One of the scarier financial factoids making the rounds this year is that local and regional banks hold 70% of US commercial real estate debt. Office buildings have been plummeting in value because of hybrid work, all commercial real estate faces challenges as low-interest loans mature amid higher rates, and look who’s holding the bag: the nation’s small and midsize banks, already facing doubters after deposit runs led to the failure of several of them earlier this year.

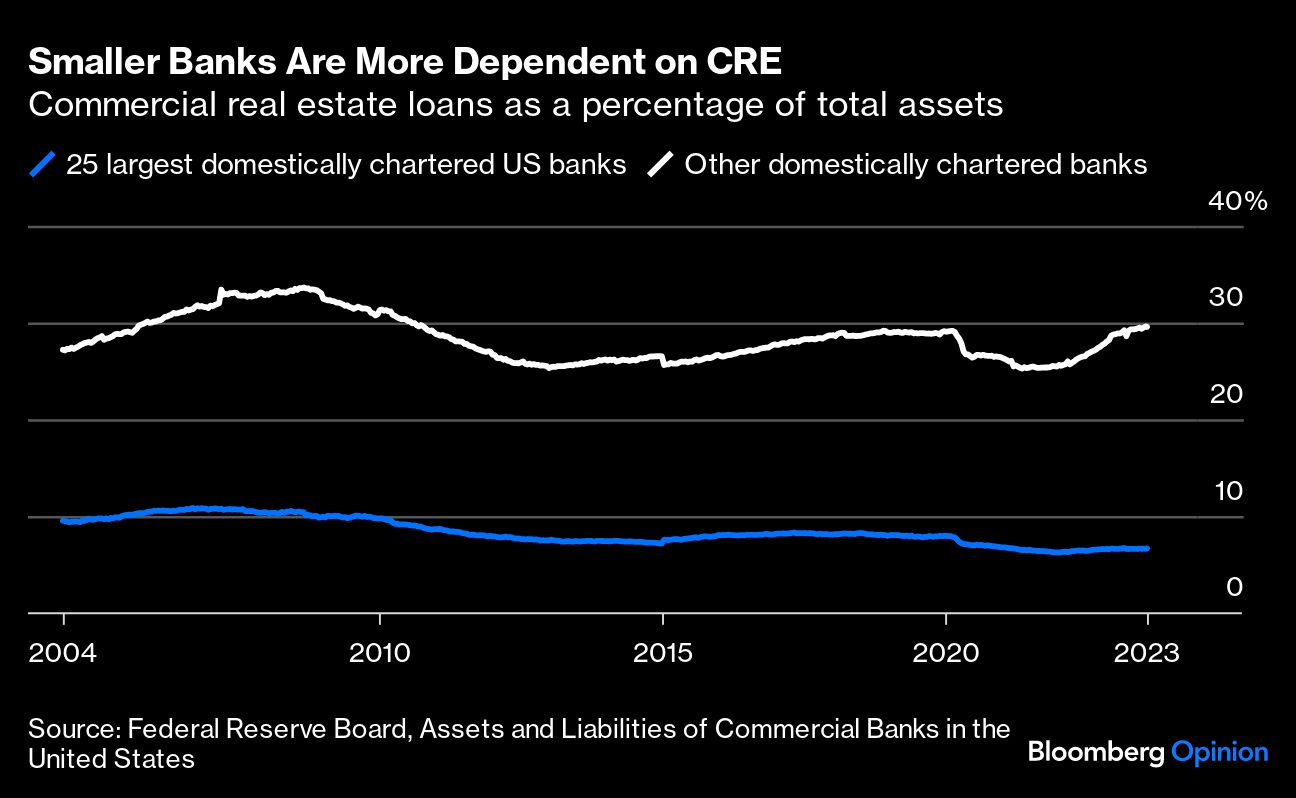

Happily, this factoid isn’t true. That is, small banks — defined as those, not among the country’s 25 largest — do in fact hold 69% of the commercial real estate loans on the balance sheets of domestically chartered commercial banks, up from 60% five years ago, according to the Federal Reserve’s weekly reports on bank assets and liabilities. But most US commercial real estate debt is owed to lenders other than domestically chartered commercial banks.

As of the end of March, this time according to the Fed’s quarterly Financial Accounts of the United States, domestic depository institutions (aka banks)1 held 47% of CRE debt, which works out to about 32% of the total in the hands of banks outside the top 25. That’s much less than 70%. It’s still a lot, though, and no other class of CRE lender comes close to the banks.

Perhaps more to the point for those worried about smaller banks’ commercial real estate exposure, CRE loans make up a much larger share of assets at smaller banks than they do at the 25 biggest.

