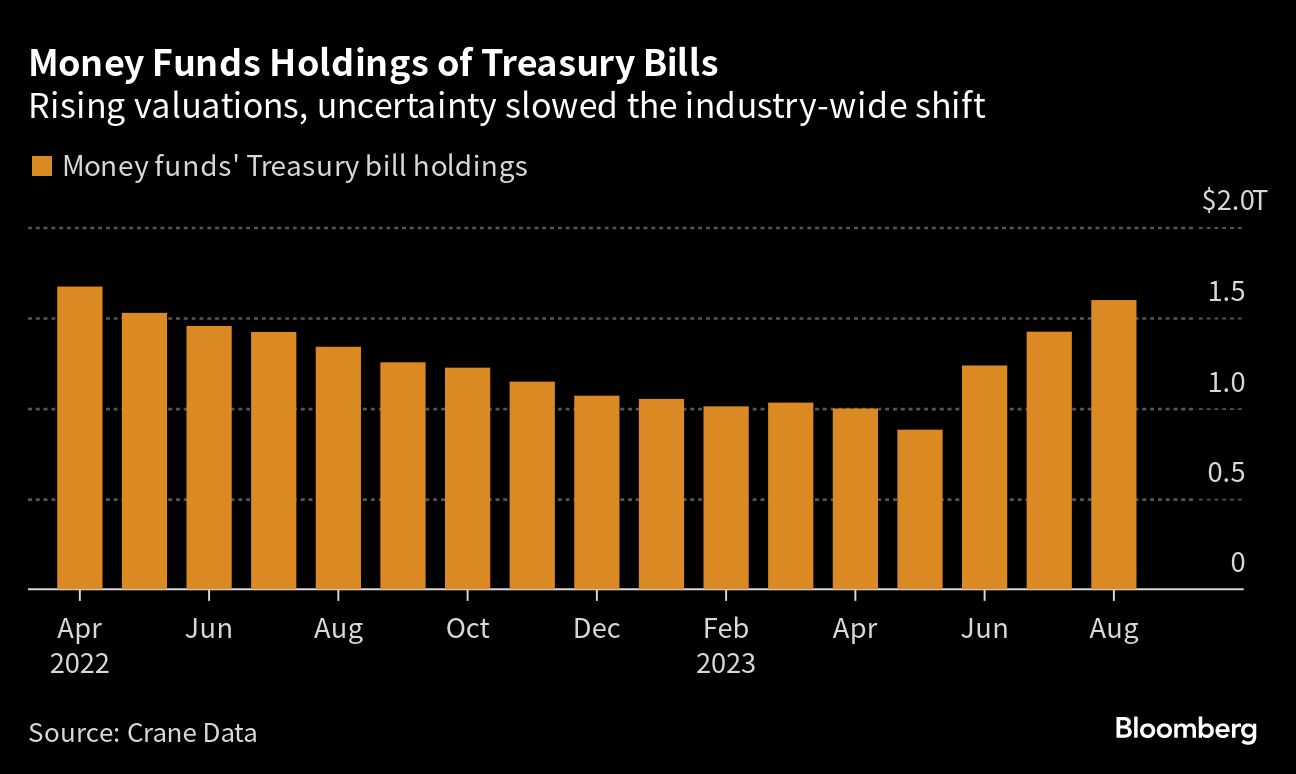

The narrowing trend has prompted some money-market funds that aren’t required to buy only T-bills taking a more cautious view as they await better entry levels and more clarity on the economy and Fed’s policy path.

With US central bank officials entering a quiet period ahead of their policy meeting Sept. 19-20, the monthly inflation report Wednesday will be closely watched for clues to how much still needs to be done to rein in price growth. While there’s little expectation of a hike this month, swaps traders are pricing in about even odds of a quarter-point increase in November.

Cash-like instruments had been perceived as an attractive investment before the 2008 financial crisis led the Fed to slash interest rates and hold them at zero for nearly a decade. Now, after another bout of near-zero rates during the pandemic, the Fed’s historic ramp-up in rates has yields for risk-free assets like T-bills relative to what one can earn at banks once again a worthwhile place to invest excess funds. Below is a ‘who’s who’ guide to the buyers flooding into bills.

Retail Investors

Shortly after the beginning of the year, benchmark Treasury bill yields topped 5% for the first time since 2008. This realization led retail investors to dust off their TreasuryDirect accounts and start buying short-dated securities instead of letting cash linger in bank accounts earning little to no interest.

