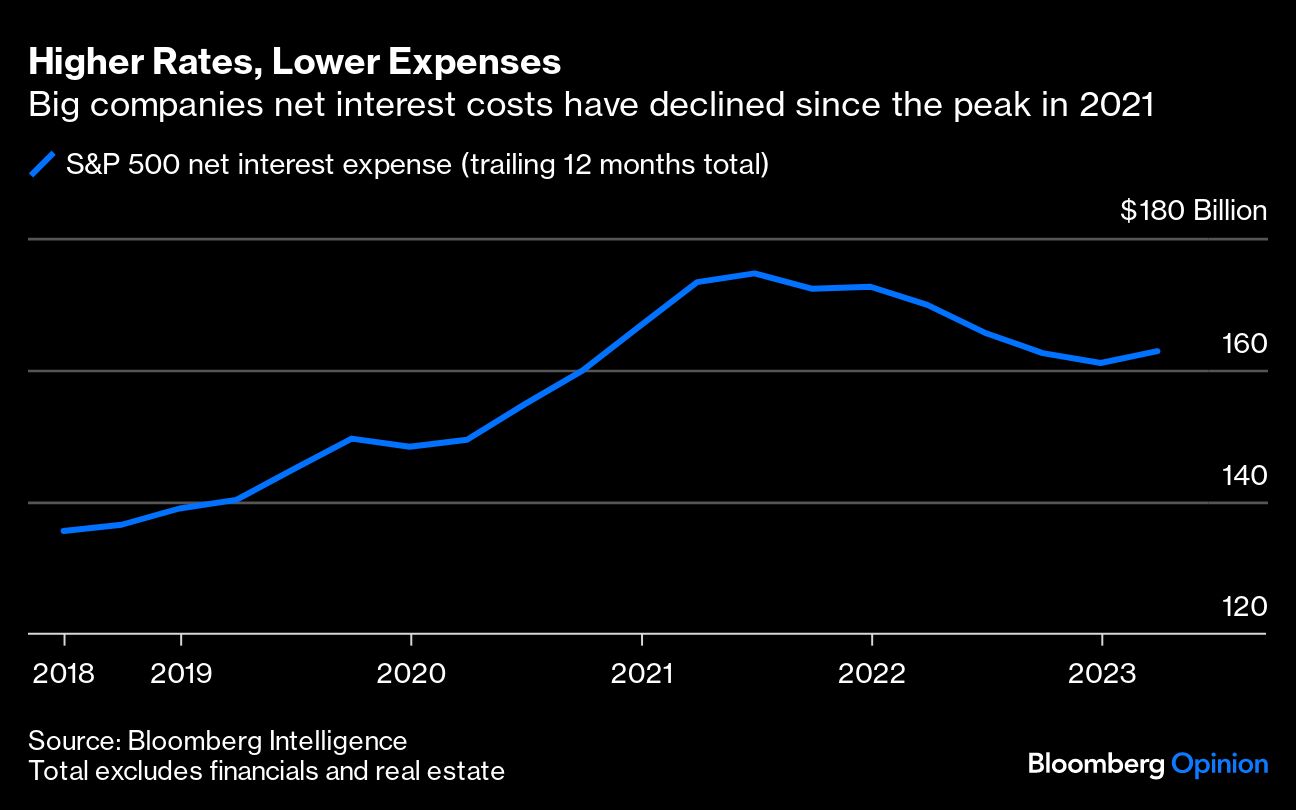

Until recently, I thought rising interest rates were — on balance — bad for businesses. In fact, many big companies are benefiting from the fastest rate-hiking cycle in decades, at least in purely financial terms.