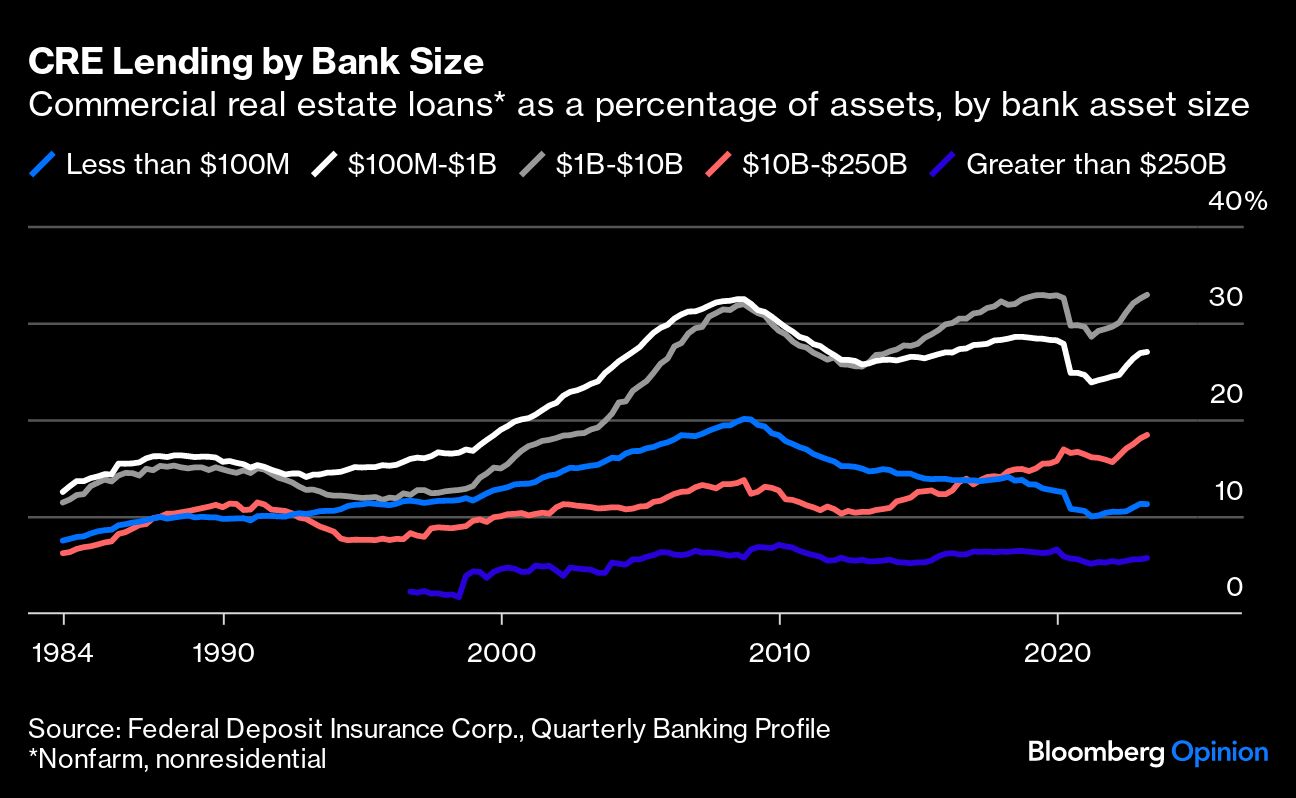

A longer-term view from the Federal Deposit Insurance Corp. that divides banks into five asset-size classes (and uses a narrower definition of commercial real estate) makes clear that the CRE concentration is highest for banks in the $100 million to $10 billion asset range — community banks, basically.

These banks usually serve smaller cities, or specific communities within larger ones, and their loans seldom finance big downtown office buildings. At OP Bancorp, which serves the Korean-American community in Los Angeles and where CRE loans make up almost 40% of assets, the average balance on those loans is just $838,526. At Mountain Commerce Bancorp Inc. in Knoxville, Tennessee, where CRE loans are 47% of assets, the loans are distributed among not just retail, warehouses and offices but hotels, campgrounds, marinas, mini-storage facilities and vacation rentals. At West Bancorporation Inc. in West Des Moines, Iowa, where CRE loans are 49% of assets, a recent investor presentation emphasizes that “office lending makes up less than 7% of the total loan portfolio, none of which is located in major metropolitan downtown areas.”