That jump in demand is seen in government’s weekly auctions, where noncompetitive bidders, which tend to be smaller investors that want to passively accept the yield without the risk of submitting a competitive bid, took a record $2.898 billion of six-month bills in mid-August at 5.29%, matching the highest since 2001 reached in May. The total take-up was about five-fold above levels before the Fed started hiking rates in March 2022.

Corporate Treasurers

When interest rates were near zero, corporations were parking more cash at banks because there was little alternative. Once the Fed started aggressively raising rates, companies moved that cash — often regarded as non-operational deposits for its tendency to chase higher yields — to money funds, which were passing on rate hikes to investors faster than financial institutions.

Now it seems corporate treasurers have been buying bills directly from the Treasury to lock in higher yields. JPMorgan Chase & Co. noted cash and cash equivalents for S&P 500 non-financial companies rose to 62% of aggregate cash portfolios as of the second quarter, from 58% in the same period in 2022. That’s just below the 63% reached in early 2020, only this time there’s no crisis, strategists led by Teresa Ho wrote in a weekly note.

Moreover, the three largest corporate cash portfolios — Apple Inc., Google parent Alphabet Inc. and Microsoft Corp. — showed a “notable increase” in commercial paper, as well as short-dated US government securities captured under cash equivalents, and a corresponding drop in holdings of longer-dated securities, according to JPMorgan.

“Treasury professionals are looking to capture that little more yield than they have before,” said Tom Hunt, director of Treasury services and payments at the Association for Financial Professionals, an industry group for corporate treasurers. “If you’re a bigger shop, companies with a lot of cash on hand, they have investment arms that are actively in the market and buying.”

Asset Managers

Asset managers have several reasons for piling into Treasury bills. For some, like John McClain, a portfolio manager for Brandywine Global, which has $54 billion in assets under management, valuations of risk assets ranging from investment-grade and high-yield debt to equities are too expensive.

“You’re being paid to be patient and there’s a very compelling opportunity to allocate excess cash into T-bills,” McClain said. “The earnings yield on the S&P 500 is below T-bills and that doesn’t happen very frequently. There’s a lot of compelling reasons why you’re supposed to invest in T-bills at the moment.”

In order for portfolio managers to recycle back into risk assets, McClain said credit spreads need to widen relative to bill yields, and the S&P 500 drop by 10% drop. A 20% slide would make it a more compelling buy, he added.

On the fixed-income side, those that were long duration — betting on Treasury yields to fall over time — were recently wiped out following Fitch Ratings’ downgrade of US debt, the resilience of the economy and the glut of bond sales leading to greater concerns about the country’s mounting deficits. That chased fixed-income investors into the very short end.

Jason Pride, director of investment strategy and research at Glenmede, which has $42 billion under management, said the firm is overweight fixed income, heavily weighted cash and short duration in that space because “if you own cash you collect a nice decent yield with very little upside or downside.”

“It’s a weird scenario in that you have a very favorable upside/downside capture in cash,” he said, adding there’s “a more normal to slightly unfavorable scenario going out the curve.”

Money Funds

Despite the rush into T-bills, more than $880 billion has flowed into the money-market industry this year, bringing the total to an all-time high of $5.62 trillion as investors park cash in higher-yielding, liquid instruments amid uncertainty over the direction of Fed tightening.

Balances could top $6 trillion by the end of the year as there’s still more cash from investors to flow into the space, especially once the market begins pricing in more Fed rate cuts, Debbie Cunningham, chief investment officer for global liquidity markets at Federated Hermes, said at the Crane’s Money Fund Symposium in June.

That bodes well as a backup source of financing the government’s ongoing flood of short-term notes. For now, funds that don’t have to buy short-term government debt are on the sidelines, according to John Tobin at Dreyfus Cash Investment Strategies.

These funds are opting to remain at the Fed and in the overnight funding markets until yields rise meaningfully above the offering rate on the reverse repo facility — currently 5.30% — or there’s more direction from the US central bank. Yet Tobin is optimistic that T-bills will start to cheapen as the government issues the last chunk of supply for 2023, which Wall Street estimates at $600 billion, because other investors have finished buying T-bills out the curve so there’s “time before it reappears.”

“We are champing at the bit to add duration here, to get ready to hedge against potential rate cuts but that has to come at a not very expensive price,” the chief investment officer said. “The industry for the most part is refusing to buy at these levels.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recentwhite papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.