UBS Group AG faced two big questions about its emergency rescue of Credit Suisse Group AG: How much profit would it make on the bargain deal? And would the distractions or taint of taking over the failing bank hurt its own business?

Its second-quarter results Wednesday should leave shareholders very happy on both points. The headline net profit of $29 billion for the three-month period ensures UBS has more than enough capital for its enlarged balance sheet, while strong wealth management inflows and a decent performance in investment banking showed UBS kept its people focused on their day jobs.

There are still gaps to fill in the numbers once UBS has done more business planning and negotiated with regulators over capital. But Chief Executive Officer Sergio Ermotti was confident enough to dangle the possibility of a swift resumption of share buybacks, with firmer news due in early 2024 at full-year results.

Of course, that makes the episode more galling for Credit Suisse’s erstwhile shareholders and holders of $17 billion of junior bonds that were wiped out, but Ermotti led with his defense on Wednesday’s earnings call. Credit Suisse didn’t simply have a funding problem sparked by depositor panic in March, he said, but a deeply flawed business model and a severely damaged reputation. Its revenue and costs were heading in the wrong direction, and it was set to report ongoing losses.

The suggestion is that it would keep losing capital, and there was little chance anyone would step up to replenish the pot – in other words, failure of some kind was ultimately inevitable. That’s a strong opinion, but it might not be wrong.

Back to the numbers: The headline quarterly profit is a world record for any bank, but that’s a fairly meaningless benchmark. That $29 billion is almost entirely the gain UBS made on the difference between what it paid for Credit Suisse and the target’s net asset value. All of that profit needs to be retained as capital to support the $238 billion of risk-weighted assets that Credit Suisse adds to UBS’s balance sheet. Buying a bank isn’t like buying a widget maker: A gain like this isn’t money that can be handed to investors.

As big as it was, the return was less than expected. UBS booked further cuts in the fair value of Credit Suisse assets, and there was a bigger second-quarter operating loss at the failing lender, too. The smaller gain means a lesser rise in tangible book value per share than expected, although it is still 49% higher at 24.6 cents, versus a share price of 26.5 cents at midday in London.

But there’s also a big positive in these Credit Suisse asset markdowns. UBS previously said about half of the value lost on loans and other positions would be recovered as they matured. On Wednesday, it said that $12.5 billion out of a total $14.7 billion in markdowns would be recovered over time. On top of that, the benefits of these recoveries would pay for UBS’s restructuring and integration costs as it offloads unwanted Credit Suisse staff, buildings, systems and so on.

The main cuts will come in Credit Suisse’s investment banking and markets business. About two-thirds of that unit’s balance sheet has been put into a bad bank to be run down along with all of Credit Suisse’s existing non-core assets.

In total, UBS starts with $55 billion of risk-weighted assets in this bad bank, and that will shrink by about half by the end of 2026 simply through loans or other positions reaching maturity. That natural runoff will release about $4 billion of capital, although this is counterbalanced by UBS amortizing $5 billion of capital relief it has been given by regulators on mainly Swiss mortgages it has acquired.

In revenue terms, it is almost pointless trying to compare Credit Suisse’s investment bank with previous quarters – there have been too many restructurings, exits and asset markdowns. However, in the loosest terms, it continued to do very badly. UBS views the parts it is keeping as almost a free hit: There are good people and if they can perform well, great; if not, then it will look again at their worth in the future.

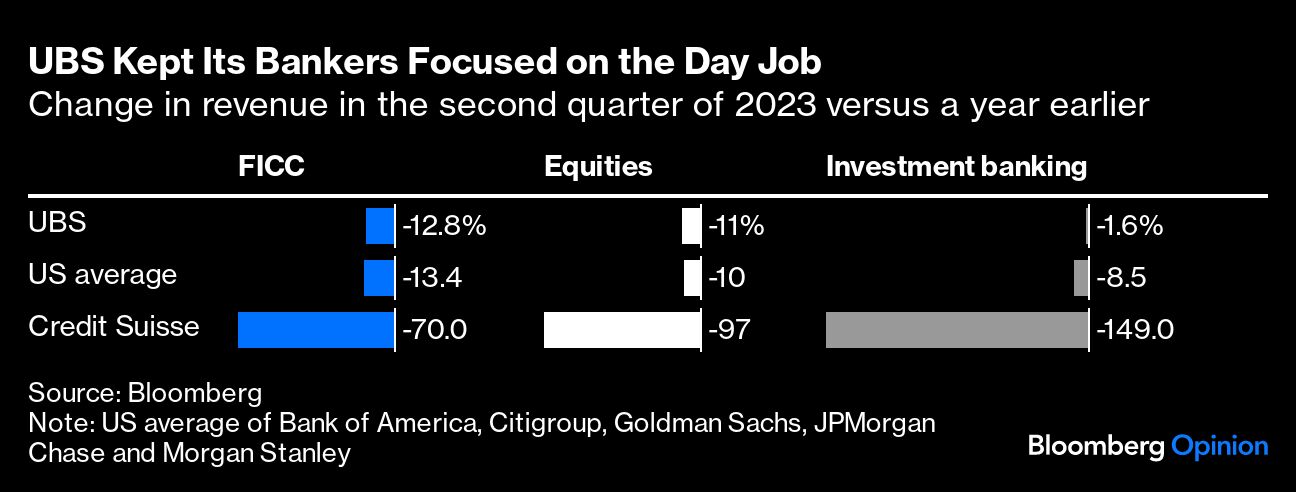

UBS’s own investment bank and markets business held up well in what has been a tough year. In fixed income and equities trading, UBS’s revenue fell, but more or less in line with the average for big US peers. In advisory work on deals and fundraisings, UBS was down far less than US counterparts.

Perhaps the biggest positive was that wealth clients and Swiss depositors showed no nerves over UBS taking charge of Credit Suisse. Net new money in wealth was $16.2 billion, the strongest second-quarter inflows in a decade, while deposits rose slightly from the first quarter. Even Credit Suisse got net new deposits of almost $34 billion across its wealth-management unit and domestic bank over the second quarter and third quarter to date.

UBS’s rescue has brought stability and looks likely to become very profitable for its investors. The better the deal looks, the more political blowback it could still face, but so far Ermotti and the rest of the leadership look like they have played themselves into a winning hand.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul Davies