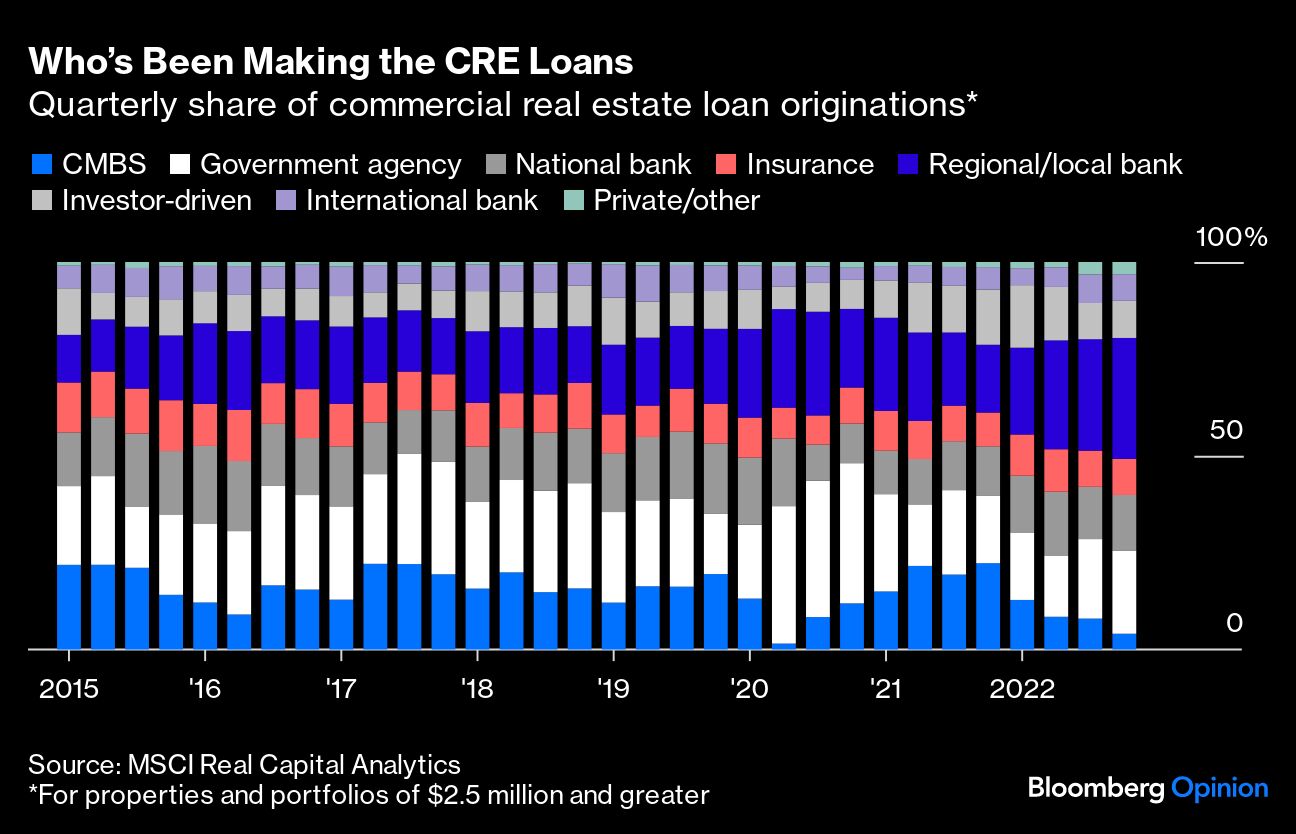

MSCI Real Capital Analytics, which tracks originations of commercial real estate loans for properties and portfolios worth $2.5 million or more, reports that the share originated by local and regional banks has more than doubled since late 2018, to 31% from 15%.

This increase is due in large part to deal activity shifting to smaller markets that other lenders are less likely to serve, said MSCI Real Assets team chief economist Jim Costello, who has been pointing out the falsehood of the 70% factoid for several months. The biggest decline in origination share has been for commercial mortgage-backed securities, which tend to be used for larger projects. On the whole, smaller banks seem to have been taking advantage of the shifts in economic activity causing distress in big urban office markets rather than being victimized by them. Also, because so many of their loans have been originated since 2019, relatively few will be maturing this year or next.

Of course, a low-interest loan originated in 2021 doesn’t do anything good for a bank’s profitability, and the fact that smaller banks are so dependent on commercial real estate lending as opposed to, say, trading, means that they will continue to struggle in the current interest-rate environment relative to the giants. But what seems to be the biggest, scariest challenge facing commercial real estate in the US at the moment — what to do about all those half-empty downtown office buildings — is for the most part, not a small-bank problem.

1. Credit unions and saving associations too, but they don't do much CRE lending.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Justin Fox