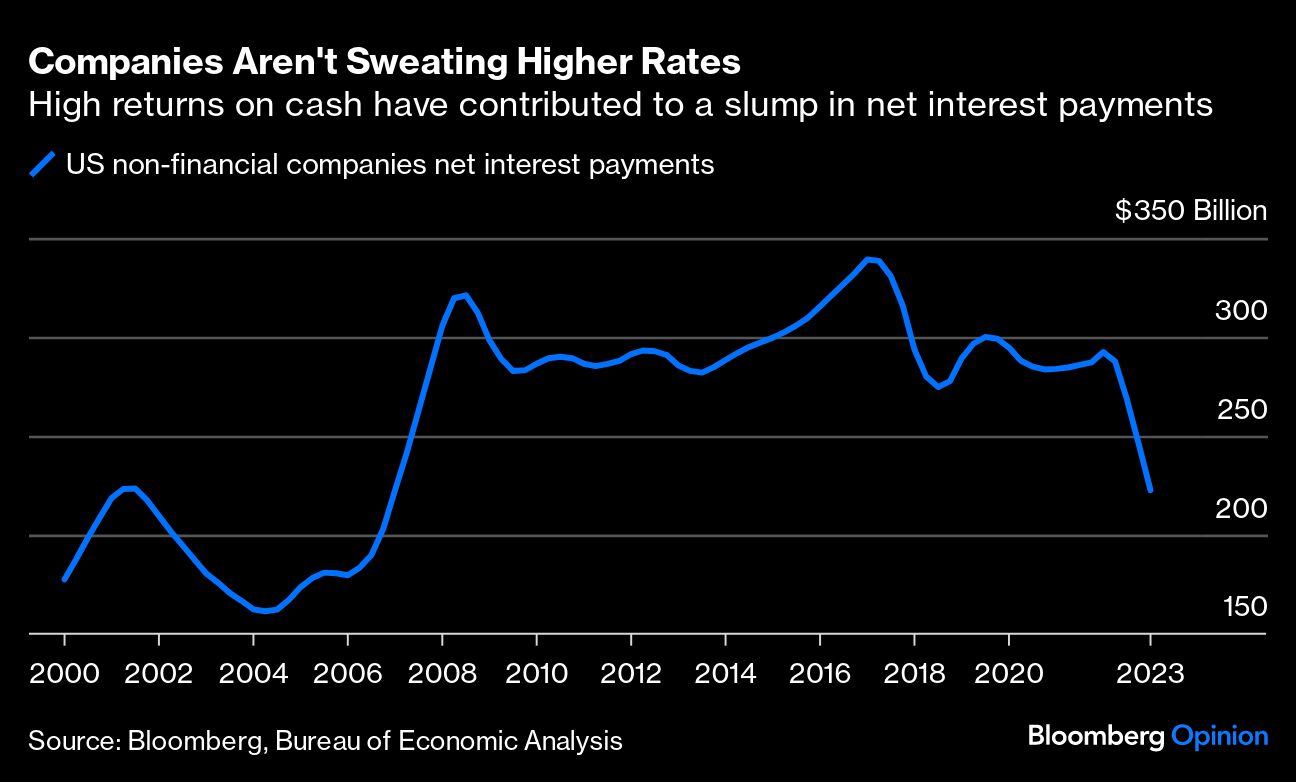

Their combined net interest expenses – interest payments on borrowings adjusted for the interest received on cash and cash-like investments – have declined since the Federal Reserve began tightening monetary policy early last year.

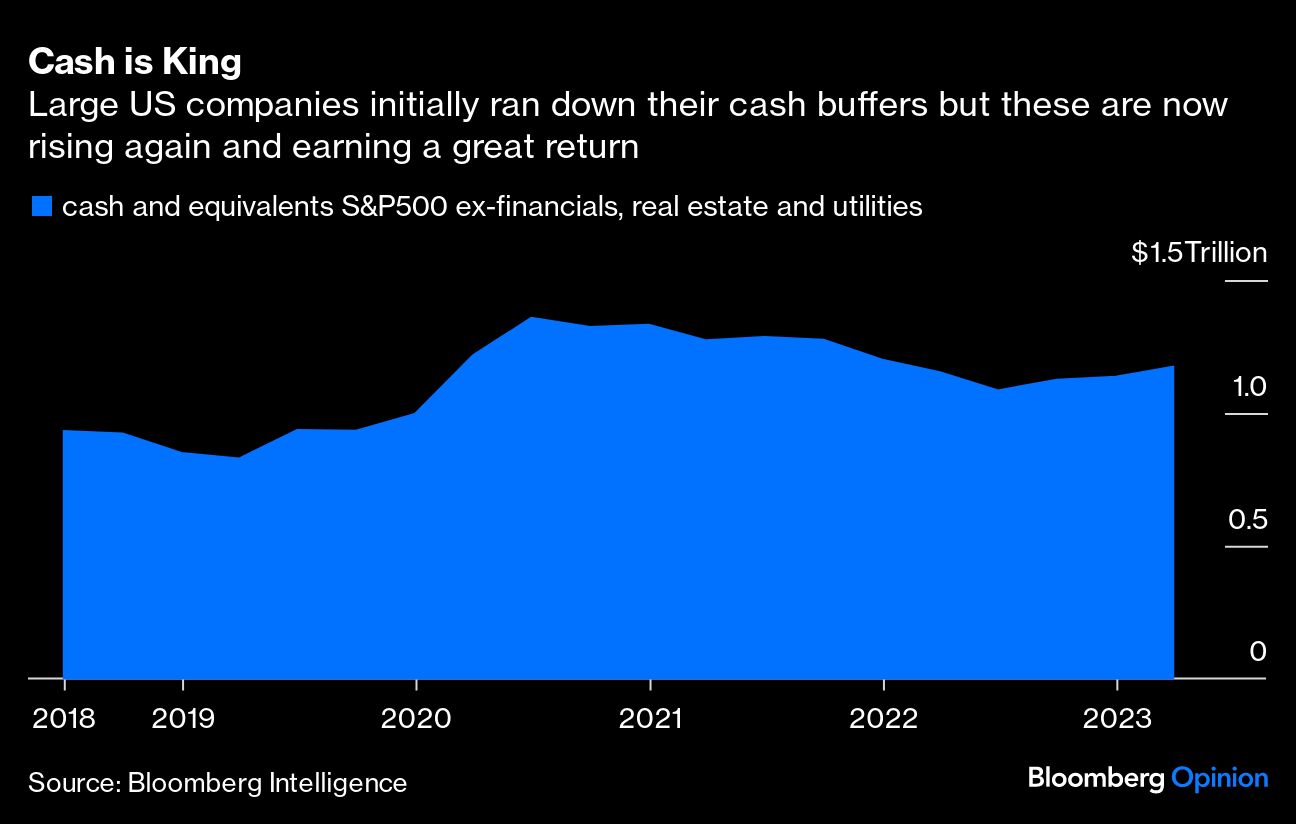

Large companies were able to lock in low-interest costs during the pandemic via fixed-rate, long-dated bonds, and since then earnings on their cash deposits have soared; hence many firms have more money left over for investments, to pay bills or to return to shareholders.

It’s part of the explanation for why the US economy has been surprisingly resilient. But the upshot is rates may need to remain higher for longer; this will put even more of a squeeze on small companies, which tend to have loans with floating rates modest cash balances, or both.

On average, S&P 500 companies are today paying an effective 3.3% interest rate on their borrowings, and nearly half of this debt matures after 2030, according to a recent Goldman Sachs Group Inc. analysis. In the meantime, US corporate cash is earning close to 5%. Floating-rate leveraged loans — often used by firms owned by private equity — account for just 18% of public debt issued by US-domiciled non-financial companies.

It’s not unlike how many homeowners now have a mortgage with a low, fixed interest rate and can relax on the veranda as their money-market fund investments pay off.

Societe Generale SA strategist Albert Edwards first drew my attention to the surprising decline in corporate net interest payments — a development he called “madness!” (My colleague John Authers wrote about it here).

The idea has since been discussed more widely. “It’s counterintuitive but true that higher interest rates have led to lower interest expense for corporate America in aggregate today,” hedge fund manager Boaz Weinstein, the founder of Saba Capital Management, said earlier this month. “So, many corporates have weathered the storm of higher rates reasonably well so far.”

Many are doing better than just OK. The cash and short-term investments held by Berkshire Hathaway Inc.’s insurance operations generated $1.4 billion of interest and investment income in the second quarter, six times more than in the same period a year ago. No wonder Warren Buffett isn’t in a hurry to deploy Berkshire’s $147 billion cash pile.

Like Berkshire, fintechs and travel companies that hold large amounts of client cash (a.k.a. “float”) are the big winners from higher rates. Though overshadowed by evidence that it faces increasing competition, payments processor Adyen NV generated €93 million ($101 million) of interest income in the first six months of this year — equivalent to 25% of pretax profit — which enabled the Dutch company to keep hiring.

Some airlines are also enjoying a tailwind. “EasyJet benefits from rising interest rates as the majority of our debt is fixed and we maintain floating rate cash balances,” the UK budget carrier told investors in May.

Companies with a high ratio of cash compared to borrowings are sitting pretty. Google’s parent company, Alphabet Inc., reported almost $900 million of interest income on its $118 billion cash balance in the second quarter, prompting questions about what it will do with the money.

Net Power Inc., a clean-tech company that went public in June, has $650 million of cash earning a more than 5% return, and no debt.

“We’re talking about $30 million or more coming in, in interest income. That’s offsetting the majority, if not all of our G&A [general and administrative expenses] right now,” the company’s CEO, Daniel Rice, boasted last week.

Texas-based construction firm Fluor Corp. received only $4 million of interest on its cash each quarter at the end of 2021. Now, that surplus is earning more than $50 million — contributing around 40% of pretax income. “Since our outstanding debt is at a fixed rate, I expect we will continue to generate positive net interest income throughout the year,” its chief financial officer, Joe Brennan, told analysts earlier this month.

“Higher interest rates were a net benefit given our cash position throughout the year,” tax-preparation company H&R Block Inc.’s CFO, Tony Bowen, told analysts last week. Carole Ferrand, CFO of French consultancy Capgemini SE, had a similar message for investors: “Interest income on our cash is increasing with rising interest rates while our bond debt is entirely at fixed rates.”

Big companies might be coping just fine with higher rates, but it’s a different story for small businesses. Over 40% of US small-cap debt is in the form of revolving credit facilities and term loans, which tend to have variable interest, notes Andrew Lapthorne, Societe Generale’s head of quantitative research.

And compared with the US, European companies — especially smaller firms — are more reliant on bank loans. Businesses in Italy and Spain have a higher share of variable rate and short-term debt versus those in France and Germany and thus will feel the impact of interest-rate hikes sooner, according to a study by the French central bank.

Over three-quarters of bank lending to UK businesses is floating rate, according to a recent Bank of England analysis; since the start of 2022, the average interest rate on those loans had risen by more than 400 basis points to around 6.5% by the end of May.

Though large companies are often net beneficiaries of rising rates, this doesn’t mean monetary tightening won’t eventually slow the economy as central banks intend.

Tesla Inc.’s more than $20 billion cash pile is earning a “ridiculous return,” but higher interest rates make its vehicles less affordable, CEO Elon Musk told investors in January.

Earning so much by just parking cash at a bank may deter companies from capital spending or buying back their shares. And net interest expenses will rise as companies deplete their cash savings or refinance their debts at much higher rates.

For now, though, interest-rate hikes aren’t squeezing big companies as much as I thought, and that’s making the Fed’s job harder.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Chris Bryant